Automotive Sensor Market Summary

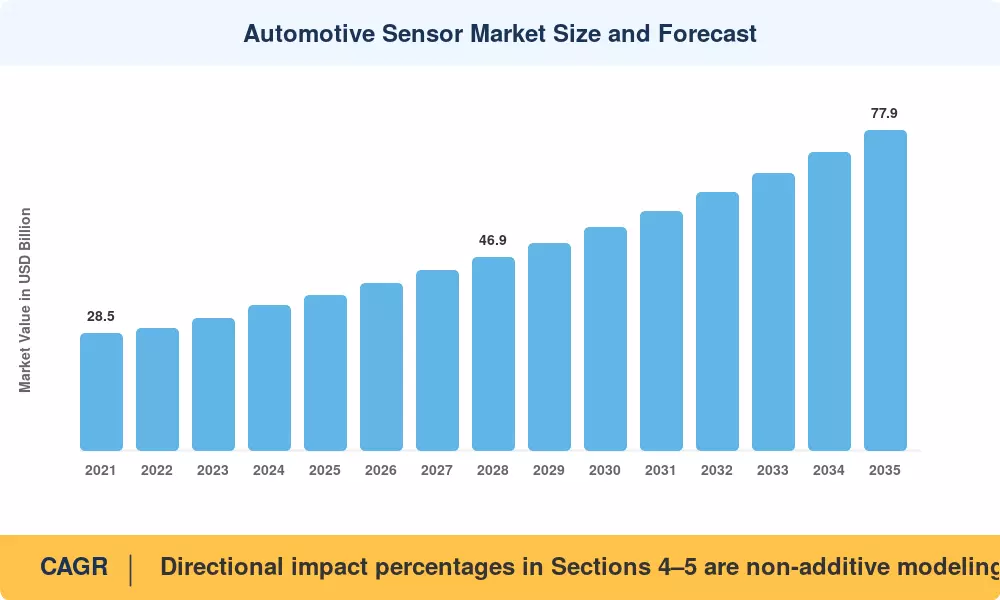

The global Automotive Sensor Market reached an estimated USD 37.8 billion in 2025 and is projected to grow from USD 40.6 billion in 2026 to USD 77.9 billion by 2035, registering a CAGR of 7.5% during the forecast period (2026–2035). This expansion is rooted in two converging forces: the worldwide push toward vehicle electrification — with over 40 countries committing to zero-emission vehicle mandates by 2035 [1] — and the rapid adoption of advanced driver-assistance systems (ADAS) now mandated in new vehicles across the European Union and increasingly in North America [2]. Automotive sensors serve as the nervous system of modern vehicles, converting physical phenomena into actionable data for everything from engine management to autonomous navigation.

The Automotive Sensor Market technical landscape is in the middle of a generational transformation. High-precision MEMS, solid-state radar, imaging and LiDAR modules are taking over basic powertrain monitoring from legacy analog sensors, and they can allow Level 3+ autonomous driving. According to the Semiconductor Industry Association [3], more than USD 78 billion of committed fab investments in the worldwide automotive semiconductor industry, directly supporting sensor production, were made from 2022 to 2025. Regulatory obligations such as the Euro 7 emissions standards and the U.S. EPA Tier 4 framework are also pushing OEMs to add more exhaust and emissions sensors in every vehicle.

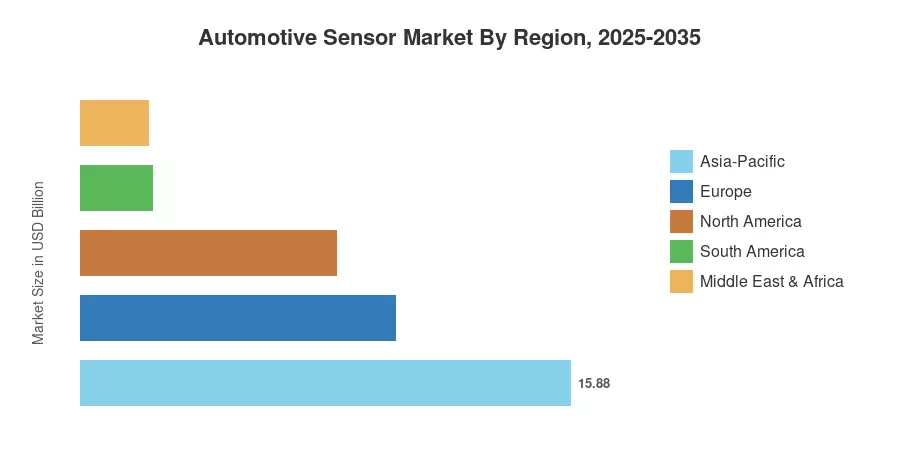

The Automotive Sensor Market is dominated by Asia-Pacific with close to 42% revenue share, led by China, being the world's largest car manufacturing and severe EV subsidies. Europe has the second-highest share at about 27%, spurred by strict ADAS and emissions legislation. North America is making up around 22% of market value, riding on the tail of EV subsidies from the Inflation Reduction Act and a renewed push for domestic chip manufacture. The Asia Pacific region is the fastest expanding, with a CAGR of 8.9% through 2035 as India and Southeast Asian markets ramp up vehicle electrification [4].

Key Report Takeaways

• By Sensor Type

- Pressure sensors command the largest revenue share in the Automotive Sensor Market at approximately 21% of the 2025 value, sustained by mandatory tire-pressure monitoring and fuel-injection control systems.

- Radar sensors represent the fastest-growing segment, registering a CAGR of 10.8% through 2035 as OEMs scale ADAS from premium to mass-market vehicle platforms.

- Image sensors account for roughly USD 5.2 billion in 2025, propelled by surround-view camera systems and driver monitoring requirements.

• By Application

- Chassis & Safety (ADAS) applications constitute the fastest-expanding application category, with a projected CAGR of 9.4% in the Automotive Sensor Market.

- Powertrain & Drivetrain applications hold the largest share at approximately 34% of total sensor demand, reflecting the enduring need for combustion, hybrid, and EV powertrain monitoring.

• By Region

- Asia-Pacific leads the Automotive Sensor Market with a 42% share, while growing at 8.9% CAGR.

- North America contributes approximately USD 8.3 billion in 2025 market value, underpinned by OEM ADAS rollouts and IRA-linked EV manufacturing.

- Europe sustains a strong position with ~27% share, driven by EU General Safety Regulation mandates.

Automotive Sensor Market Size and Forecast (2021–2035)

The market size estimates below draw on a triangulated methodology combining bottom-up sensor shipment volumes from tier-1 supplier disclosures, top-down automotive production forecasts from OICA, and cross-referencing against semiconductor revenue data from the World Semiconductor Trade Statistics organization [3][5]. Historical figures reflect actual industry conditions, including the 2021–2022 chip shortage impact and the 2023–2024 ADAS-driven recovery.