Car Insurance Market Summary

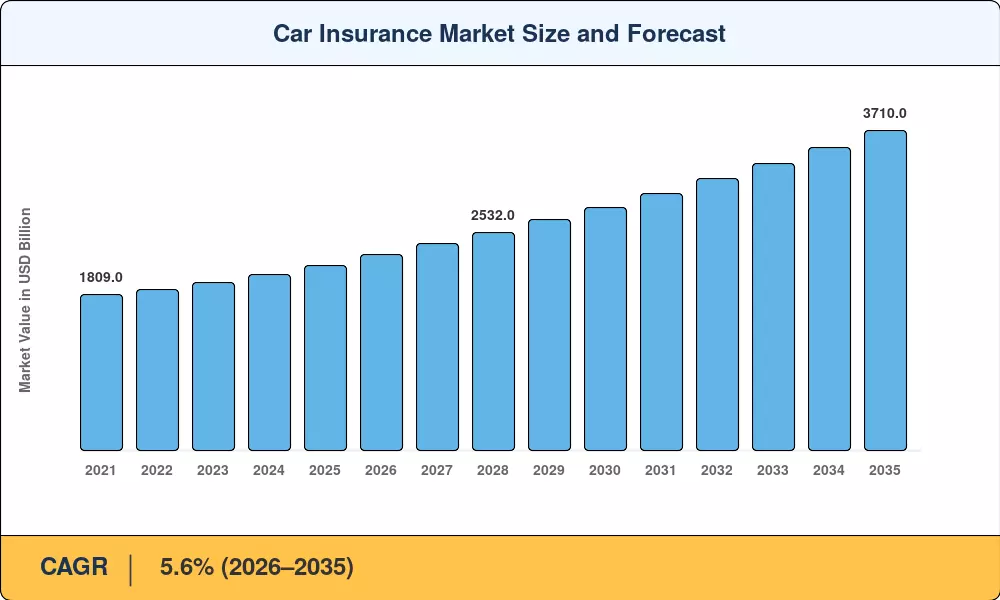

The global car insurance market reached an estimated USD 2,150 billion in premium value during 2025 and is projected to grow from USD 2,271 billion in 2026 to approximately USD 3,710 billion by 2035, registering a compound annual growth rate of 5.6% across the forecast window. Mandatory liability requirements continue to expand — at least nine US states tightened statutory minimum coverage limits between 2023 and 2025, while India's Motor Vehicles Amendment Rules raised third-party liability floors by 22% [1]. These regulatory ratchets convert directly into gross written premium gains and show no sign of reversing.

A sweeping digital overhaul is reshaping how policies are priced, sold, and serviced. Legacy broker-dependent distribution is giving ground to direct-to-consumer platforms that underwrite and bind coverage in minutes. Insurers collectively invested an estimated USD 18 billion in claims automation and digital underwriting infrastructure between 2022 and 2024, according to Global Insurance Report data [2]. Climate-driven insured losses, which surpassed USD 140 billion globally in 2024, are simultaneously hardening rates and encouraging parametric product innovation.

North America commands the largest share of the car insurance market at roughly 38% of 2025 premiums, underpinned by the world's highest average policy prices. Asia-Pacific is the fastest-growing region, expanding at an estimated 7.1% CAGR through 2035 as vehicle penetration surges in India, Indonesia, and Vietnam. Europe holds the second-largest position with approximately 27% of global premiums, driven by the EU Motor Insurance Directive revision and growing BEV adoption. The next decade will test which carriers can pair underwriting discipline with technology-led distribution at scale.

Key Report Takeaways

• By Coverage

- Own damage coverage accounted for 62.2% of the car insurance market share in 2025, reflecting consumer preference for comprehensive protection in high-repair-cost environments.

- Ancillary and add-on coverages are projected to record the fastest growth at an 8.5% CAGR through 2035 as cyber-liability riders and roadside-assistance bundles gain traction.

• By Powertrain

- Internal combustion engine vehicles represented 77.3% of premiums within the car insurance market in 2025.

- Battery electric vehicle insurance is forecast to expand at a 13.5% CAGR through 2035, propelled by rising EV registrations and higher average insured values.

• By Distribution Channel

- Intermediated channels — agents, brokers, and bancassurance — captured an estimated 62.8% of car insurance market premiums in 2025.

- Embedded, affinity, and partnership distribution models are advancing at a 9.6% CAGR through 2035.

• By Region

- North America held the dominant position in the car insurance market, representing approximately 38% of 2025 premiums.

- Asia-Pacific is projected to grow at a 7.1% CAGR, making it the fastest-growing region through 2035.

Car Insurance Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from disclosed gross written premium filings, national regulatory submissions, and verified industry databases. Forecast projections apply a proprietary model that weights mandatory-coverage expansion, claims inflation indices, vehicle parc growth, and digitalization adoption curves against macroeconomic baselines.