Confectionery Ingredients Market Summary

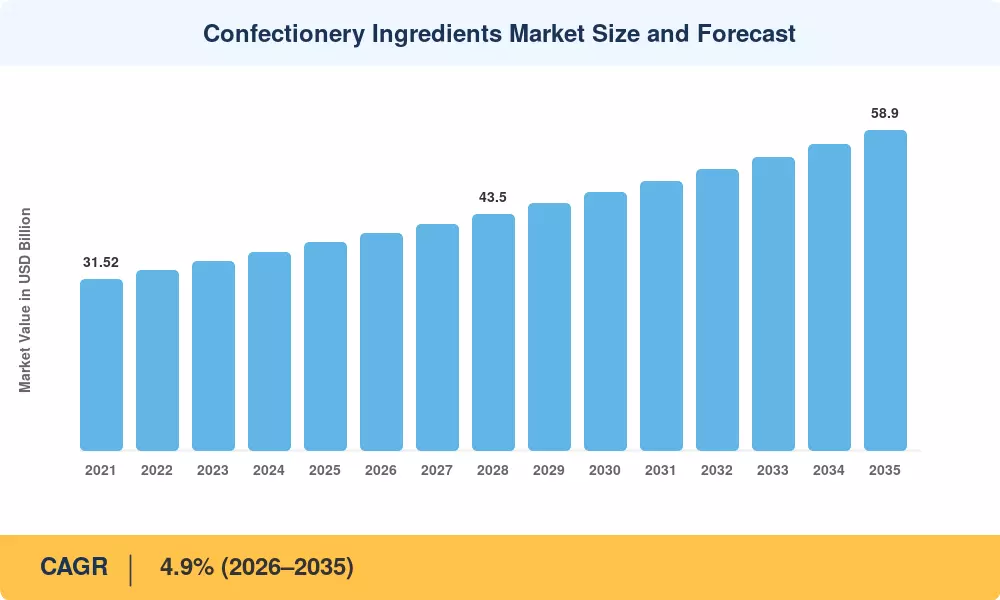

The global Confectionery Ingredients Market reached an estimated USD 38.2 billion in 2025, with forecast-period revenues starting at USD 40.1 billion in 2026 and climbing to USD 58.9 billion by 2035 at a compound annual growth rate of 4.9%. Two catalysts anchor this trajectory: rising per-capita chocolate and sugar confectionery consumption across emerging economies and an accelerating reformulation wave driven by clean-label regulations in the EU and North America [2]. Governments in more than 30 countries have now implemented or proposed sugar-reduction levies, pushing confectionery manufacturers toward functional confectionery additive solutions and next-generation sweetener blends that maintain indulgence while meeting new nutritional thresholds [3].

The ingredient supply chain itself is undergoing a quiet transformation. Traditional commodity-grade cocoa butter chocolate couverture is steadily giving way to traceable, single-origin couverture systems backed by blockchain provenance platforms. Barry Callebaut's USD 125 million "Generation Cocoa" program and Cargill's sustainable-sourcing pledge illustrate how upstream investment is reshaping what downstream confectioners can offer [4]. Sugar confectionery texture agents — hydrocolloids, modified starches, and pectin — are also seeing reformulation, as manufacturers pursue vegan-friendly gelling systems to replace gelatin in gummies and jellies .

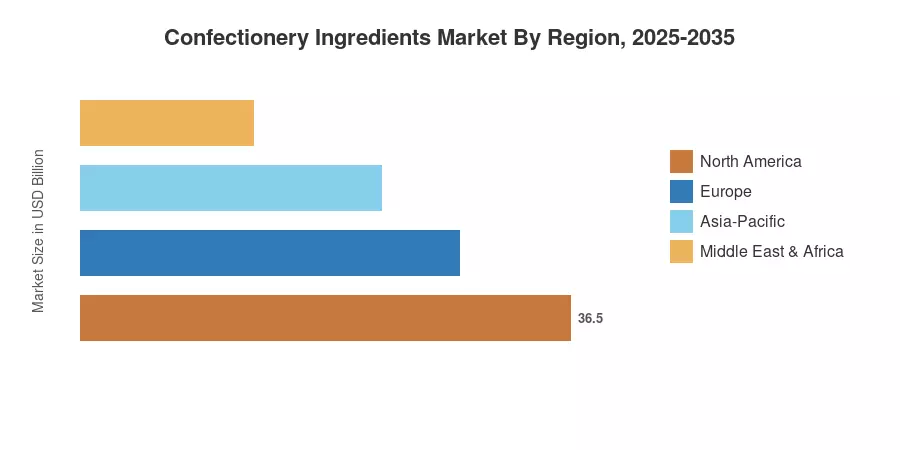

Europe commands the largest slice of the Confectionery Ingredients Market, holding roughly 33% of 2025 revenues, anchored by Switzerland, Germany, and Belgium's concentration of premium chocolate production. Asia-Pacific is the fastest-growing region at a 6.3% CAGR, fueled by expanding middle-class demand in China and India for branded chocolate and sugar confectionery. North America accounts for approximately 28% of the global market, with the United States driving demand for confectionery flavor ingredient innovation in seasonal and limited-edition product lines. The decade ahead will reward suppliers that can simultaneously deliver indulgence, transparency, and nutritional optimization.

Key Report Takeaways

• By Ingredient Type

- Cocoa and chocolate ingredients (including cocoa butter chocolate couverture and cocoa powder) held the largest revenue share at ~38% in 2025, driven by premiumization and bean-to-bar trends

- Sugar confectionery texture agents are forecast to grow at a 5.4% CAGR through 2035, reflecting accelerated demand for plant-based gelling agents in gummy and marshmallow formats

- Confectionery flavor ingredient revenues surpassed USD 4.8 billion in 2025 as limited-edition and exotic flavor profiles proliferated across global product launches

• By Application

- Chocolate confectionery applications represent USD 15.6 billion in ingredient demand, anchored by Western European and North American consumption

- Sugar-boiled and gummy confectionery applications are expanding at 5.7% CAGR, the fastest among application segments in the Confectionery Ingredients Market

• By Region

- Europe dominates at ~33% market share, with Germany alone accounting for over 9% of global ingredient consumption

- Asia-Pacific's 6.3% CAGR makes it the fastest-growing region in the Confectionery Ingredients Market, with China and India as the primary engines

- North America holds ~28% share, underpinned by strong private-label confectionery growth and functional confectionery additive adoption

Market Size and Forecast (2021–2035)

MRFR's market-sizing methodology triangulates top-down revenue estimates from ingredient-supplier financials with bottom-up demand modeling across 12 confectionery sub-categories in 45 countries. Historical data (2021–2024) derives from trade databases, customs records, and disclosed company revenues; forecast values (2026–2035) apply a blended econometric-demand model calibrated to GDP per-capita growth, sugar-levy adoption rates, and cocoa commodity price projections[7].

.webp?v=1782888035)