Canned Seafood Market Summary

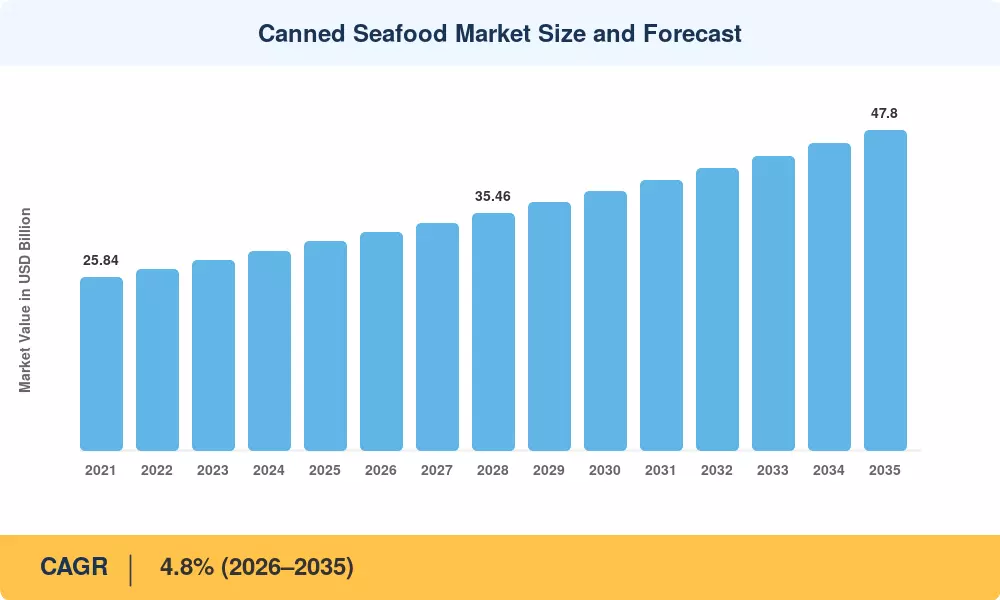

The global Canned Seafood Market stood at an estimated USD 31.2 billion in 2025 and is projected to reach USD 32.7 billion in 2026 before climbing to USD 47.8 billion by 2035, registering a CAGR of 4.8% across the forecast window of 2026–2035. Two catalysts anchor this trajectory: surging consumer demand for shelf-stable, high-protein convenience foods and a tightening regulatory environment around sustainable seafood canning practices that is reshaping procurement across the value chain. Government-backed traceability mandates — notably the EU's updated IUU Regulation and the U.S. SIMP program — have pushed processors to invest over USD 1.4 billion collectively in supply-chain digitization since 2022 [2].

The production landscape is undergoing a quiet but meaningful transformation. Legacy thermal-retort lines are giving way to high-pressure processing (HPP) and advanced nitrogen-flush packaging that extend shelf life while preserving omega-3 content and texture. Premium canned seafood brands have capitalized on this shift, commanding price points 40–60% above commodity tins by emphasizing single-origin sourcing and artisan preparation [3]. Retail data from IRI/Circana shows the premium tier grew at nearly twice the rate of the overall canned seafood category in 2024, validating the "tinned fish renaissance" trending across social media and specialty retail.

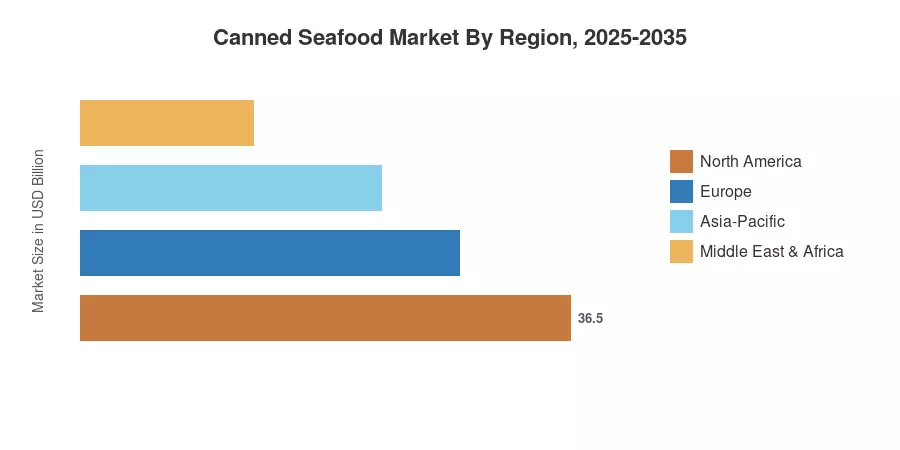

North America remains the dominant region, holding roughly 32% of global revenue, driven by strong private-label penetration and a mature retail infrastructure for ready-to-eat seafood convenience products. Asia-Pacific is the fastest-growing region, forecast to expand at a 6.1% CAGR through 2035, propelled by rising urbanization in Southeast Asia and growing cold-chain gaps that favor ambient protein. Europe accounts for approximately 27% of the Canned Seafood Market, anchored by Iberian and Scandinavian canning traditions and robust demand for canned sardines mackerel products The decade ahead will be shaped by how well processors balance cost efficiency with the sustainability credentials consumers increasingly demand.

Key Report Takeaways

• By Product Type

- Canned tuna holds the largest share at approximately 38% of the Canned Seafood Market, supported by its versatility across foodservice and retail channels

- Canned salmon is the fastest-growing product segment with a projected CAGR of 5.9%, driven by health-conscious consumers seeking omega-3-rich ready-to-eat seafood convenience options

- Canned sardines and mackerel collectively represent an estimated USD 7.4 billion in 2025 revenue, fueled by the canned sardines mackerel trend sweeping European and North American specialty retailers

• By Distribution Channel

- Supermarkets and hypermarkets account for roughly 52% of the Canned Seafood Market by value, reflecting the dominance of brick-and-mortar retail for shelf-stable proteins

- E-commerce is growing at a 7.3% CAGR, the fastest among all distribution channels, as DTC premium canned seafood brand offerings gain traction

• By Geography

- North America commands roughly USD 10.0 billion in 2025 revenue within the Canned Seafood Market

- Asia-Pacific is forecast to register a 6.1% CAGR, the highest regional growth rate, underpinned by expanding middle-class protein consumption in Indonesia, Vietnam, and the Philippines

- Europe holds the second-largest share at approximately 27%, with Spain, Portugal, and Norway leading in sustainable seafood canning capacity

Canned Seafood Market Size and Forecast (2021–2035)

Market size estimates draw on a triangulated methodology combining top-down trade-flow analysis (FAO FishStatJ, UN Comtrade), bottom-up processor revenue aggregation (company filings, trade association data), and demand-side validation through retail scanner datasets (NielsenIQ, Circana). All figures are expressed in constant 2025 USD.

.webp?v=1785231591)