Clean Coal Technology Market Summary

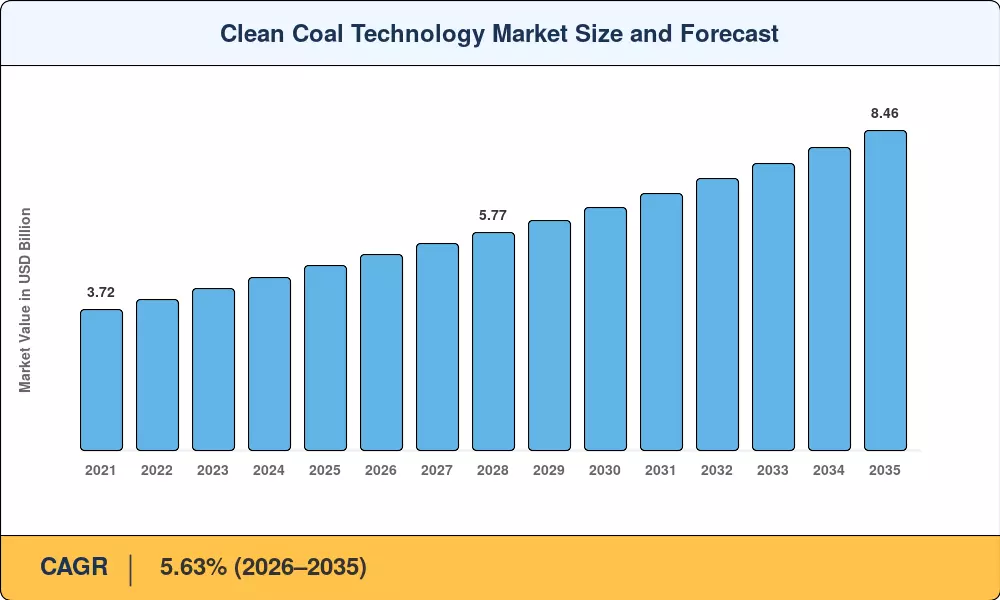

The Clean Coal Technology Market reached an estimated USD 4.89 Billion in 2025 and is projected to grow from USD 5.17 Billion in 2026 to USD 8.46 Billion by 2035, registering a CAGR of 5.63% during the forecast period. Tightening emission regulations across both OECD and non-OECD economies — including the expanded U.S. 45Q tax credit worth up to USD 85 per ton of sequestered CO₂ and the EU Emissions Trading System carbon price exceeding EUR 70 per ton — are channeling capital toward cleaner coal combustion and post-combustion capture systems [1][2].

A generational shift in coal-fired power infrastructure is well underway. Legacy subcritical units, which still account for roughly 40% of the global coal fleet, are being replaced or retrofitted with supercritical and ultra-supercritical boilers that push thermal efficiencies beyond 45%. The International Energy Agency estimates that converting all subcritical plants to high-efficiency, low-emissions technology could cut global CO₂ output by 2 gigatons annually [3]. Meanwhile, carbon capture, utilization, and storage retrofits are extending the economic life of mid-age plants that would otherwise face early retirement, unlocking an estimated USD 12–18 Billion in avoided stranded-asset losses across Asia and North America through 2035 [4].

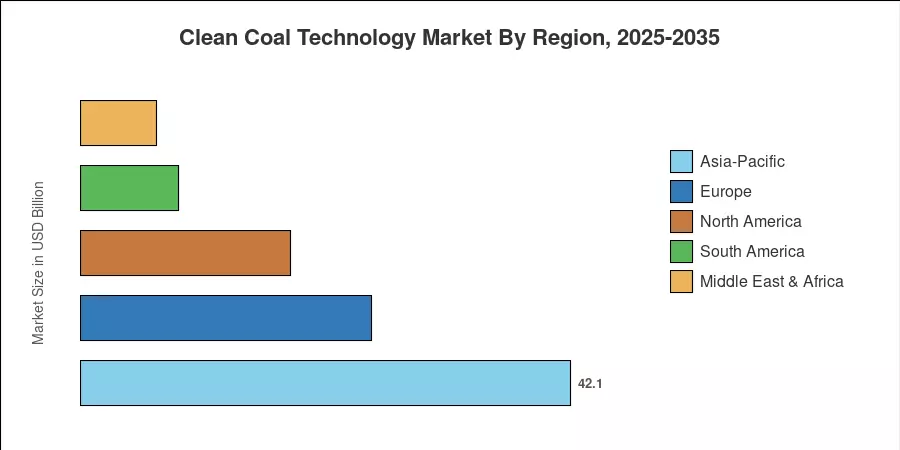

From a geographic standpoint, the Clean Coal Technology Market is anchored by Asia-Pacific, which commanded approximately 42.1% of global revenue in 2025, driven by aggressive coal fleet modernization programs in China and India. North America is on track to post the fastest regional CAGR of 7.47% between 2026 and 2035, supported by federal incentive structures and industrial decarbonization mandates. Europe held the second-largest share at roughly 25.0%, where EU taxonomy rules continue to push remaining coal assets toward capture-ready configurations [5]. The decade ahead will hinge on how quickly financing mechanisms scale to match the technical readiness of next-generation combustion and capture systems.

Key Report Takeaways

• By Technology

- Supercritical systems held approximately 47.5% of the Clean Coal Technology Market in 2025, reflecting broad adoption across Asian and European coal fleets.

- Ultra-supercritical technology is expected to record a CAGR of 15.8% through 2035, making it the fastest-growing combustion segment.

- Circulating fluidized bed combustion is gaining traction in industrial co-firing applications, with demand rising steadily in cement and chemicals end-use verticals.

• By Component

- Equipment accounted for 76.2% of the Clean Coal Technology Market share in 2025, encompassing boilers, turbines, and emissions-control hardware.

- Services — including engineering, procurement, construction, and maintenance — are forecast to expand at an 8.55% CAGR through 2035 as the installed base grows.

• By End-User

- Power utilities represented 78.8% of the Clean Coal Technology Market in 2025, underscoring the sector's dependence on grid-scale coal generation.

- Iron and steel applications are projected to register the fastest end-user growth at a 9.05% CAGR, fueled by blast-furnace emission reduction mandates.

• By Region

- Asia-Pacific led global revenue with a 42.1% share in 2025, anchored by fleet expansion in China and India.

- North America is forecast to post the highest regional CAGR at 7.47% between 2026 and 2035.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework combines bottom-up plant-level capacity analysis, import-export trade data for key combustion and capture equipment, and validated secondary research from government energy agencies, OEM annual filings, and multilateral development bank project databases.