Automotive Digital Mapping Market Summary

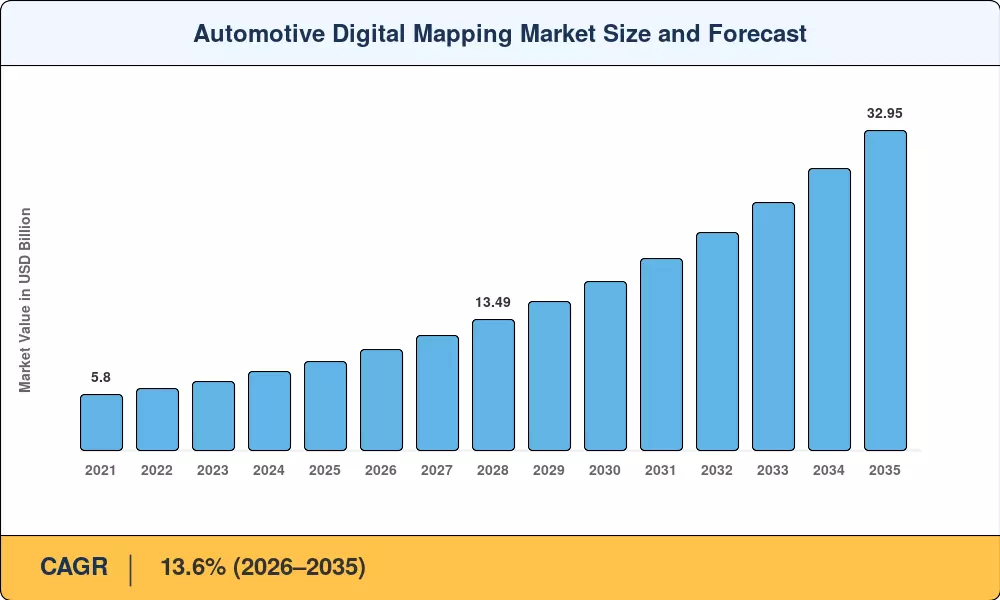

The automotive digital mapping market reached an estimated USD 9.20 billion in 2025 and is projected to grow from USD 10.45 billion in 2026 to USD 32.95 billion by 2035, registering a compound annual growth rate of 13.6% over the forecast period. Government-backed autonomous vehicle testing programs and the rapid expansion of connected car ecosystems across North America and Europe are the primary investment catalysts behind this acceleration. Automakers committed over USD 35 billion globally toward self-driving R&D between 2023 and 2025, much of which flows directly into high-definition spatial data infrastructure [2].

The automotive digital mapping market is experiencing a fundamental technology shift. Legacy turn-by-turn navigation databases — static, updated quarterly, and centimeter-imprecise — are being replaced by cloud-refreshed, sensor-fused spatial layers capable of sub-10-centimeter accuracy. This transition gained momentum after the European Commission allocated EUR 1.8 billion under Horizon Europe for intelligent transport corridor digitization through 2027 [3]. OEMs now treat mapping not as an infotainment add-on but as a safety-critical tier-one subsystem.

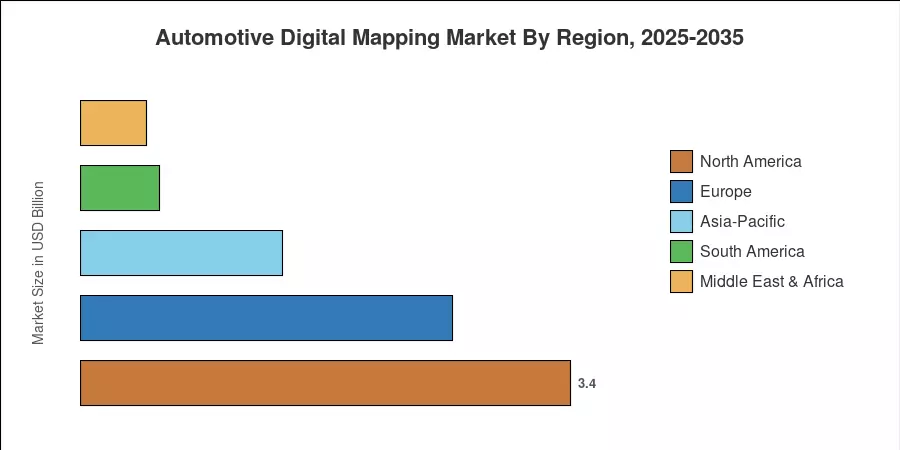

North America commands approximately 37% of the automotive digital mapping market, driven by Silicon Valley mapping investments and federal ADAS mandates. Asia-Pacific is the fastest-growing region with an estimated CAGR of 15.2%, fueled by Chinese and Japanese OEM demand. Europe holds a roughly 28% share, anchored by Germany's automotive corridor programs. As vehicle autonomy levels increase from L2+ to L3 and L4 through 2035, the mapping layer becomes the operational backbone of every self-driving platform.

Key Report Takeaways

• By Component

- Solutions dominate the automotive digital mapping market with approximately 64% revenue share in 2025, reflecting OEM preference for integrated map platforms over standalone service contracts.

- Services are expanding at a CAGR of 15.1% as fleet operators and ride-hail platforms demand real-time map update subscriptions.

• By Application

- The autonomous cars segment generated approximately USD 3.45 billion in 2025, reflecting the capital intensity of L3+ mapping requirements.

- ADAS applications represent the fastest-growing segment in the automotive digital mapping market at roughly 14.8% CAGR, driven by Euro NCAP and NHTSA mandates.

- Fleet management holds a steady 22% application share, benefiting from logistics digitization across e-commerce supply chains.

• By Region

- North America accounts for the largest share of the automotive digital mapping market, estimated at 37% of global revenue.

- Asia-Pacific is projected to grow at 15.2% CAGR through 2035.

- Europe contributes approximately USD 2.58 billion in 2025 base-year revenues.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down revenue analysis from OEM mapping procurement budgets with bottom-up licensing and subscription data from mapping vendors. Historical figures rely on verified company filings and regional trade data, while forward projections apply segment-adjusted growth modeling calibrated against macroeconomic and regulatory pipelines.