Autonomous Mobile Robot Market Summary

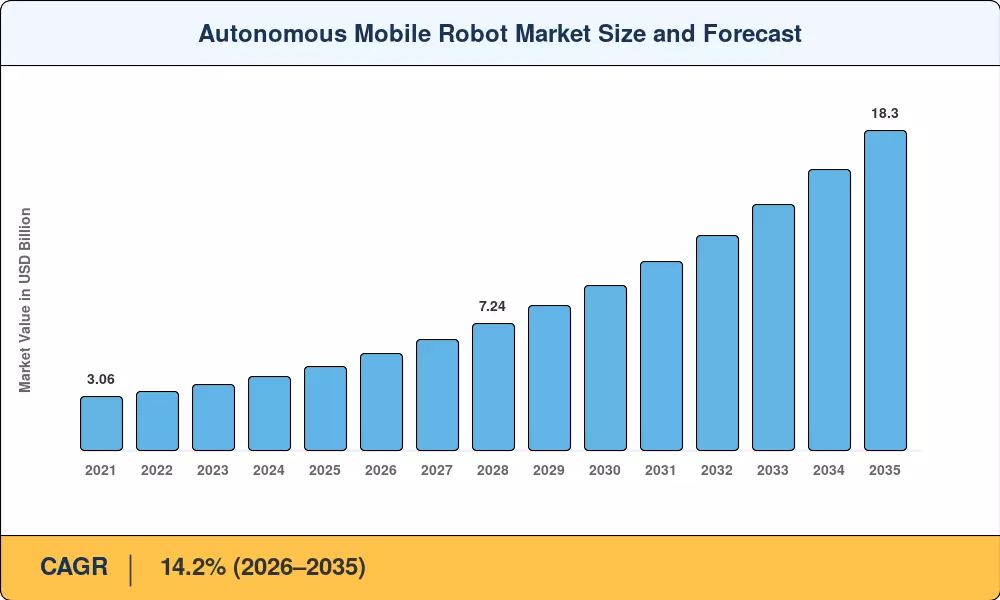

The Autonomous Mobile Robot Market was valued at USD 4.81 billion in 2025 and is projected to reach USD 5.54 billion in 2026 before climbing to USD 18.30 billion by 2035, expanding at a CAGR of 14.2% during 2026–2035. Two structural forces anchor this trajectory: persistent labor shortages across warehouse and manufacturing floors in OECD economies, and aggressive government incentive programs — including the EU's "Factory of the Future" grants and China's "Made in China 2025" robotics subsidies — that reduce capital-expenditure risk for mid-sized adopters [1][2].

The current technological revolution substitutes software-defined, sensor-fused platforms with real-time path planning capabilities for manually guided vehicles and fixed conveyor infrastructure. The total cost of ownership for AMR fleets decreased by about 18% from 2021 levels in 2024 as the price of lithium-ion batteries dropped below USD 140 per kWh [3]. Concurrently, multi-robot coordination at scale within brownfield facilities is made possible by advancements in 5G-Advanced connectivity, which enable centralized fleet orchestration at latencies sub 10 ms [4].

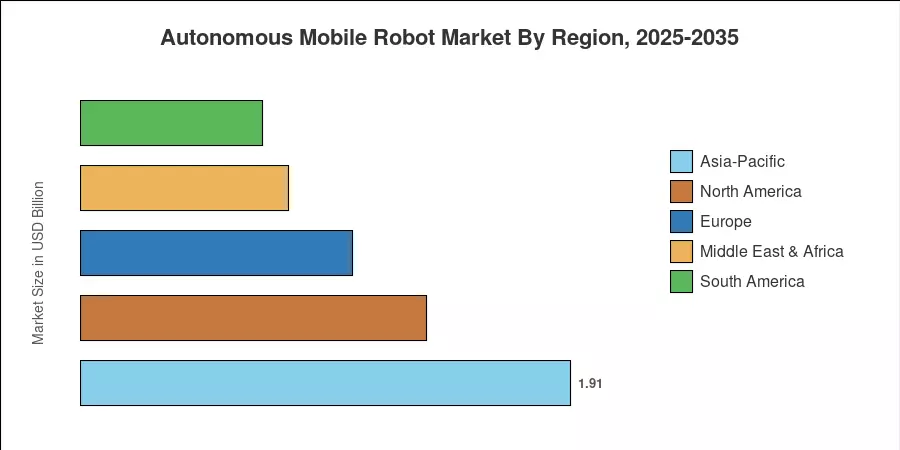

With a projected 39.8% revenue share in 2025, Asia-Pacific leads the autonomous mobile robot market because to Chinese integrators who combine competitive hardware pricing with in-house navigation stacks. With a predicted CAGR of 16.9% through 2035, the Middle East and Africa area is expected to develop at the quickest rate due to mega-project logistics in Saudi Arabia and the United Arab Emirates. At about 28%, North America has the second-largest market, driven by early adoption of humanoid platforms and need for e-commerce fulfillment.

Key Report Takeaways

• By Type

- Unmanned ground vehicles commanded approximately 48.5% of the Autonomous Mobile Robot Market in 2025, reflecting broad deployment across indoor logistics and manufacturing.

- Humanoid robots represent the fastest-expanding type segment, advancing at a projected 17.1% CAGR through 2035 as pilot deployments scale across automotive assembly and hospitality.

• By Navigation Technology

- LiDAR SLAM-based systems captured the leading share of the Autonomous Mobile Robot Market by navigation type in 2025.

- Vision-based navigation is forecast to grow at 18.9% CAGR through 2035, supported by declining camera-module costs and edge-AI chip advances.

• By End-User Industry

- Warehouse and logistics end users represented 35.4% of the Autonomous Mobile Robot Market in 2025.

- Healthcare facilities are projected to register the fastest end-user CAGR at 17.4% over the forecast period, fueled by pharmacy automation and intra-hospital delivery mandates.

• By Region

- Asia-Pacific led the Autonomous Mobile Robot Market with a 39.8% revenue share in 2025.

- The Middle East & Africa region is anticipated to expand at the highest regional CAGR of 16.9% through 2035.

Autonomous Mobile Robot Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining vendor revenue disclosures, import/export trade data, and bottom-up capacity modeling across 28 country markets. Historical figures (2021–2024) reflect audited vendor filings and validated shipment databases, while the forecast trajectory (2026–2035) embeds scenario-weighted assumptions for technology penetration, labor cost inflation, and regulatory stimulus timing.