Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

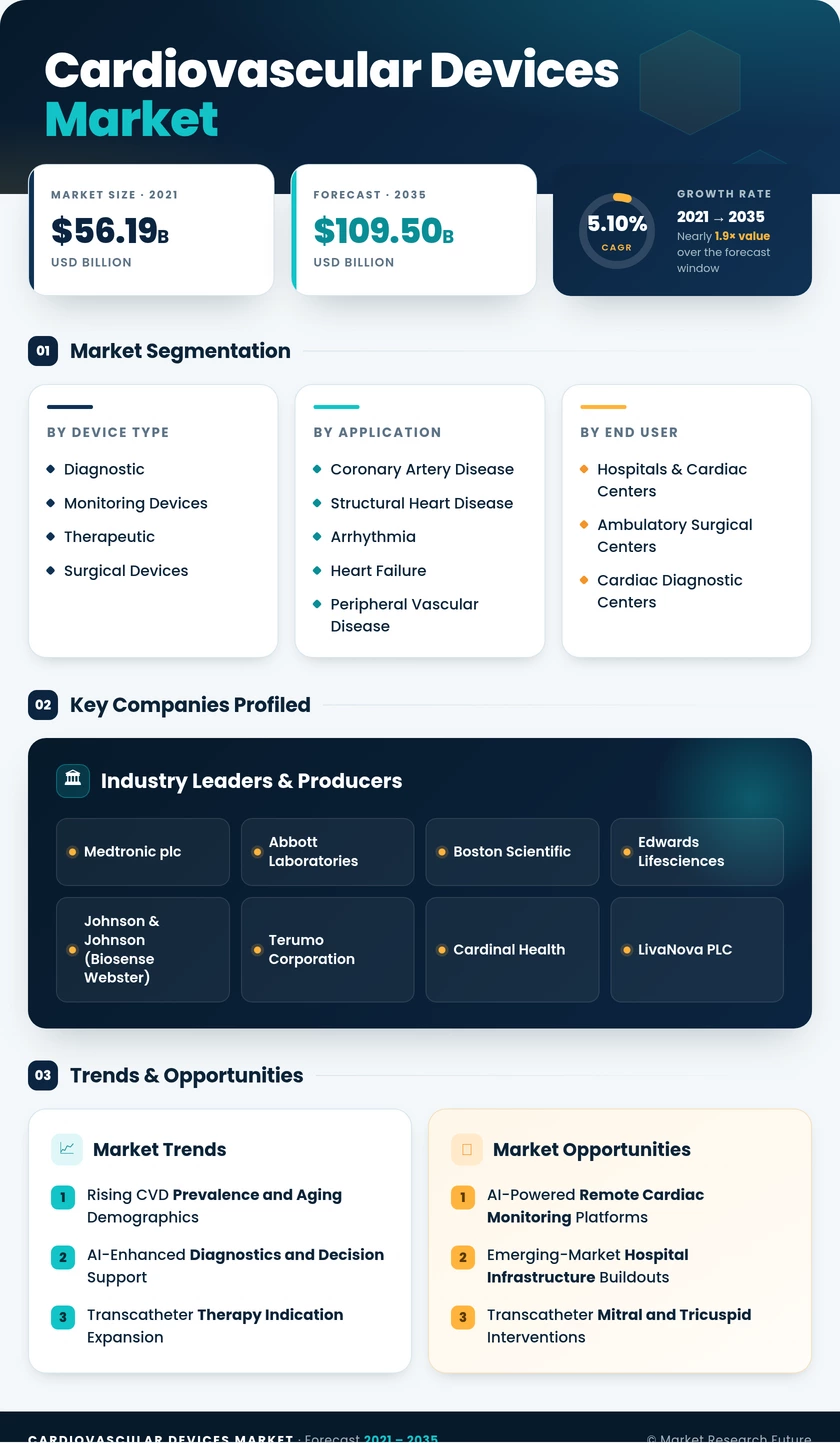

| By Device Type | Diagnostic and Monitoring Devices; Therapeutic and Surgical Devices | Diagnostic and Monitoring Devices | Therapeutic and Surgical Devices |

| By Application | Coronary Artery Disease; Structural Heart Disease; Arrhythmia; Heart Failure; Peripheral Vascular Disease | Coronary Artery Disease | Structural Heart Disease |

| By End User | Hospitals & Cardiac Centers; Ambulatory Surgical Centers; Cardiac Diagnostic Centers | Hospitals & Cardiac Centers | Ambulatory Surgical Centers |

| By Region | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Device Type

| Sub-Segment | Key Trend |

| Diagnostic and Monitoring Devices | AI-algorithm integration driving upgrade cycles; portable ultrasound and wearable ECG proliferation |

| Therapeutic and Surgical Devices | Transcatheter valve expansion, leadless pacing, bioresorbable scaffolds entering pivotal trials |

Diagnostic and monitoring devices encompass electrocardiography systems, echocardiography platforms, cardiac CT/MRI modules, Holter monitors, and emerging wearable rhythm sensors. The segment benefits from recurring software-upgrade revenue as AI compatibility becomes a procurement prerequisite.

By Application

| Sub-Segment | Key Trend |

| Coronary Artery Disease | Drug-eluting stent evolution and physiology-guided PCI adoption |

| Structural Heart Disease | Transcatheter aortic, mitral, and tricuspid device pipelines maturing |

| Arrhythmia | Pulsed-field ablation and next-generation leadless pacemakers |

| Heart Failure | LVAD miniaturization and implantable hemodynamic sensors |

| Peripheral Vascular Disease | Drug-coated balloons and atherectomy innovation |

Coronary artery disease dominates by revenue, but structural heart disease offers the highest growth trajectory as transcatheter therapies achieve regulatory clearance across progressively lower-risk patient populations.

By End User

| Sub-Segment | Key Trend |

| Hospitals & Cardiac Centers | Hybrid OR buildouts and cath-lab volume consolidation |

| Ambulatory Surgical Centers | CMS procedure-list expansion enabling outpatient cardiac interventions |

| Cardiac Diagnostic Centers | Decentralized screening and AI-enabled remote interpretation |

Hospitals remain the primary setting for complex cardiovascular interventions, but ambulatory surgical centers are the fastest-growing channel as reimbursement policies and lower-profile device designs enable same-day discharge for an expanding procedure set.