Automotive Relay Market Summary

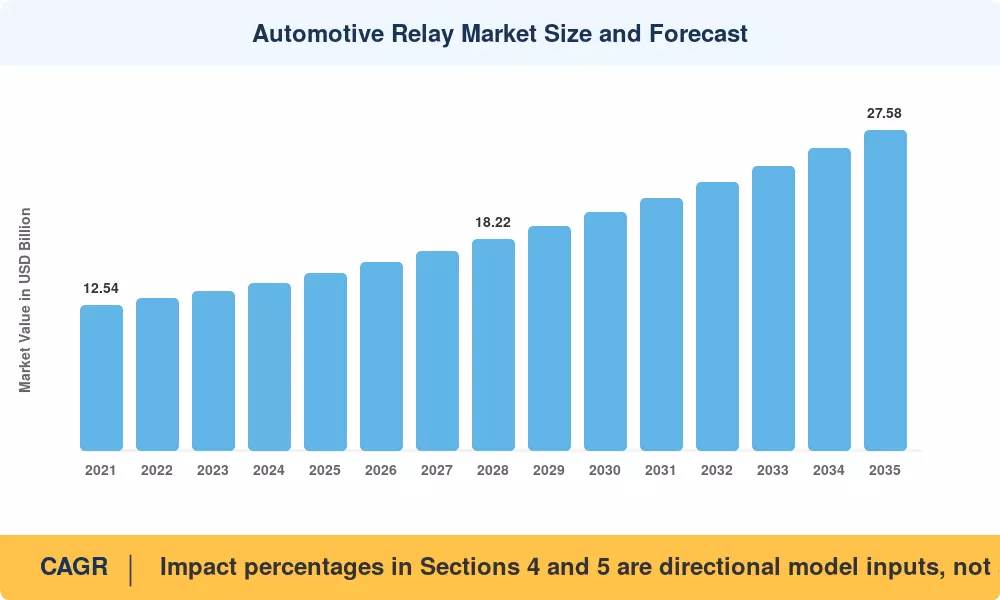

The Automotive Relay Market was valued at USD 15.25 billion in 2025 and is projected to grow from USD 16.18 Billion in 2026 to USD 27.58 billion by 2035, registering a CAGR of 6.1% during the forecast period (2026–2035). Two forces are reshaping demand simultaneously: the global electrification mandate — with over 40 countries committing to zero-emission vehicle targets by 2035 [1] — and the rapid proliferation of advanced driver-assistance systems (ADAS) required under the EU General Safety Regulation and NHTSA rulemaking in the United States [2]. Together, these regulatory catalysts are expanding the per-vehicle relay content from an average of 20 units in conventional cars to upwards of 40 in battery-electric platforms.

A pronounced technology shift is underway within the Automotive Relay Market. Electromechanical relays that once dominated powertrain switching are steadily yielding ground to high-voltage relay architectures designed for 400 V and 800 V EV battery systems. OEMs committed roughly USD 515 billion in announced EV-related capital expenditure between 2022 and 2030 [3], and every new electric platform requires pre-charge relays, main contactors, and auxiliary power relays absent from legacy ICE vehicles. This investment wave has triggered a parallel expansion of relay test and validation infrastructure across Tier-1 suppliers.

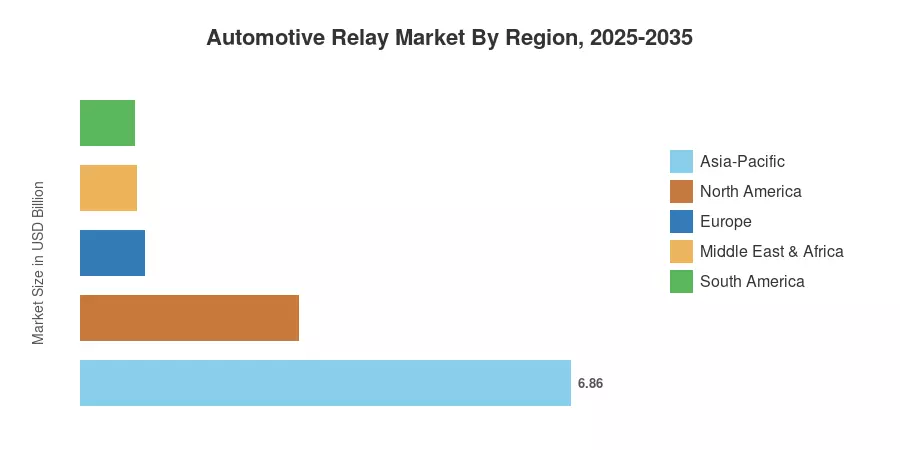

Asia-Pacific commands the largest share of the Automotive Relay Market at approximately 45% of global revenue, anchored by China's dominance in both vehicle production and EV adoption. The region also posts the fastest CAGR at 6.8%, propelled by India's Production-Linked Incentive scheme for automotive electronics and Japan's established relay manufacturing base. Europe holds the second-largest regional share at roughly 25%, driven by the EU's stringent CO₂ fleet-emission standards. The decade ahead will be defined by voltage architecture transitions and the integration of intelligent relay management into vehicle software platforms.

Key Report Takeaways

• By Type

- PCB relays account for the largest type-level share within the Automotive Relay Market, exceeding 28% of 2025 revenue, driven by their compact form factor for body-electronics modules.

- High-voltage relays represent the fastest-growing type segment with a projected CAGR of 8.4% through 2035, tied directly to EV battery-pack switching requirements.

• By Application

- Powertrain systems constitute the highest-value application in the Automotive Relay Market, reflecting the relay-intensive nature of engine/motor management and transmission control.

- Safety systems are expanding rapidly as ADAS mandates increase the electronic actuator count per vehicle across all major regulatory regions.

• By Region

- Asia-Pacific leads the Automotive Relay Market with a 45% revenue share, supported by annual vehicle production exceeding 50 million units in the region.

- North America contributes roughly 20% of global value, with growth anchored by the Inflation Reduction Act's EV manufacturing incentives.

- Europe's Automotive Relay Market is projected to grow at a 5.9% CAGR, underpinned by Euro 7 emission standards and the 2035 ICE phase-out timeline.

Market Size and Forecast (2021–2035)

Market Research Future employs a bottom-up revenue model combining Tier-1 supplier shipment data, OEM procurement disclosures, and trade-flow analysis. Historical estimates (2021–2024) are cross-referenced with customs-level import/export databases, while forecast projections (2026–2035) integrate IEA global EV outlook scenarios and regional production schedules.