Black Pepper Market Summary

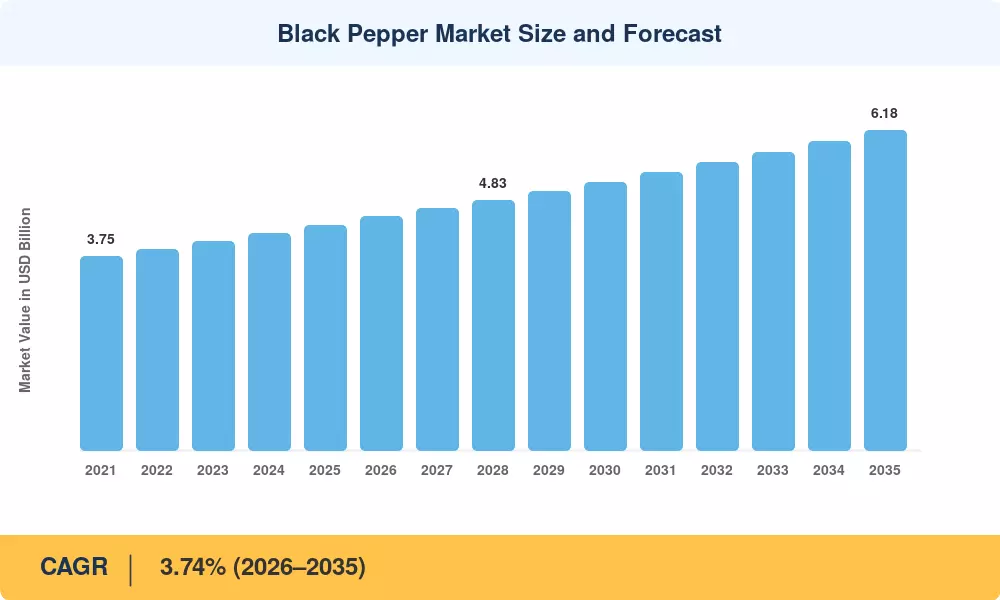

The black pepper market reached a valuation of USD 4.35 billion in 2025 and is projected to grow from USD 4.52 billion in 2026 to USD 6.18 billion by 2035, registering a CAGR of 3.74% during the forecast period. Rising demand for piperine bioactive compound extractions across nutraceutical and pharmaceutical applications has accelerated capital allocation toward advanced pepper cultivation and harvesting infrastructure. Vietnam's average export prices surpassed USD 7,000 per metric ton in early 2025, signaling a constrained global supply that benefits origin-linked processors with established multi-year procurement agreements [2].

Piper nigrum cultivation is undergoing a technology-driven transformation. Precision agriculture tools — including IoT-enabled soil moisture sensors, drone-based canopy health mapping, and AI-powered disease detection — are replacing traditional visual inspection methods across plantations in Vietnam, India, and Brazil. The Indian Spices Board committed approximately USD 48 million between 2023 and 2026 to promote climate-smart cultivation techniques and improve post-harvest processing yields among smallholder growers [3]. Blockchain-based traceability platforms now cover an estimated 18% of internationally traded whole and ground black pepper volumes, up from less than 5% in 2021.

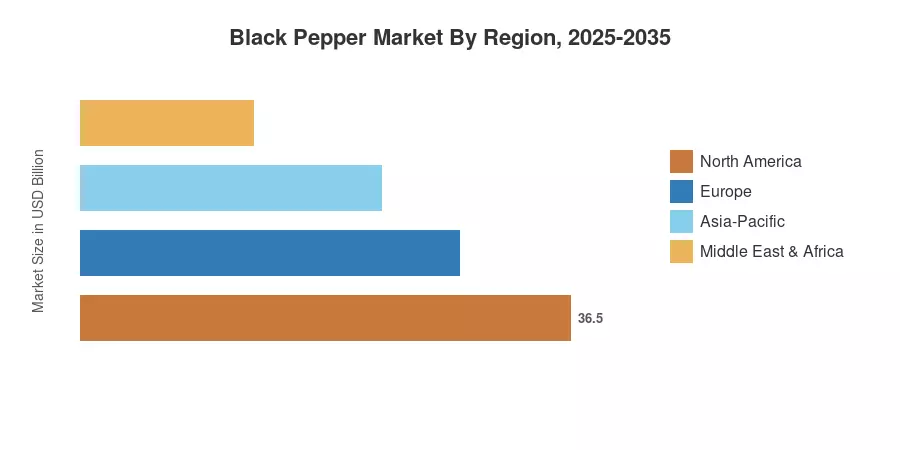

Asia-Pacific commands roughly 67% of the black pepper market, anchored by Vietnam's dominant export position and India's growing domestic consumption. Africa is the fastest-growing region with a projected CAGR of 4.10% through 2035, driven by expanding Piper nigrum cultivation in Madagascar, Uganda, and Tanzania. Europe holds the second-largest consumption share at approximately 15%, fueled by clean-label reformulation trends among food manufacturers. The black pepper market is poised for steady expansion as functional ingredient demand and supply chain formalization converge across both mature and emerging trade corridors.

Key Report Takeaways

• By Product Type

- Whole and ground black pepper accounted for an estimated 78% of the black pepper market in 2025, supported by food-service procurement and retail private-label expansion

- Black pepper essential oil is forecast to grow at a CAGR of 5.20% through 2035, driven by aromatherapy, personal care, and nutraceutical formulation demand

• By Application

- Food and beverage processing remains the anchor application in the black pepper market, representing approximately USD 3.10 billion in 2025

- Pharmaceutical and nutraceutical applications are expanding as clinical research validates piperine bioactive compound benefits for nutrient bioavailability enhancement

• By Region

- Asia-Pacific held roughly 67% of the black pepper market share in 2025, with Vietnam and India collectively accounting for over 80% of global production volume

- Africa is projected to register the highest regional CAGR of 4.10% through 2035, as Madagascan and Ugandan growers invest in pepper cultivation and harvesting modernization

- North America contributed approximately USD 0.42 billion to the black pepper market in 2025, with demand concentrated in clean-label food manufacturing

Market Size and Forecast (2021–2035)

The MRFR estimation approach combines the production volume data from FAOSTAT, trade flow data from ITC Trade Map, wholesale pricing indices from national commodities exchanges, and primary interviews with growers, processors, and distributors. All historical numbers are calendar-year farmgate-plus-processing revenues. Forecast values include supply-demand elasticity modeling and yield modifications based on El Niño probabilities.