Digital Power Utility Market Summary

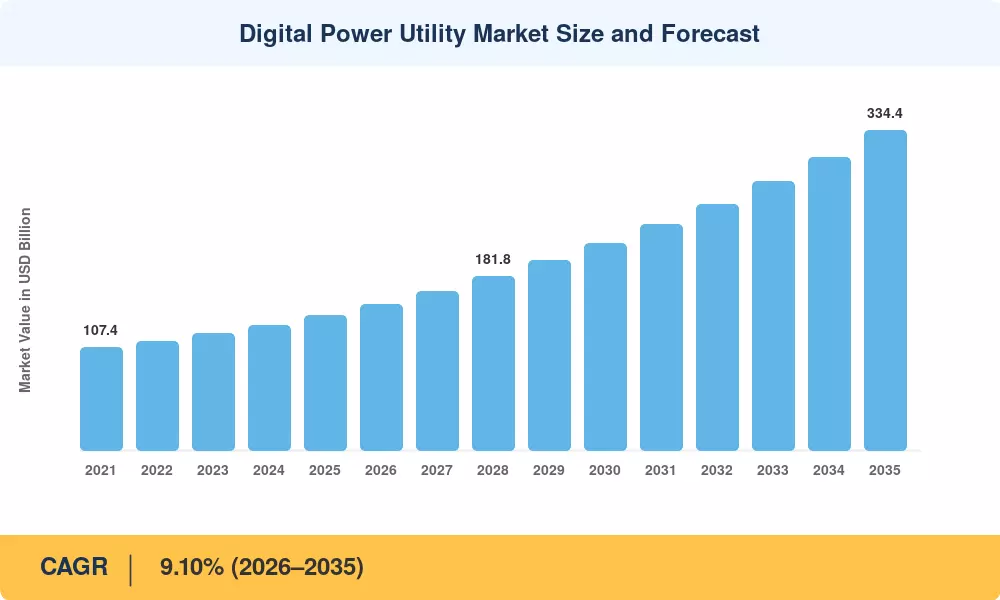

The digital power utility market was valued at USD 140.80 billion in 2025 and is projected to reach USD 152.70 billion in 2026 before climbing to USD 334.40 billion by 2035, registering a CAGR of 9.10% across the 2026–2035 forecast window. Two catalysts anchor this trajectory: the U.S. Department of Energy's USD 20.5 billion Grid Resilience and Innovation Partnerships program, which is channeling federal dollars into digitized distribution networks, and the EU's revised Energy Efficiency Directive mandating real-time consumption transparency for all member-state utilities by 2030 [1][2]. Together, these policy frameworks are converting what was once discretionary IT spending into compliance-driven capital expenditure across the digital power utility market.

Legacy SCADA architectures and manual meter-reading workflows are giving way to cloud-native platforms that fuse artificial intelligence with high-density IoT sensor arrays. Utilities that once budgeted 2–3% of revenue for technology now allocate 6–8%, a shift validated by the International Energy Agency's 2024 estimate that global grid digitalization investment surpassed USD 48 billion for the first time [3]. The result is a sector-wide pivot from reactive maintenance to predictive, data-driven operations.

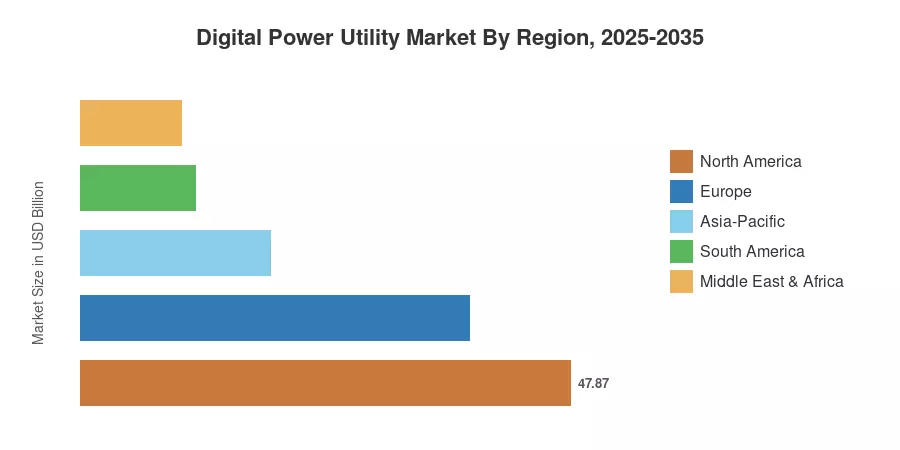

North America commands roughly 34% of the digital power utility market, supported by decades of regulatory mandates around advanced metering. Asia-Pacific is the fastest-growing region at a projected 13.20% CAGR, fueled by India's Revamped Distribution Sector Scheme and China's aggressive state-grid modernization campaigns [4]. Europe holds the second-largest share at approximately 27%, anchored by the Nordic region's near-complete rollout of second-generation smart meters. As electrification accelerates globally, the digital power utility market stands to absorb a disproportionate share of infrastructure investment through 2035.

Key Report Takeaways

• By Technology

- Integrated solutions held the leading position in the digital power utility market in 2025, commanding approximately 55% of total revenue, driven by utility demand for unified analytics-and-control platforms.

- Hardware components are expected to register a CAGR of 12.0% through 2035, propelled by mass deployments of intelligent electronic devices and communication gateways.

• By Sector

- Power generation represented roughly 43% of the digital power utility market in 2025, reflecting heavy investment in plant-level digital twins and predictive maintenance suites.

- Energy storage is poised for the fastest sectoral growth at a projected 15.30% CAGR through 2035, as battery-management software becomes integral to grid balancing.

• By Region

- North America remained the dominant geography in the digital power utility market, supported by FERC Order 2222 and state-level performance-based ratemaking incentives.

- Asia-Pacific is forecast to advance at a 13.20% CAGR between 2026 and 2035, making it the fastest-growing regional market.

Digital Power Utility Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates bottom-up revenue estimates from utility IT/OT budgets, vendor financial disclosures, and top-down macro indicators such as grid investment intensity ratios published by the IEA. Historical values (2021–2024) are reconciled against audited annual reports of the top-20 vendors, while forecast values (2026–2035) apply a calibrated compound growth rate validated against independent econometric models.