Boiler Control Market Summary

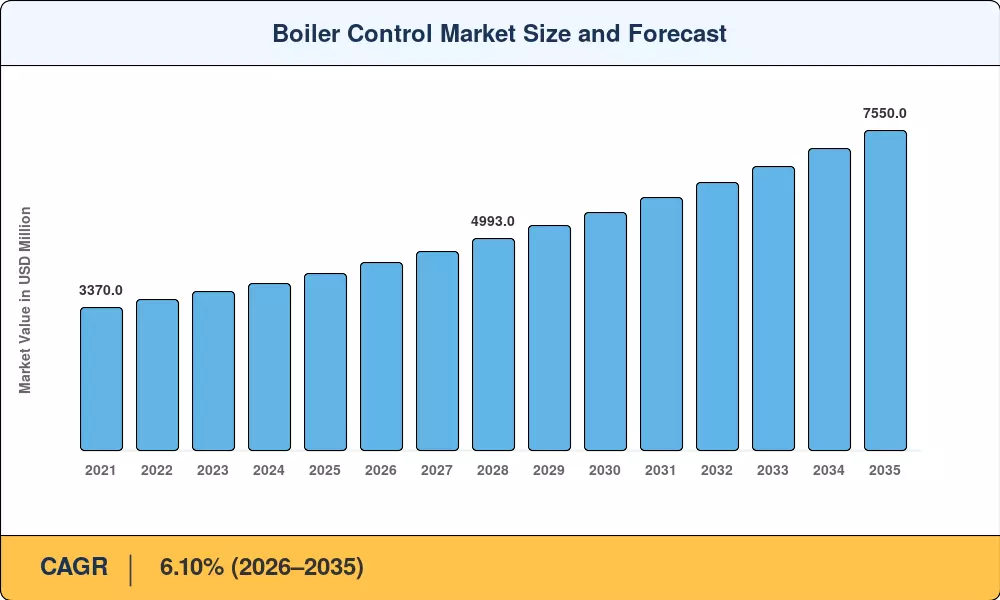

The Boiler Control Market reached an estimated USD 4,180 Million in 2025 and is projected to grow from USD 4,435 Million in 2026 to USD 7,550 Million by 2035, registering a CAGR of 6.10% over the forecast period. Two catalysts underpin this trajectory: tightening emissions regulations under frameworks such as the U.S. EPA's Boiler MACT rule and the EU Industrial Emissions Directive, and a sustained wave of industrial capacity additions across Asia-Pacific's power and process sectors [1][2]. As facility operators face rising natural-gas prices and carbon-cost exposure, the economic case for upgrading legacy controls has shifted from optional to urgent.

Aging pneumatic and relay-based control architectures — many installed during the 1990s and early 2000s — are giving way to digitalized platforms that integrate distributed control systems (DCS), programmable logic controllers, and cloud-connected analytics layers. The U.S. Department of Energy estimates that advanced boiler optimization can cut fuel consumption by 5–15%, translating to annual savings exceeding USD 30,000 per mid-size industrial boiler [3]. Facility owners are channeling this cost-avoidance narrative into capital budgets, accelerating retrofit cycles from 15 years down to 8–10 years.

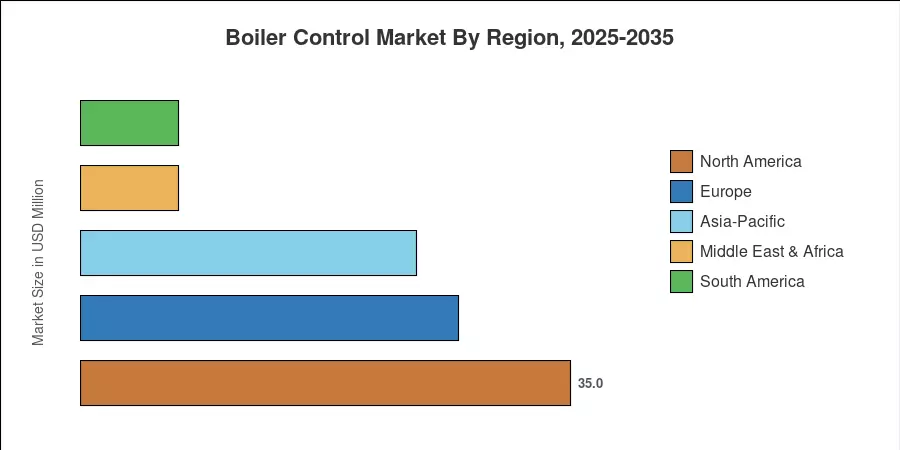

North America commands roughly 35% of global revenue, anchored by a mature installed base and stringent air-quality mandates. Asia-Pacific is the fastest-growing region, expanding at a CAGR of 7.40%, propelled by new coal-to-gas switching programs and greenfield manufacturing build-outs in China, India, and Southeast Asia. Europe holds the second-largest share at approximately 27%, driven by the EU Fit for 55 package and district-heating modernization. These three regions collectively will shape the Boiler Control Market trajectory through 2035.

Key Report Takeaways

• By Boiler Type

- Water Tube Boiler dominates with approximately 48% of the Boiler Control Market share in 2025, driven by heavy demand in power generation and large-scale process industries.

- Fire Tube Boiler is projected to register the fastest CAGR of 6.80% through 2035, supported by expansion in commercial heating and small-to-mid-scale manufacturing.

• By Component

- Hardware accounts for an estimated USD 2,760 million in 2025, reflecting continued investment in sensors, actuators, and controller modules across the Boiler Control Market.

- Software is growing at a CAGR of 7.20%, fueled by demand for predictive analytics platforms and remote-monitoring dashboards.

• By Region

- North America holds a 35% share of the Boiler Control Market, led by U.S. refinery and petrochemical retrofit cycles.

- Asia-Pacific is the fastest-growing region at a 7.40% CAGR, with China and India together accounting for over 60% of regional demand.

- Europe contributes approximately 27% of global value, with Germany and the Nordic countries leading district-heating upgrades.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up supplier revenue data with top-down macroeconomic indicators, validated against proprietary primary interviews with 45+ boiler OEMs, system integrators, and end-user procurement managers.

.webp?v=1782120130)