Cable Tray Market Summary

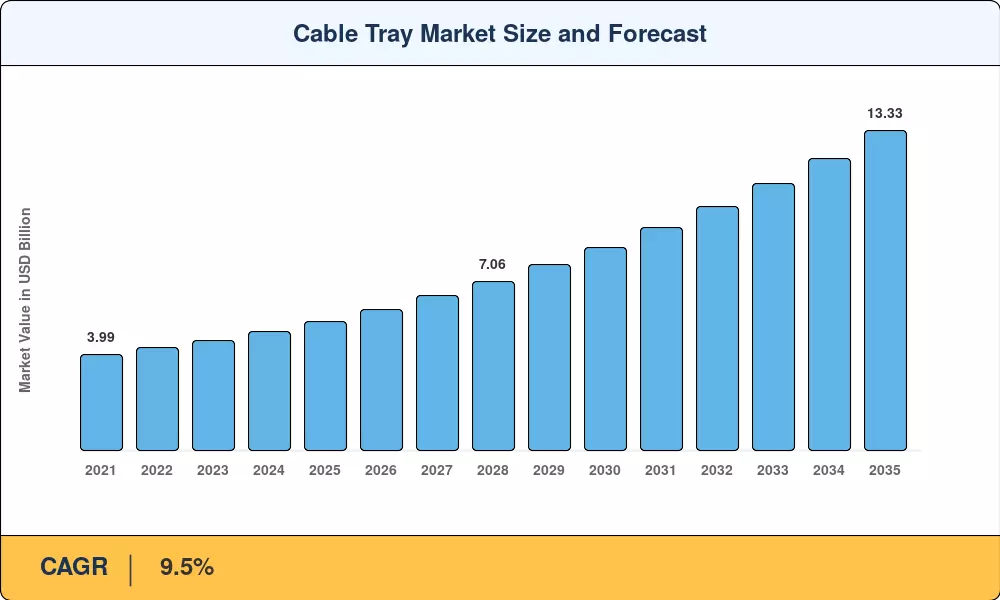

The cable tray market reached an estimated USD 5.38 billion in 2025, setting the stage for a forecast period that begins at USD 5.89 billion in 2026 and climbs to USD 13.33 billion by 2035, expanding at a CAGR of 9.5%. Two forces are doing the heavy lifting here: a global construction boom anchored by urbanization policies across Asia and the Middle East, and a parallel surge in data center investment that JLL projects will bring roughly 10 GW of new hyperscale and colocation capacity online by late 2025 alone, representing an estimated asset value near USD 170 billion [1].

Cable management is evolving well past basic wire routing. Legacy conduit-based systems — rigid, labor-intensive, and difficult to modify — are steadily giving way to modular tray architectures that accommodate higher cable densities, easier reconfiguration, and better airflow management. The U.S. Department of Energy's grid modernization initiatives and the EU's revised Construction Products Regulation are both pushing facility owners toward cable tray solutions that meet stricter fire-safety and ventilation codes [2][3].

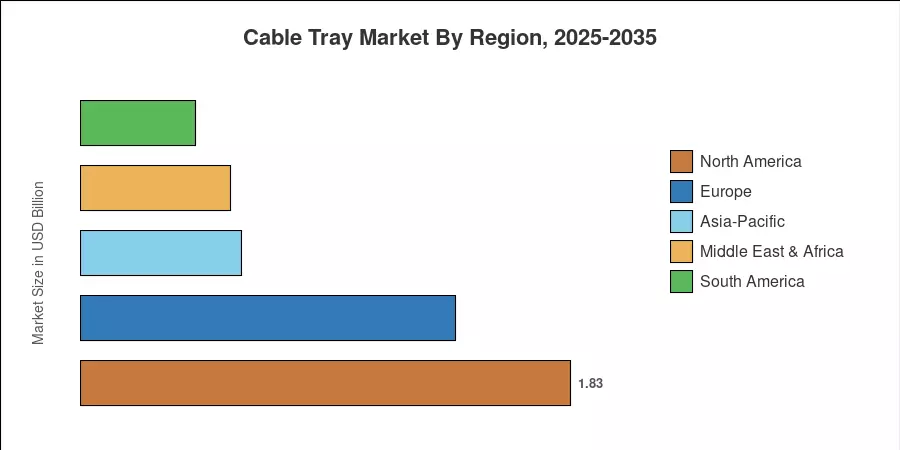

North America holds the dominant position in the cable tray market with roughly 34% of global revenue, driven by sustained utility infrastructure spending and data center expansion. Asia-Pacific is the fastest-growing region at a CAGR exceeding 11%, fueled by India's smart-city mission and China's 5G rollout. Europe accounts for the second-largest share at approximately 26%, supported by industrial modernization across Germany and the Nordic countries. The decade ahead will reward suppliers who can deliver lightweight, code-compliant systems at scale.

Key Report Takeaways

• By Material

- Steel remains the backbone of the cable tray market, commanding roughly 48% of global revenue in 2025, thanks to its load-bearing capacity and widespread availability in heavy-industrial environments.

- Aluminum is the fastest-growing material segment with a CAGR of 10.8% through 2035, favored for its corrosion resistance and lighter weight.

- Fiber-Reinforced Polymers (FRP) hold approximately 20% share, carving a niche in chemical plants and coastal installations where corrosion is a primary concern.

• By End-User Industry

- Power and Utilities represent the largest end-user group in the cable tray market, accounting for an estimated USD 2.04 billion in 2025.

- Construction contributes roughly 30% of total demand, propelled by commercial real-estate development and smart-building mandates.

• By Region

- North America generated the highest cable tray market revenue in 2025, led by the United States.

- Asia-Pacific is projected to grow at the steepest CAGR through 2035, with India and China as principal contributors.

- Europe's share sits near 26%, anchored by industrial retrofitting across Western economies.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from trade-association shipment data, customs records, and company filings, while the forecast model applies bottom-up demand projections across material, end-user, and regional dimensions, triangulated against top-down macroeconomic indicators including construction output and data center capital expenditure.