Automotive Wheel Rims Market Summary

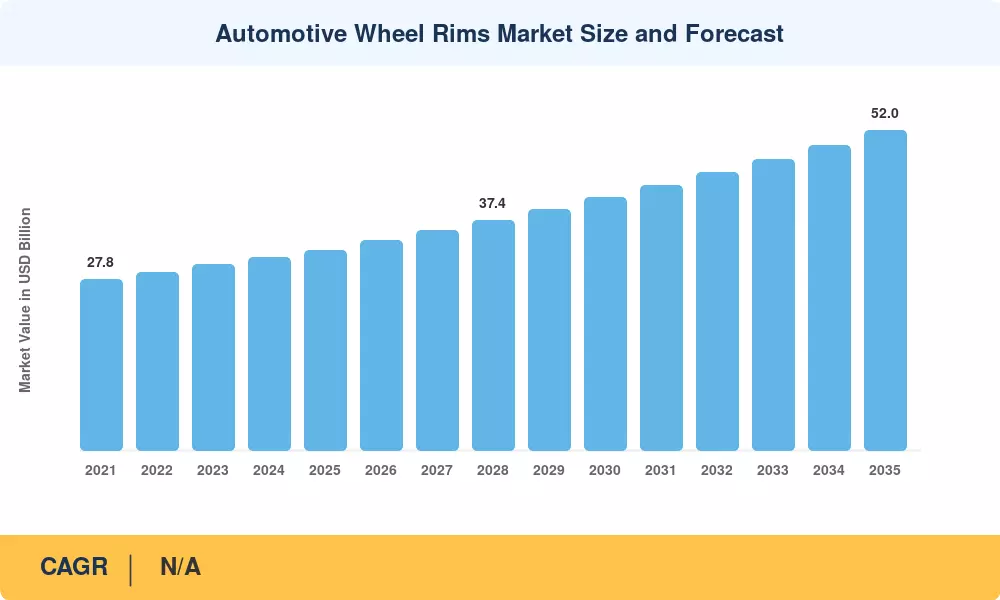

The Automotive Wheel Rims Market reached an estimated USD 32.5 billion in 2025 and is projected to grow from USD 34.1 billion in 2026 to USD 52.0 billion by 2035, registering a CAGR of 4.8% during the forecast period (2026–2035). Two forces are driving this acceleration: tightening fuel-economy mandates across major automotive markets — the EU's CO₂ fleet standard of 93.6 g/km effective 2025 and the U.S. CAFE target of 49 mpg by 2026 — and a surge in consumer preference for larger-diameter, aesthetically differentiated wheels that command higher per-unit revenue [1][2]. Global light-vehicle production, expected to surpass 92 million units annually by 2027, provides the volume floor on which this growth rests [3].

A material-technology transition is reshaping the Automotive Wheel Rims Market. Traditional pressed-steel designs that dominated economy segments for decades are steadily losing ground to low-pressure die-cast and flow-formed aluminum alloy wheels, which offer a 30–40% weight reduction per corner. OEMs are specifying lightweight rims as a zero-cost compliance lever for emissions targets — every kilogram removed from unsprung mass yields disproportionate efficiency gains. Investment in alloy casting capacity exceeded USD 1.2 billion across Asia-Pacific foundries between 2022 and 2024, signaling long-term structural commitment [4][5].

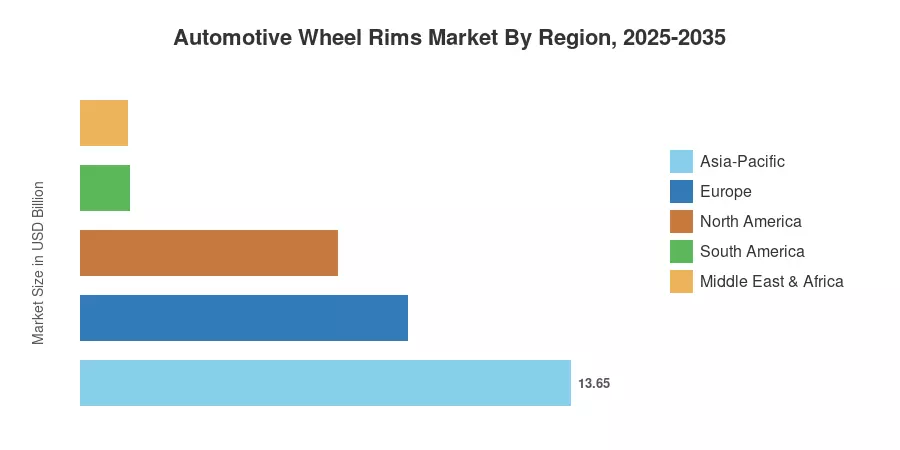

Asia-Pacific commands approximately 42% of global revenue, driven by China's and India's combined output of over 35 million passenger vehicles per year. Europe holds the second-largest position with roughly a 28% share, supported by premium OEM specification trends in Germany and Italy. North America — at 22% share — is the third-largest region but benefits from the highest aftermarket spend per vehicle. The fastest-growing region is Asia-Pacific, projected at a 5.9% CAGR through 2035, as rising disposable income in Southeast Asia and India accelerates the shift from steel to alloy rims.

Automotive Wheel Rims Market — Key Report Takeaways

By Material Type

- Aluminum alloy wheels account for an estimated 58% of global Automotive Wheel Rims Market revenue in 2025, led by OEM adoption in the B- and C-segment passenger car classes.

- Steel wheels retain a meaningful presence in commercial-vehicle and entry-level passenger segments, valued at approximately USD 9.8 billion.

- Carbon-fiber-reinforced polymer (CFRP) wheels are the fastest-growing material segment, expanding at a CAGR of 8.2% as performance and luxury OEMs integrate them into factory options.

By Sales Channel

- OEM sales represent roughly 62% of the Automotive Wheel Rims Market, reflecting the growing OEM practice of offering multiple wheel-design tiers at the point of vehicle purchase.

- Aftermarket channels are projected to reach USD 20.3 billion by 2035, fueled by customization culture and e-commerce wheel-and-tire bundles.

By Region

- Asia-Pacific leads the Automotive Wheel Rims Market with a 42% share, anchored by Chinese aluminum casting clusters in Zhejiang and Guangdong provinces.

- Europe's growth tracks premium vehicle output and EU lightweighting regulation.

- North America's aftermarket intensity — averaging USD 340 per vehicle annually on wheel-related accessories — sustains strong replacement demand.

Automotive Wheel Rims Market Size and Forecast (2021–2035)

Primary and secondary research underpins the Automotive Wheel Rims Market sizing methodology. Historical data (2021–2024) draws on OEM production volumes, trade-flow databases, and company filings. Forecast values (2026–2035) apply a bottom-up model segmenting demand by material, vehicle type, rim size, and sales channel, cross-validated against macroeconomic indicators including GDP growth, vehicle parc expansion, and regulatory timelines.