Building Automation Control Systems Market Summary

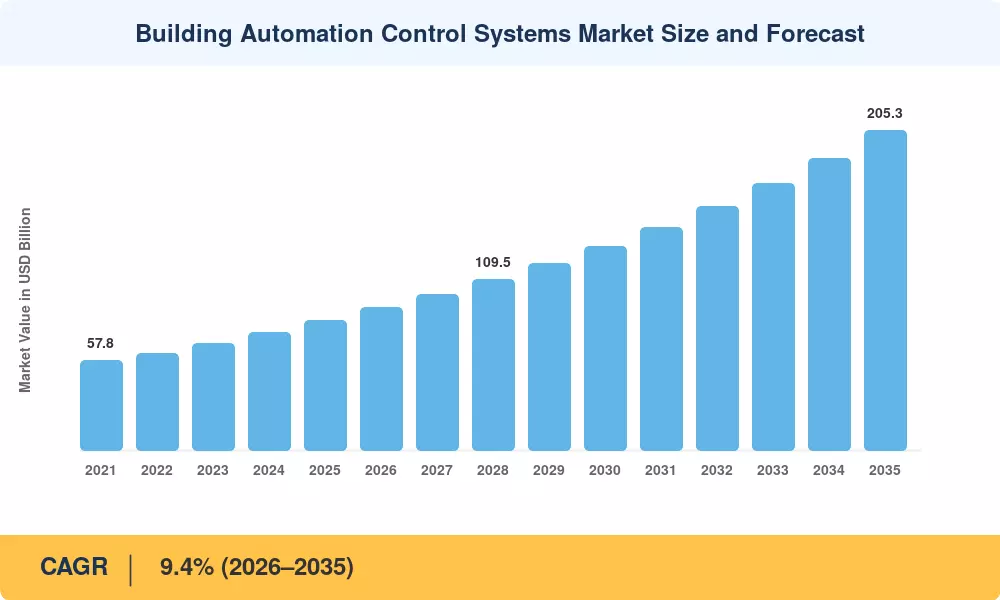

The Building Automation Control Systems Market reached an estimated USD 83.6 billion in 2025 and is projected to grow from USD 91.5 billion in 2026 to USD 205.3 billion by 2035, registering a CAGR of 9.4% during the forecast period (2026–2035). Two forces are accelerating this trajectory: the European Union's Energy Performance of Buildings Directive (EPBD) recast mandating automated controls in all non-residential buildings above 290 kW by 2030 [1]. The U.S. Inflation Reduction Act's USD 369 billion clean-energy package, which directs roughly USD 3.4 billion toward federal building decarbonization through advanced controls retrofits [2].

Disruption of the Building Automation Control Systems Market through technology transformation is centered on the replacement of traditional pneumatic actuators and standalone programmable logic controllers with cloud-connected IP-based supervisory platforms. These buildings, built before 2005, account for over 60% of the total commercial floor space worldwide and still depend on siloed single-loop controllers, wasting an estimated 20-30% of the HVAC energy [3]. Retrofit programs of the U.S. Department of Energy’s Better Buildings Initiative have shown 18–25% whole-building energy savings by replacing these antiquated designs with integrated automation platforms [4].

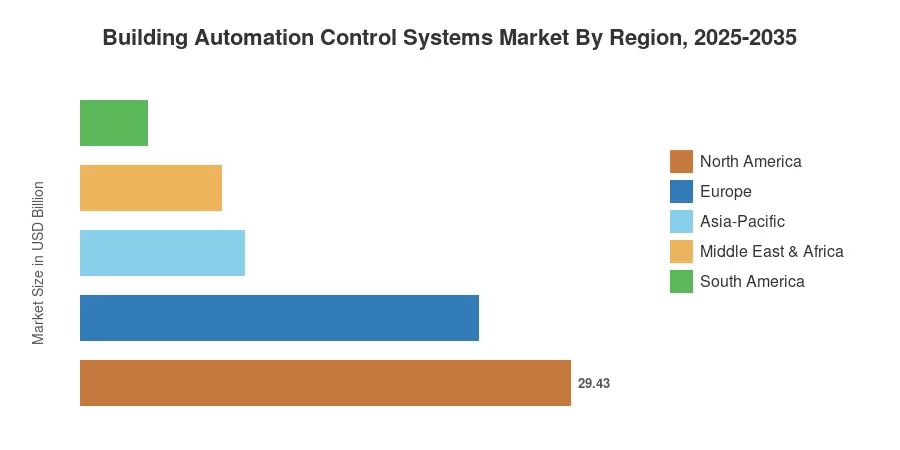

North America is the prominent region in the Building Automation Control Systems Market with a market share of 35.2% in 2025 due to stringent ASHRAE 90.1 code revisions and strong federal procurement rules. Asia-Pacific is the fastest-growing market, at a CAGR of 11.8%, owing to the dual-carbon policy of China and the revision of the Energy Conservation Building Code (ECBC) 2024 in India. The second greatest percentage in Europe, 28.6%, is also a key driver for the EU Taxonomy’s technical screening requirements for building renovations. From energy-management tools, automation systems will morph into full-stack operational intelligence platforms during the next decade.

Key Report Takeaways

• By System Type

- HVAC controls dominate the Building Automation Control Systems Market with a 42.3% revenue share in 2025, reflecting the outsized role of heating and cooling in commercial energy consumption.

- Security and access-control systems are expanding at a CAGR of 11.2% through 2035, propelled by converged physical-cyber security mandates in critical infrastructure.

- Lighting control systems generated approximately USD 12.8 billion in 2025, driven by LED-integrated daylight harvesting and occupancy-responsive dimming.

• By Component

- Software and analytics platforms represent the fastest-growing component segment at a 12.1% CAGR, as cloud-based supervisory solutions displace on-premise servers.

- Hardware — including controllers, sensors, and actuators — holds the largest share at 48.5% but faces margin compression from commoditization.

• By Geography

- The Building Automation Control Systems Market in North America accounted for USD 29.4 billion in 2025, reflecting early-mover regulatory pressure and deep retrofit pipelines.

- Asia-Pacific's 11.8% CAGR is the highest globally, with China and India together adding an estimated USD 28 billion in incremental demand by 2035.

- Europe's share is anchored by the EU's mandatory Building Automation and Control Systems (BACS) Class B requirement under EN 15232.

Market Size and Forecast (2021–2035)

Market Research Future estimates the global Building Automation Control Systems Market using a triangulated methodology that combines bottom-up revenue analysis of tier-1 OEMs, top-down macro-economic modeling of construction and retrofit spending, and primary interviews with over 120 industry stakeholders. Historical figures (2021–2024) are validated against publicly filed revenues of the top-10 suppliers; forecast projections (2026–2035) incorporate regulatory phase-in schedules, building-stock turnover rates, and regional energy-price scenarios.