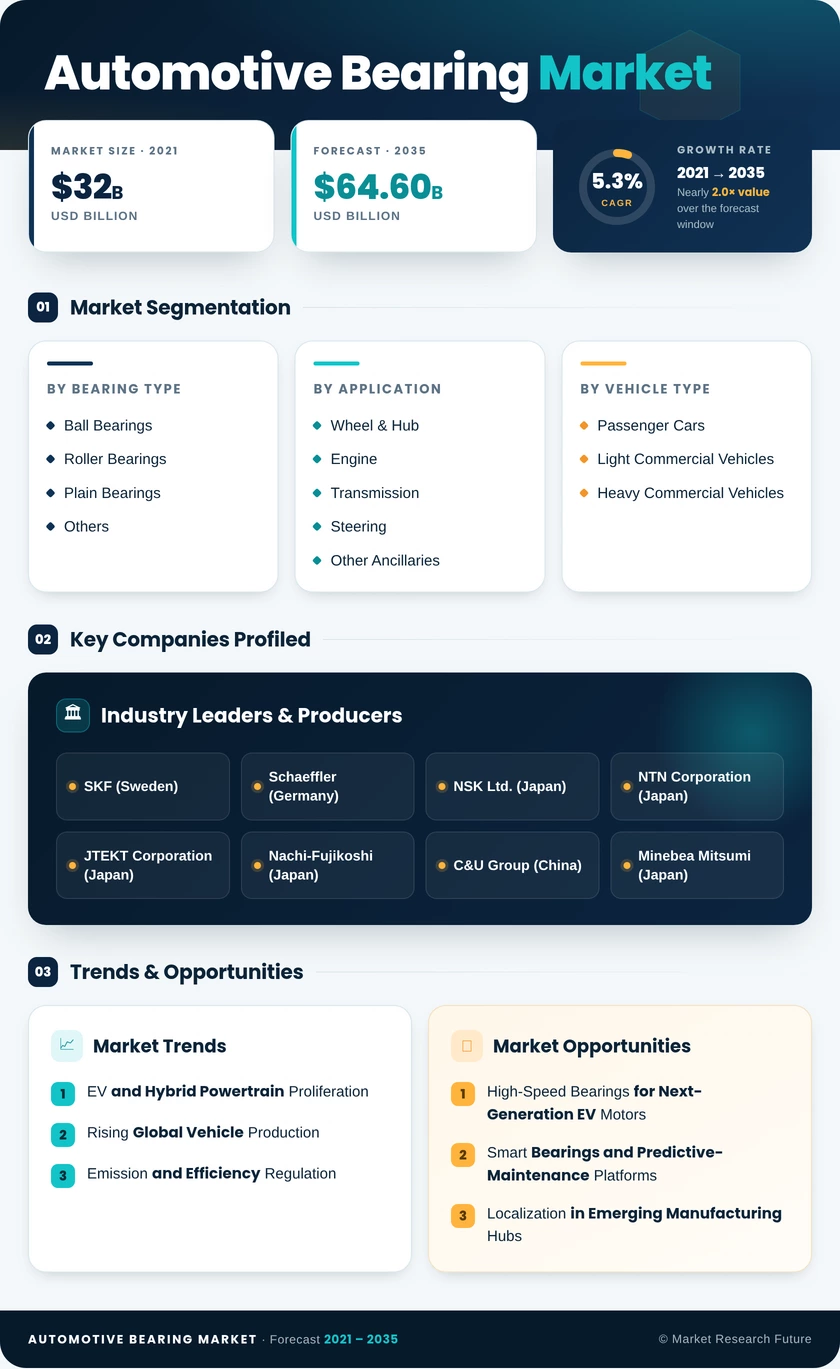

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Bearing Type | Ball Bearings, Roller Bearings, Plain Bearings, Others | Ball Bearings (38%) | Roller Bearings (5.6% CAGR) |

| By Application | Wheel & Hub, Engine, Transmission, Steering, Other Ancillaries | Wheel & Hub (30%) | Transmission (5.8% CAGR) |

| By Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles | Passenger Cars (55%) | Heavy Commercial Vehicles (6.1% CAGR) |

| By Sales Channel | OEM, Aftermarket | OEM (62%) | Aftermarket (5.9% CAGR) |

Market Segmentation Overview

By Bearing Type

| Sub-Segment | Key Trend |

| Ball Bearings | Expanding into EV traction-motor support, deep-groove variants dominate engine accessories. |

| Roller Bearings | Growing share in heavy-load differential and e-axle applications for electric SUVs and trucks |

| Plain Bearings | Steady demand from ICE crankshaft and connecting-rod assemblies; gradual decline with ICE phase-down |

| Others (Needle, Thrust, etc.) | Niche use in transmission synchronizer assemblies and steering columns; specialized high-value SKUs |

Ball bearings remain the most widely used bearing type across all powertrain architectures due to their balanced radial and axial load-handling capability at moderate cost. Roller bearings are gaining momentum as vehicle electrification drives heavier platform weights, particularly in SUV and truck segments where differential and wheel-end loads exceed ball-bearing design limits.

By Application

| Sub-Segment | Key Trend |

| Wheel & Hub | Integration of ABS/ESC sensors into hub-bearing modules increases unit value. |

| Engine | Large bearing count per ICE powertrain sustains volumes; gradual decline in BEV-dominant markets. |

| Transmission | Multi-speed EV gearbox adoption is doubling bearing count per transmission unit. |

| Steering | Electric power-steering shift is creating demand for low-friction, low-NVH bearings. |

| Other Ancillaries | HVAC compressor, turbocharger, and water-pump bearings providing stable incremental demand |

Wheel and hub bearings serve every wheeled vehicle regardless of powertrain type, making this segment resilient to the ICE-to-EV transition. Transmission bearings are the fastest-growing application, driven by the shift from single-speed to multi-speed reduction gearboxes in next-generation EV platforms.

By Vehicle Type

| Sub-Segment | Key Trend |

| Passenger Cars | Electrification is reshaping bearing specifications; the largest unit-volume segment. |

| Light Commercial Vehicles | E-commerce logistics growth is increasing LCV fleet sizes and replacement cycles |

| Heavy Commercial Vehicles | High per-vehicle bearing count (80–120 units) amplifying revenue contribution per unit sold |

Passenger cars generate the highest bearing volumes globally, while heavy commercial vehicles offer disproportionate revenue per vehicle due to their large bearing counts and premium specifications for durability and load capacity.

By Sales Channel

| Sub-Segment | Key Trend |

| OEM | Multi-year platform contracts lock in volumes; specification-driven procurement |

| Aftermarket | Aging vehicle parc expanding replacement demand; counterfeit competition a persistent challenge |

OEM procurement dominates total revenue, but the aftermarket channel offers higher per-unit margins and is growing faster as the global vehicle fleet ages and bearing replacement intervals shorten for older, higher-mileage vehicles.