Automotive Bearing Market Summary

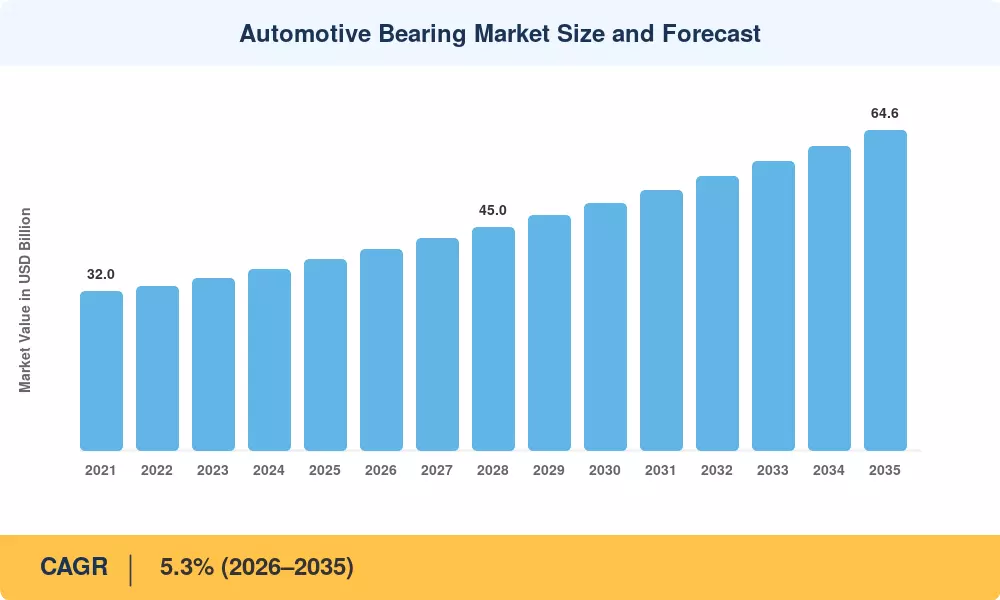

The Automotive Bearing Market was valued at USD 38.5 billion in 2025 and is projected to grow from USD 40.5 billion in 2026 to USD 64.6 billion by 2035, registering a CAGR of 5.3% during the forecast period. Two catalysts anchor this trajectory: global vehicle production volumes crossing 95 million units annually [1] and the accelerating shift toward electric drivetrains, which demand bearings engineered for higher rotational speeds and reduced friction losses. Government mandates—including the EU's Euro 7 emission standards and China's Phase VI fuel-efficiency requirements—are compelling automakers to source precision-engineered bearing solutions that cut parasitic energy losses by 15–20% compared to conventional designs [2].

Technology transformation is changing the Automotive Bearing Market from the inside. Legacy stamped-cage bearing assemblies are being replaced by polymer-cage and hybrid-ceramic equivalents to meet the needs of EV traction motors to operate above 20,000 rpm. Tier-1 suppliers have earmarked more than USD 2.8 billion in capital investment from 2023 to 2026 to retool production lines for next-generation bearing platforms [3]. Another frontier is sensor-integrated “smart bearings” with incorporated vibration and temperature monitoring, which allows for predictive maintenance and reduces warranty costs for OEMs.

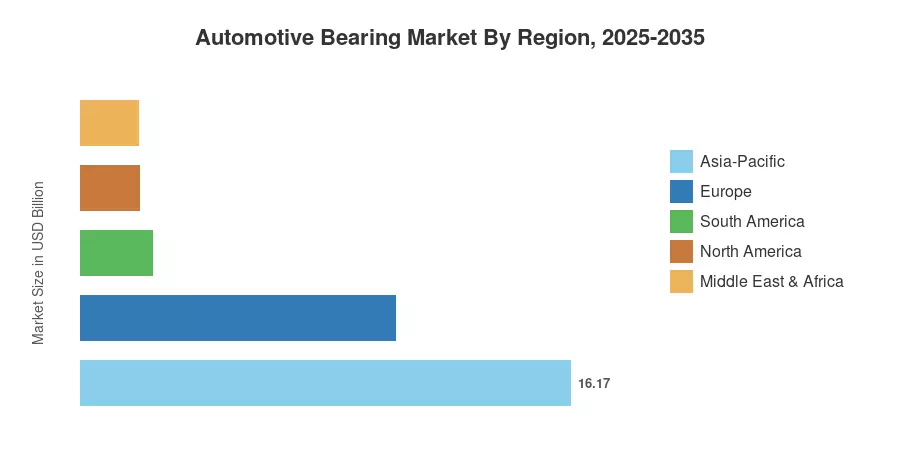

The Asia-Pacific region contributes to over 42% of the Automotive Bearing Market due to the large vehicle assembly ecosystems in China, Japan and India. The region also leads growth with an anticipated 6.8% CAGR through 2035. Europe retains the second largest share at over 27% supported by premium OEM demand and strict efficiency rules while North America accounts for around 20% supported by light-truck manufacturing and aftermarket replacement cycles. The Automotive Bearing Market is all set to expand further across all the vehicle classes with the launch of the electrification and autonomous driving platforms on a global scale.

Key Report Takeaways

• By Bearing Type

- Ball bearings held approximately 38% of the Automotive Bearing Market in 2025, driven by universal applicability across engine, transmission, and wheel assemblies.

- Roller bearings are projected to register a 5.6% CAGR through 2035, reflecting rising demand for heavy-load differential and axle applications.

- Plain bearings accounted for USD 6.9 billion in 2025 revenue, supported by crankshaft and connecting-rod use in internal combustion powertrains.

• By Application

- The wheel and hub segment represented the largest application share at about 30% of the Automotive Bearing Market.

- Engine-bearing applications generated approximately USD 9.6 billion in 2025.

- Transmission bearings are expected to achieve a 5.8% CAGR, fueled by multi-speed EV gearbox adoption.

• By Geography

- Asia-Pacific dominated the Automotive Bearing Market with a 42% revenue share in 2025.

- Europe's share stood at 27%, underpinned by premium automotive OEM concentration.

- South America is forecast to grow at 6.2% CAGR, led by expanding Brazilian vehicle production.

Market Size and Forecast (2021–2035)

Market sizing follows a triangulated approach combining top-down revenue analysis from bearing manufacturer annual filings, bottom-up unit-shipment modeling across vehicle production platforms, and third-party validation through customs trade-flow databases. Historical data (2021–2024) reflects actual reported values; the base year (2025) incorporates preliminary shipment data, and the forecast period (2026–2035) applies a compound growth rate calibrated against macroeconomic vehicle production projections and electrification penetration curves [1].