Diabetes Drug Market Summary

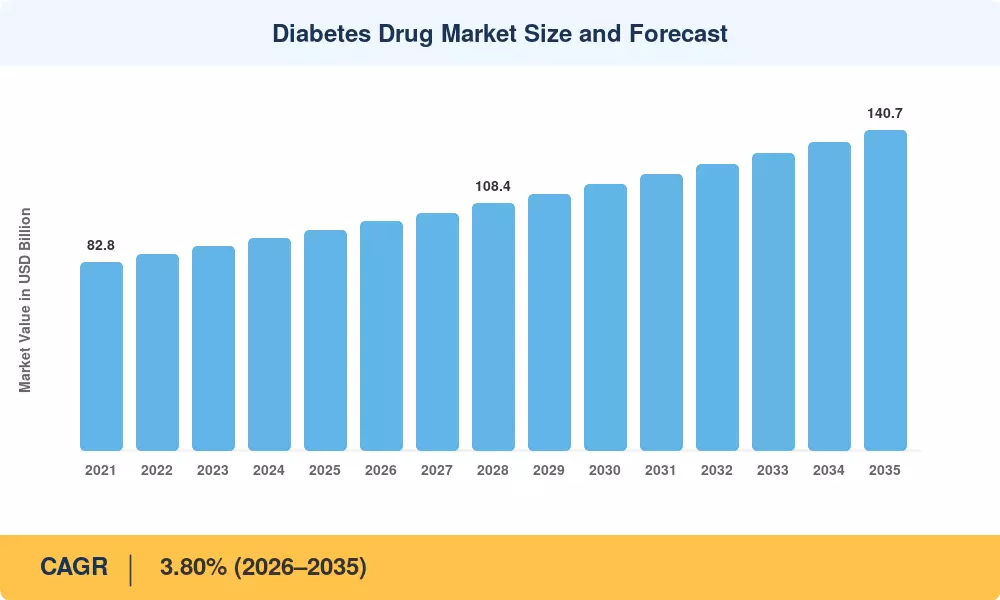

The Diabetes Drug Market size was valued at USD 96.90 Billion in 2025, and the market is projected to grow from USD 100.60 Billion in 2026 to USD 140.70 Billion by 2035, registering a CAGR of 3.80% during the forecast period 2026–2035. Two structural forces are propelling this trajectory: the U.S. Inflation Reduction Act's Medicare drug-price negotiation provisions, which are reshaping manufacturer pricing strategies across the insulin portfolio, and the International Diabetes Federation's projection that global diabetes prevalence will surpass 850 million adults before 2050 [1]. Together, these catalysts are locking in durable volume growth while compressing average selling prices in mature economies.

A pronounced therapeutic shift is underway within the Diabetes Drug Market. Legacy sulfonylureas and older basal insulin formulations are steadily losing ground to newer dual-incretin co-agonists and next-generation long-acting analogs. Novo Nordisk, Eli Lilly, and Sanofi collectively committed more than USD 16 billion in manufacturing capacity expansion between 2023 and 2025 to address persistent supply shortages of injectable therapies [2]. Regulatory bodies in the EU and Japan have fast-tracked biosimilar approvals, intensifying price competition across subcutaneous delivery formats.

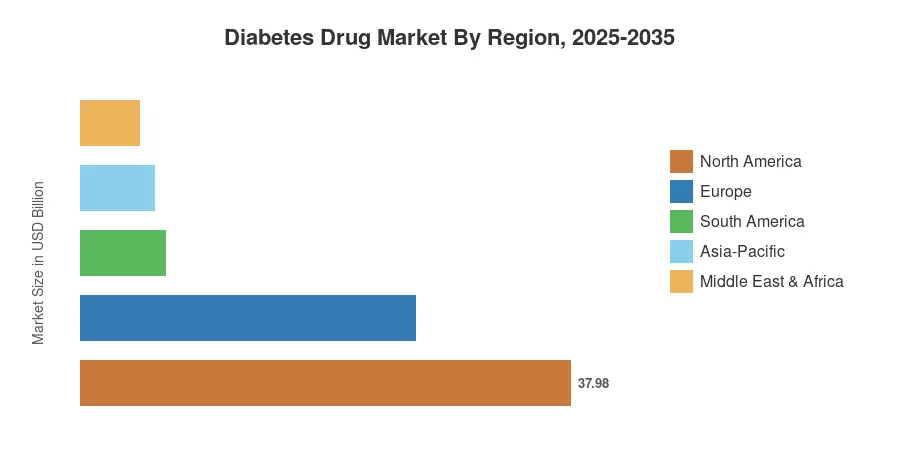

North America held a 39.2% share of the Diabetes Drug Market in 2025, anchored by high per-capita spending and broad commercial insurance coverage for branded therapies. Asia-Pacific represents the fastest-growing region at a 5.95% CAGR through 2035, driven by nationwide screening programs in China and India that are converting undiagnosed populations into treated patients. Europe retains the second-largest position with a 26.8% share, supported by centralized reimbursement frameworks. The next decade will reward manufacturers that balance premium innovation with accessible pricing in emerging markets.

Key Report Takeaways

• By Drug Class

- Insulin accounted for 52.6% of the Diabetes Drug Market in 2025, reflecting entrenched prescribing patterns in Type 1 and advanced Type 2 diabetes management.

- Non-insulin injectable drugs are forecast to grow at a 4.55% CAGR through 2035, buoyed by cardiovascular and renal outcome trial evidence favoring incretin-based therapies.

- Combination drugs are gaining formulary traction across Europe as payers push for fixed-dose regimens that improve adherence.

• By Route of Administration

- Subcutaneous delivery captured 66.5% of the Diabetes Drug Market in 2025, underscoring the dominance of injectable insulin and pen-based therapies.

- Oral administration is projected to expand at a 5.24% CAGR to 2035 as oral semaglutide and emerging oral biologics gain share.

• By Distribution Channel

- Hospital pharmacies represented 36.3% of revenue in 2025, although digital pharmacy platforms are eroding traditional channel dominance.

- Online pharmacies constitute the fastest-growing channel at a 6.28% CAGR, led by transparent cash-pay pricing models in the United States.

• By Region

- North America commanded 39.2% of the Diabetes Drug Market in 2025, driven by premium pricing and large employer-sponsored insurance pools.

- Asia-Pacific is set to expand at a 5.95% CAGR through 2035, propelled by government-led diabetes screening drives across China, India, and the Gulf states.

Market Size and Forecast (2021–2035)

Data in this section draws on a triangulated methodology combining manufacturer revenue disclosures, prescription-volume audits from IQVIA and government health-expenditure databases, and proprietary primary interviews with hospital procurement directors and payer formulary committees.