Clean Beauty Market Summary

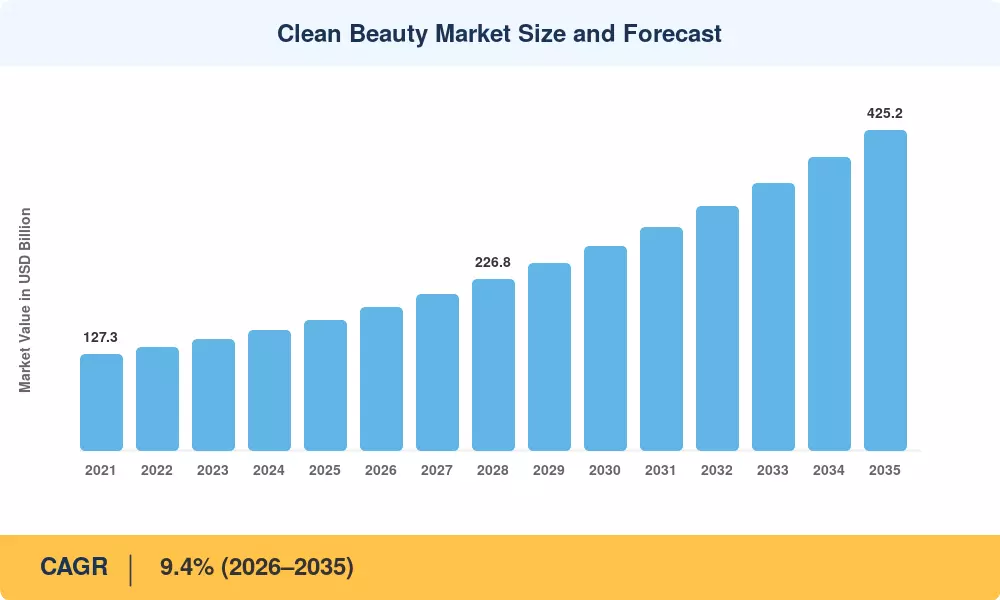

The Clean Beauty Market was valued at USD 173.20 billion in 2025 and is projected to reach USD 189.50 billion in 2026, climbing to USD 425.20 billion by 2035 at a CAGR of 9.4% during the forecast period (2026–2035). This trajectory reflects a deep structural shift in how consumers interact with personal care — demanding full ingredient transparency, stringent safety standards, and verifiable sustainability claims. The passage of the FDA's Modernization of Cosmetics Regulation Act (MoCRA) in December 2022 established the first major federal overhaul of U.S. cosmetics regulation in over 80 years, mandating facility registration, product listing, and adverse event reporting. That regulatory anchor, combined with the EU's tightening of its Cosmetics Regulation (EC No 1223/2009) banning over 2,000 substances, has accelerated reformulation investment across the industry [1][2].

The emergence of biotech-derived alternatives, plant-derived actives and upcycled component platforms is replacing legacy formulation paradigms predicated on synthetic preservatives, parabens and sulfates. The global investment in green chemistry was predicted at USD 16.2 billion in 2024, of which personal care represented around 18% of the capital [3]. Brands are redirecting R&D investments into fermentation-derived retinol replacements, microbiome-friendly surfactants, and waterless concentrate formulations that address efficacy and environmental impact concurrently.

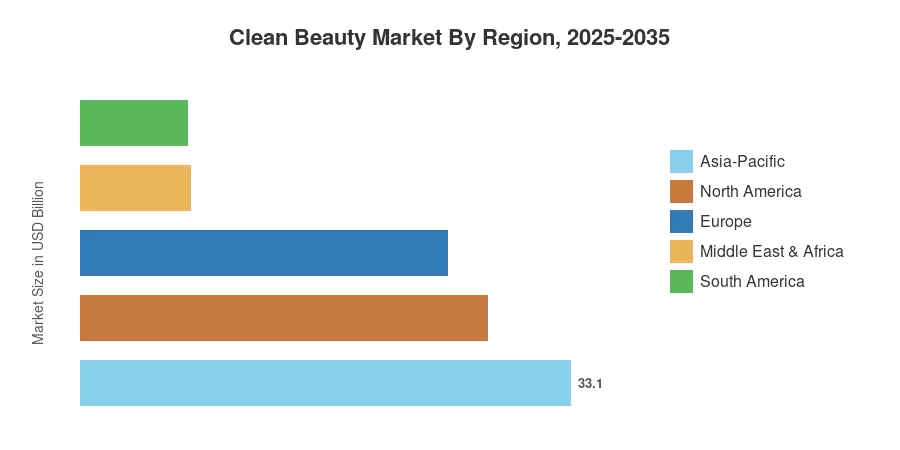

The Asia-Pacific region is the greatest contributor to the Clean Beauty Market, with over 33.1% of the global revenue share in 2025. The growth is driven by premiumization tendencies in China and a quick increase in demand in India’s tier-2 and tier-3 cities. Next is North America with a 27.5% share, driven by MoCRA compliance spending and the development of DTC brands, and Europe follows at 24.8%, spurred by the EU Green Deal’s circular-economy objectives [4]. The path to profoundly changing beauty commerce is being paved by biotech innovation, digital-first distribution and regulatory convergence, as they continue to drive worldwide acceptance through 2035.

Key Report Takeaways

• By Product Type

- Skincare captured an estimated 36.4% of the Clean Beauty Market revenue in 2025, maintaining its position as the largest product category.

- Make-Up and Colour Cosmetics are projected to register a CAGR of 13.1% through 2035, fueled by social media influence and biotech pigment innovation

• By End User

- The kids category is advancing at a 14.0% CAGR through 2035, supported by parental demand for gentle, certified-safe formulations

• By Geography

- Asia-Pacific leads the Clean Beauty Market with 33.1% share in 2025 and is poised to record the fastest growth at a 13.0% CAGR

- North America holds the second-largest position with 27.5% share, supported by regulatory modernization under MoCRA

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) forecasts are based on a triangulated methodology integrating primary industry interviews (150+ stakeholders), regulatory filings, trade association data, and proprietary econometric modeling. Historical data are based on confirmed industry revenues; future estimates are based on the calibrated 9.4% CAGR adjusted for the regulatory, macroeconomic and technological adoption curves across all five areas.

.webp?v=1783952168)