Chronic Obstructive Pulmonary Disease (COPD) Market Summary

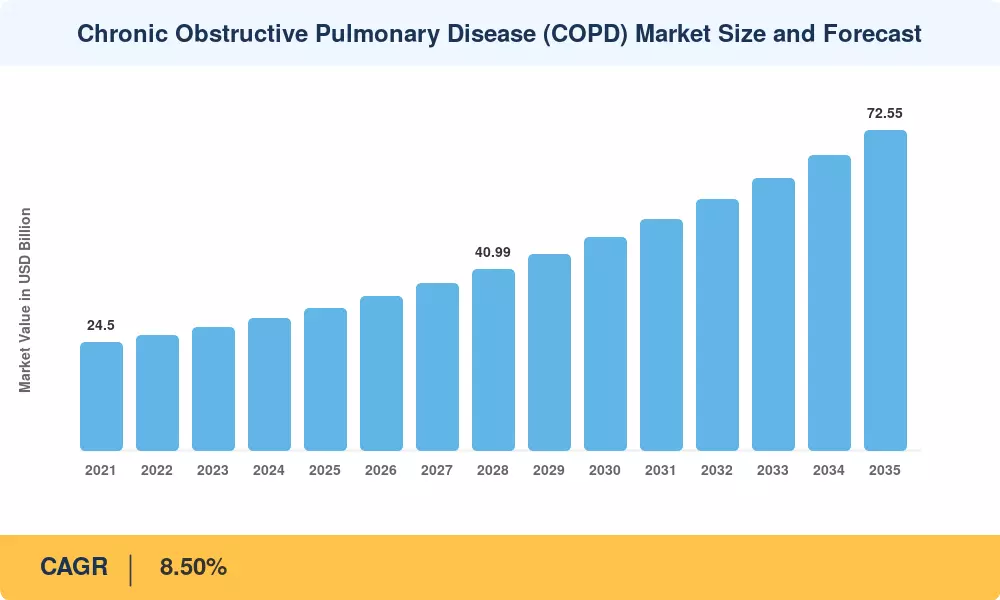

The global Chronic Obstructive Pulmonary Disease Market reached an estimated USD 32.10 Billion in 2025 and is projected to grow from USD 34.82 Billion in 2026 to USD 72.55 Billion by 2035, registering a CAGR of 8.50% over the forecast period (2026–2035). Rising disease prevalence among aging populations, expanded Medicare reimbursement for home-based respiratory care, and the accelerated adoption of triple-combination inhalers are the primary catalysts behind this trajectory. The WHO's 2024 Global Burden of Disease update estimates that COPD affects more than 480 million adults globally, and public-health spending directed at chronic respiratory diseases exceeded USD 14 billion across OECD countries in fiscal year 2024 [1].

A significant technology transformation is reshaping how clinicians manage the Chronic Obstructive Pulmonary Disease Market. Legacy metered-dose inhalers using high-GWP propellants are giving way to low-GWP reformulations and smart connected devices that generate real-world adherence data. The European Commission's F-gas Regulation phase-down, effective through 2030, is compelling manufacturers to invest over USD 2 billion collectively in inhaler redesigns [2]. Simultaneously, first-in-class biologics targeting eosinophilic COPD phenotypes — including dupilumab and itepekimab — are entering late-stage regulatory review, creating entirely new therapeutic sub-segments within the Chronic Obstructive Pulmonary Disease Market.

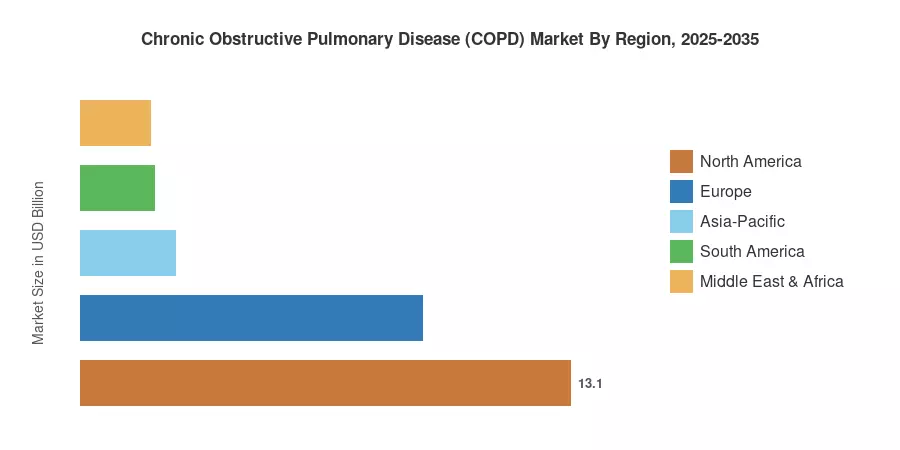

North America leads the Chronic Obstructive Pulmonary Disease Market with approximately 40.80% revenue share, driven by robust insurance reimbursement and high diagnostic penetration. Asia-Pacific is the fastest-growing region at an estimated 7.90% CAGR through 2035, as China and India scale primary-care spirometry infrastructure. Europe holds the second-largest share at roughly 28.50%, supported by EU Pharmaceutical Strategy incentives for respiratory innovation. The competitive landscape will intensify as biosimilar long-acting bronchodilators reach formulary by 2028.

Key Report Takeaways

• By Product Type

- Drug Class therapies commanded approximately 69.50% of the Chronic Obstructive Pulmonary Disease Market share in 2024, reflecting strong uptake of fixed-dose LABA/LAMA/ICS combinations.

- Consumables & Accessories are forecast to expand at an 8.00% CAGR through 2035, fueled by recurring replacement cycles for nebulizer kits and spacer devices.

- Monitoring Devices reached USD 2.85 Billion in 2024, propelled by remote patient monitoring reimbursement codes introduced by CMS.

• By End User

- Hospitals and clinics accounted for roughly 83.30% of the Chronic Obstructive Pulmonary Disease Market revenue in 2024.

- Homecare settings are projected to register a 7.30% CAGR through 2035 as payers shift acute exacerbation management to outpatient and home-based models.

• By Region

- North America captured 40.80% of the Chronic Obstructive Pulmonary Disease Market in 2024, underpinned by Medicare Part D coverage expansion.

- Asia-Pacific is projected to record the fastest growth at 7.90% CAGR through 2035.

- Europe contributed an estimated USD 9.15 billion in 2024, with Germany and the UK as leading national markets.

Chronic Obstructive Pulmonary Disease Market Size and Forecast (2021–2035)

Market sizing follows a bottom-up revenue model aggregating manufacturer-reported sales across drug classes, diagnostic devices, monitoring devices, and consumables. Historical figures (2021–2024) draw from annual reports, national health expenditure databases, and prescription audit datasets from IQVIA and MIDAS. Forecast projections (2026–2035) apply segment-level growth assumptions validated against epidemiological prevalence models and payer-mix scenarios [3].