Digital Holography Market Summary

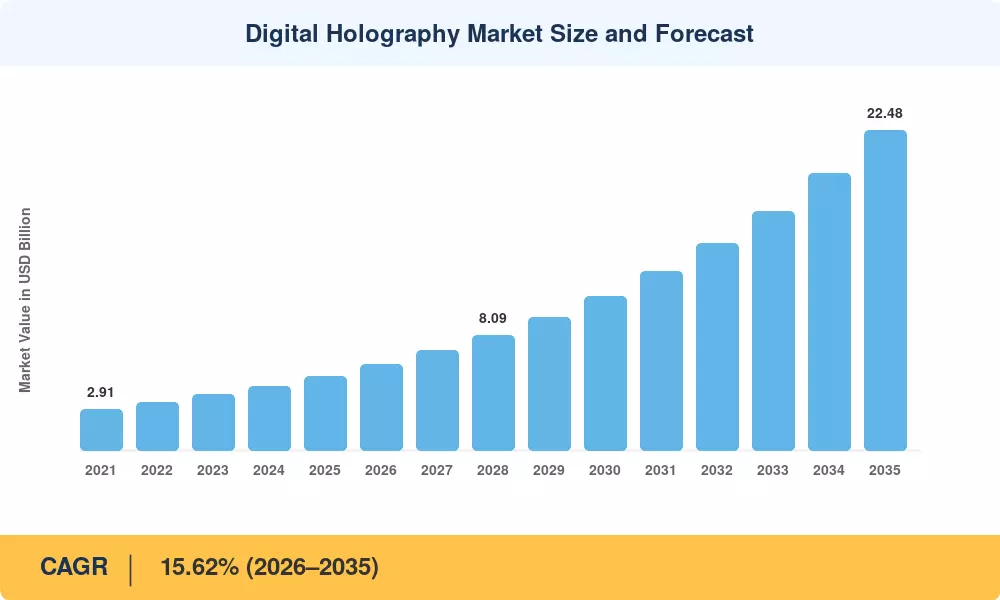

The Digital Holography Market was valued at USD 5.22 billion in 2025 and is projected to reach USD 5.97 billion in 2026 before climbing to USD 22.48 billion by 2035, registering a CAGR of 15.62% during 2026–2035. This trajectory reflects a sharp acceleration driven by defense modernization budgets — the U.S. Department of Defense allocated over USD 1.2 billion toward holographic LiDAR and situational-awareness programs across FY2024–2025 [2] — alongside expanding clinical adoption of digital holographic microscopy for research in pathology labs across Japan and South Korea [3].

A generational shift is underway as legacy 2D imaging, fluorescence-based microscopy, and mechanical head-up displays give way to coherent-light holographic optical elements for AR systems, phase-spatial light modulators for holography, and volumetric telepresence platforms. The deployment of Versatile Video Coding (H.266/VVC) slashed holographic data payloads by roughly 40%, making real-time holographic 3D display technology viable over commercial 5G networks for the first time [4]. Automakers in Germany and South Korea have signed multi-year contracts for waveguide-based holographic HUDs, pulling investment into series production lines.

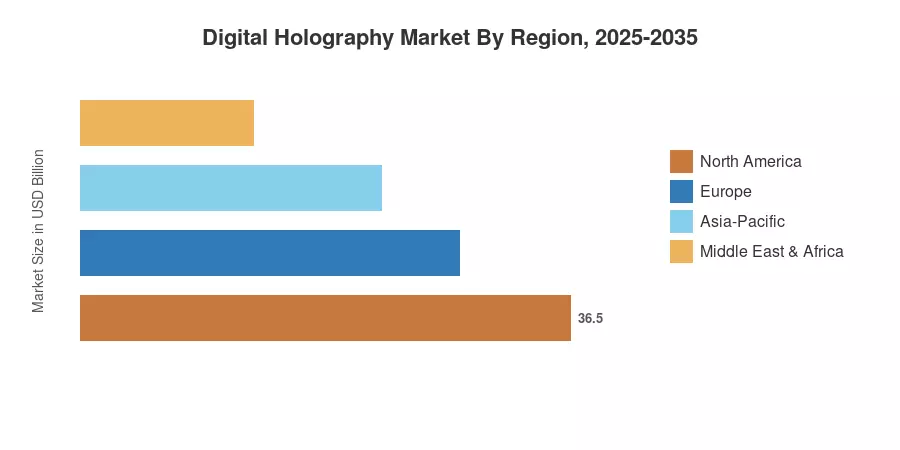

North America commands the largest share of the Digital Holography Market at approximately 44.8% of 2025 revenue, anchored by U.S. federal R&D and Silicon Valley start-up activity. Asia-Pacific is the fastest-growing region with a projected CAGR of 17.05%, fueled by Chinese retail volumetric advertising and Japanese biophotonics grants. Europe holds the second-largest position, contributing roughly 27% of global revenue through German automotive and Nordic defense programs As holographic data storage research matures and bandwidth costs fall, the Digital Holography Market is positioned to penetrate verticals that were economically inaccessible just three years ago.

Key Report Takeaways

• By Offering

- Hardware accounted for 65.5% of Digital Holography Market revenue in 2025, driven by spatial light modulator shipments and holographic display panel demand

- Software platforms are advancing at a 15.78% CAGR through 2035, as cloud-based holographic reconstruction and AI-enhanced phase-retrieval algorithms gain traction

• By Technique

- Off-axis holography led with USD 3.68 billion in 2025 revenue, reflecting its dominance in digital holographic microscopy for research and industrial metrology

- Synthetic-aperture methods are expanding fastest at a 17.56% CAGR, supported by demand for wide-field-of-view holographic optical elements for AR systems

• By Application

- Digital holographic displays captured 47.8% of the Digital Holography Market in 2025, with telepresence solutions forecast to grow at 16.28% CAGR

• By End-User Vertical

- Medical and life sciences held 33.2% share in 2025, leveraging label-free cell analysis powered by phase-spatial light modulators for holography

- The automotive sector is projected to grow at 16.62% CAGR as holographic HUD integration scales across premium and mid-tier vehicles

• By Region

- North America dominated the Digital Holography Market with 44.8% share in 2025

- Asia-Pacific is projected to rise at a 17.05% CAGR to 2035, outpacing all other regions