Cardiovascular Devices Market Summary

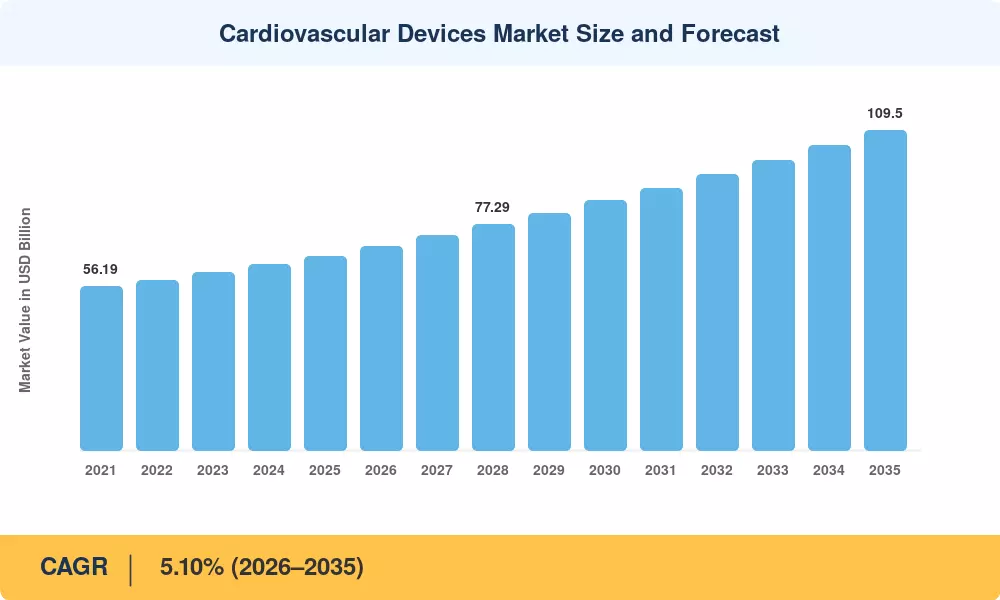

The Cardiovascular Devices Market size was valued at USD 66.55 Billion in 2025, and the market is projected to grow from USD 69.95 Billion in 2026 to USD 109.50 Billion by 2035, registering a CAGR of 5.10% during the forecast period 2026–2035. Rising cardiovascular disease prevalence across aging populations and expanded government screening mandates — including the U.S. Medicare Coverage of Innovative Technology pathway and the EU Medical Device Regulation (MDR 2017/745) transition — are anchoring demand for next-generation diagnostic and interventional platforms [1][2].

A sweeping technology shift is redefining this space. Legacy fluoroscopy-guided catheter procedures are giving way to AI-enabled imaging fusion, robotic-assisted percutaneous interventions, and leadless pacing systems. The National Institutes of Health allocated over USD 2.4 Billion to cardiovascular research in fiscal year 2024 alone, accelerating translational device development from bench to bedside [3]. Transcatheter solutions are displacing open-heart surgery for an expanding range of valve and structural pathologies, compressing hospital stays and lowering complication rates.

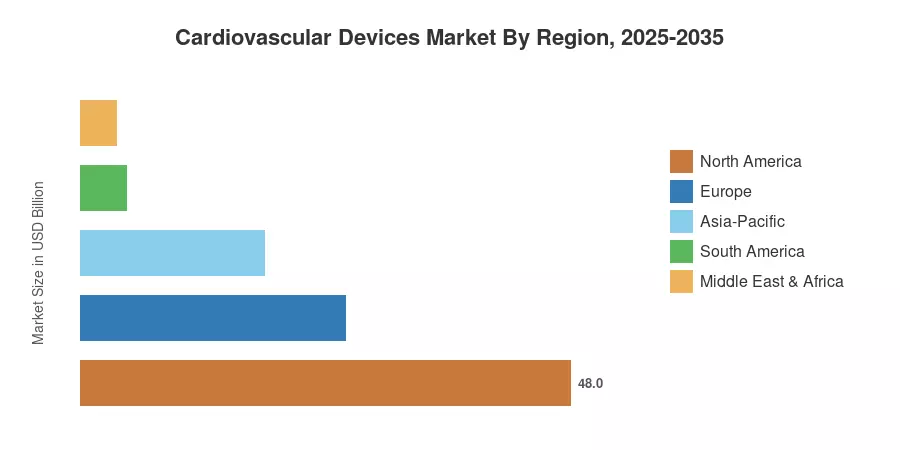

North America commands roughly 48% of the Cardiovascular Devices Market, backed by dense cath-lab infrastructure and favorable reimbursement. Asia-Pacific is the fastest-growing region at a projected CAGR of 9.1%, propelled by hospital capacity buildouts in China and India. Europe holds the second-largest share at approximately 26%, driven by harmonized MDR compliance investments and aging demographics. The decade ahead will hinge on how quickly AI-driven diagnostics and remote patient monitoring reshape clinical workflows globally.

Key Report Takeaways

• By Device Type

- Diagnostic and monitoring devices captured the largest share of the Cardiovascular Devices Market in 2025, reflecting sustained imaging and ECG platform upgrades.

- Therapeutic and surgical devices are expanding at a CAGR of 7.3% through 2035, fueled by transcatheter valve adoption and next-generation stent platforms.

• By Application

- Coronary artery disease represented approximately 48% of the Cardiovascular Devices Market in 2025.

- Structural heart disease is projected to grow at a CAGR of 8.0% to 2035, driven by expanded transcatheter mitral and tricuspid indications.

• By End User

- Hospitals and cardiac centers accounted for roughly 63% of revenue in 2025, reinforcing their role as primary procedure sites.

- Ambulatory surgical centers are registering the fastest end-user CAGR at 10.2%, reflecting outpatient migration for low-acuity interventions.

• By Region

- North America led the Cardiovascular Devices Market with approximately 48% share in 2025.

- Asia-Pacific is advancing at a 9.1% CAGR, the highest among all regions.

Cardiovascular Devices Market Size and Forecast (2021–2035)

Market sizing integrates bottom-up revenue analysis from device manufacturers' annual filings, regulatory clearance databases (FDA 510(k)/PMA, EU MDR EUDAMED), and proprietary hospital procurement surveys across 42 countries. Historical figures reflect reported revenues; forecast values apply segment-level growth models calibrated to demographic, reimbursement, and technology adoption curves [4][5].