Crime Risk Report Market Summary

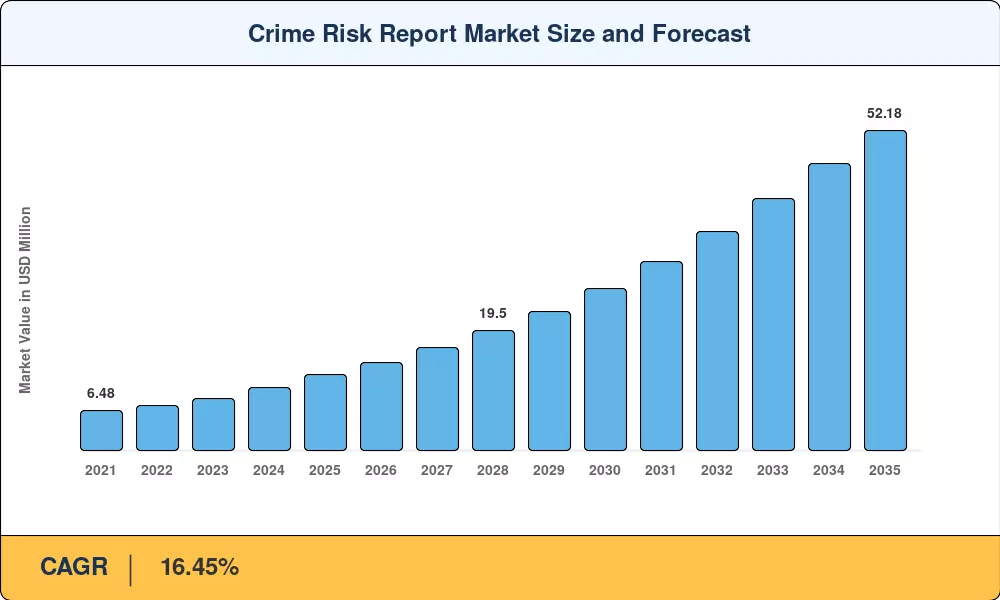

The crime risk report market was valued at USD 12.42 billion in 2025 and is projected to reach USD 14.38 billion in 2026 before climbing to USD 52.18 billion by 2035, registering a CAGR of 16.45% across the forecast window. This acceleration traces directly to FinCEN's December 2025 mandate requiring anti-money-laundering disclosures on non-financial residential property transfers, a rule that pulls title agents, escrow firms, and property platforms into a compliance perimeter once reserved for banks [1]. Cumulative AML penalties exceeding USD 362 billion levied on global financial institutions since 2019 have made the cost of inaction untenable, channeling capital toward AI-native surveillance and crime risk scoring for property underwriting tools that slash manual case reviews.

Legacy rule-based transaction monitoring is giving way to graph-analytics engines and real-time crime risk data API for real estate platforms that ingest structured and unstructured feeds simultaneously. Cloud-native architectures now handle watch-list screening in under five milliseconds while cutting false positives by roughly 60%, a performance threshold that on-premise mainframes cannot match [4]. Predictive crime mapping analytics capabilities fuse satellite imagery, demographic shifts, and historical incident records to generate block-level threat assessments, reshaping how insurers and lenders price exposure.

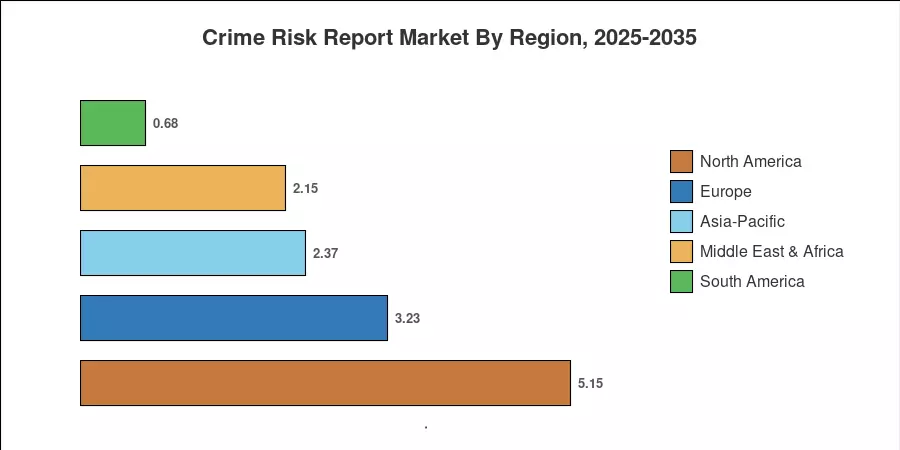

North America commands approximately 41.5% of 2025 revenue, anchored by U.S. federal spending on domestic semiconductor capacity that strengthens the hardware backbone powering geospatial crime analysis for insurers' workloads. Asia-Pacific is the fastest-growing corridor at an estimated 19.1% CAGR, propelled by Australia's plan to extend AML/CTF obligations to nearly 80,000 additional businesses from July 2026 [3]. Europe holds the second-largest share, driven by GDPR-compliant location-based crime risk intelligence data platforms gaining traction across the EU's insurance sector. The crime risk report market is poised for a decade of structural expansion as regulatory mandates, cloud migration, and AI adoption converge.

Key Report Takeaways

• By Component

- Software platforms captured the dominant revenue position in 2025 within the crime risk report market, reflecting the shift toward API-driven detection stacks that integrate predictive crime mapping analytics modules natively

- Consulting and managed services are projected to grow at a 19.5% CAGR through 2035 as banks outsource model governance and regulatory certification to specialized partners

• By Deployment

- Cloud-based deployment accounted for 69.2% of the crime risk report market in 2025, fueled by elastic compute that supports real-time crime risk data API for real estate platforms and digital-wallet authorization

- On-premise configurations retain relevance for institutions bound by data-sovereignty statutes, though share erosion continues

• By End-User Industry

- Banking institutions held the largest end-user share in 2025, driven by statutory SAR-filing deadlines and enforcement actions

- Insurance is the fastest-growing vertical, expanding at approximately 18.7% CAGR as geospatial crime analysis for insurers becomes integral to usage-based policy pricing

• By Region

- North America contributed USD 5.16 billion of 2025 revenue, while Asia-Pacific is pacing at the highest regional CAGR through 2035

MRFR's sizing methodology triangulates top-down revenue analysis from public filings and regulatory spend data with bottom-up vendor surveys across 42 countries. Historical figures (2021–2024) reflect audited industry revenues; base-year 2025 values incorporate Q4 regulatory catalysts; and forecast estimates (2026–2035) apply a calibrated compound growth model validated against macroeconomic and policy scenarios.