China Electric Vehicle Market Summary

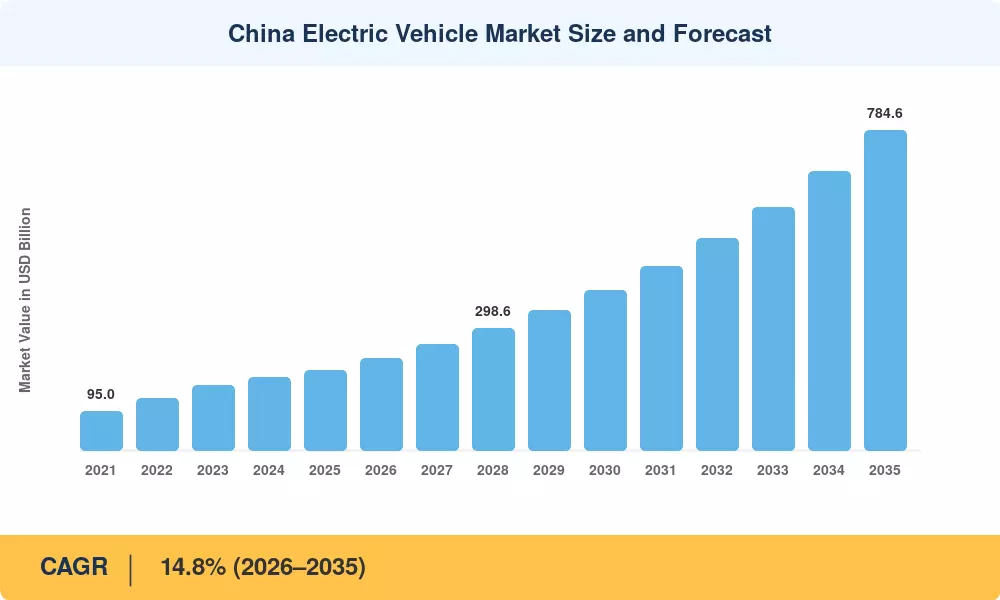

The China Electric Vehicle Market reached an estimated USD 197.3 billion in 2025, positioning the country as the single largest electric vehicle ecosystem on the planet. From a 2026 forecast starting point of USD 226.5 billion, the China Electric Vehicle Market is projected to expand at a compound annual growth rate of 14.8% through 2035, reaching USD 784.6 billion by the end of the forecast period. This trajectory is anchored in Beijing's dual-carbon goals — peak carbon by 2030, carbon neutrality by 2060 — and the State Council's New Energy Vehicle Industry Development Plan (2021–2035), which mandates that NEVs account for 50% of all new vehicle sales by 2035 [1]. Provincial purchase incentives, license-plate lottery exemptions in megacities, and aggressive charging-station rollout targets collectively underpin sustained demand.

A technological transformation is well underway. Internal combustion engine platforms that dominated Chinese roads for three decades are rapidly being displaced by battery-electric and plug-in hybrid architectures built on dedicated EV-native platforms. CATL's Qilin battery and BYD's Blade Battery have pushed pack-level energy density past 200 Wh/kg, while cumulative battery manufacturing capacity across China exceeded 1,500 GWh in 2024 [2]. The Ministry of Industry and Information Technology channeled over CNY 180 billion in NEV-related subsidies between 2015 and 2023 before pivoting to tax-exemption mechanisms, ensuring a smooth transition from direct subsidy to market-driven adoption [3].

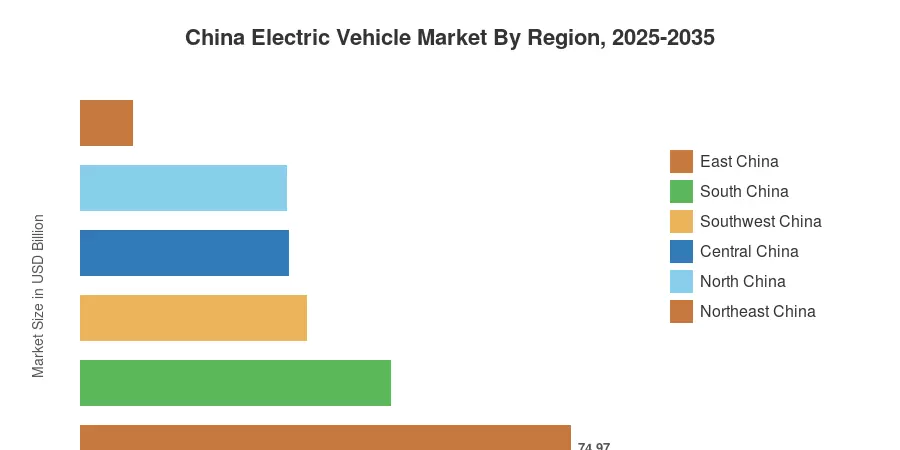

East China — led by Shanghai, Jiangsu, and Zhejiang — commands roughly 38% of the China Electric Vehicle Market, buoyed by OEM headquarters clusters and Tier-1 supplier concentration. Southwest China is the fastest-growing region, posting a CAGR of approximately 17.5% as Chongqing and Chengdu scale production capacity. South China, anchored by Guangdong's BYD-Shenzhen nexus, accounts for about 24% of domestic EV revenue. As battery costs continue declining and provincial governments accelerate rural electrification, the China Electric Vehicle Market is poised for a decade of structural expansion that will reshape global automotive supply chains.

Key Report Takeaways

• By Vehicle Type

- Battery Electric Vehicles (BEVs) hold approximately 72% share of the China Electric Vehicle Market, driven by declining pack costs and range improvements above 600 km

- Plug-in Hybrid Electric Vehicles (PHEVs) are registering a CAGR of 18.3%, the fastest among vehicle types, as range-anxiety-conscious buyers in Tier-3 and Tier-4 cities prefer dual-powertrain flexibility

- Fuel Cell Electric Vehicles (FCEVs) are valued at approximately USD 4.1 billion in 2025, concentrated in heavy-duty trucking corridors across northern provinces

• By Application

- Passenger vehicles represent roughly 82% of the China Electric Vehicle Market by revenue, reflecting mass-market adoption of compact and midsize BEVs

- Commercial vehicles — buses, logistics vans, and medium-duty trucks — are growing at a CAGR of 16.2%, supported by municipal fleet electrification mandates

• By Region

- East China leads with a 38% share, powered by manufacturing density along the Yangtze River Delta

- Southwest China is expanding at the fastest CAGR of 17.5% as Sichuan and Chongqing invest in lithium processing and assembly capacity

- South China contributes approximately USD 47.4 billion in 2025, anchored by Guangdong's vertically integrated EV supply chain

Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates bottom-up OEM shipment data from the China Association of Automobile Manufacturers (CAAM), top-down macroeconomic indicators from the National Bureau of Statistics, and proprietary pricing surveys across 28 provincial markets. Historical figures (2021–2024) rely on audited industry filings, while the forecast (2026–2035) applies a regression-adjusted growth model calibrated to battery cost trajectories, policy timelines, and infrastructure deployment curves.