Disposable Medical Sensors Market Summary

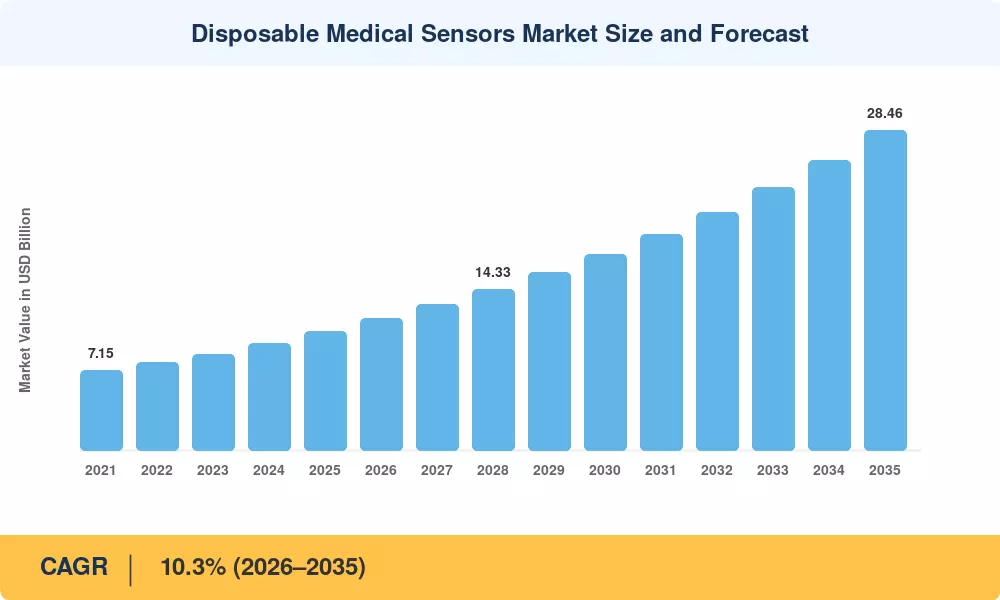

The Disposable Medical Sensors Market size was valued at USD 10.58 Billion in 2025, and the market is projected to grow from USD 11.78 Billion in 2026 to USD 28.46 Billion by 2035, registering a CAGR of 10.3% during the forecast period 2026–2035. Sustained regulatory pressure around infection prevention — highlighted by the U.S. FDA's updated Quality System Regulation amendments mandating single-use device traceability — and rising insurance reimbursement for home-based monitoring have propelled procurement budgets upward [1]. These forces are compounded by a global shift away from reusable sensors, where sterilization costs and cross-contamination risks erode long-term value.

A technological inflection point is reshaping the Disposable Medical Sensors Market. Legacy reusable electrodes and bulky wired transducers are giving way to ultra-thin, flexible printed sensor arrays built on biocompatible substrates. Governments across the EU and Asia have collectively earmarked over USD 3.2 billion in MedTech digitization grants through 2028, accelerating miniaturization and wireless connectivity in throwaway sensor platforms [2]. Biodegradable polymer substrates — still at pilot scale in 2023 — now figure in at least twelve FDA-cleared device families.

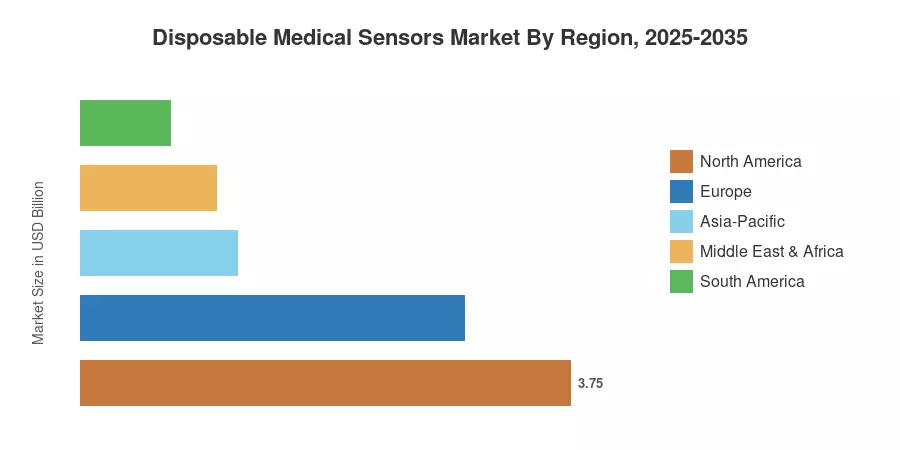

North America leads the Disposable Medical Sensors Market with an estimated 35.4% share of global revenue in 2025, driven by entrenched hospital networks and favorable reimbursement structures. Asia-Pacific stands out as the fastest-growing region at an 11.3% CAGR to 2035, fueled by India's Ayushman Bharat digital health expansion and China's tiered-hospital sensor procurement mandates [3]. Europe remains the second-largest region, anchored by Germany and France's medtech innovation ecosystems. As sustainability mandates tighten worldwide, closed-loop sensor recycling programs are poised to open entirely new revenue channels by the early 2030s.

Key Report Takeaways

• By Product

- Biosensors commanded a 44.5% revenue share of the Disposable Medical Sensors Market in 2025, benefiting from glucose and cardiac biomarker detection demand.

- Image sensors are forecast to expand at a 12.3% CAGR through 2035, driven by endoscopic and point-of-care imaging adoption.

• By Application

- Patient monitoring held a 42.8% share of the Disposable Medical Sensors Market in 2025 as telehealth utilization stabilized above pandemic-era levels.

- Diagnostics applications are projected to grow at a 12.9% CAGR to 2035, led by rapid lateral-flow and lab-on-chip platforms.

• By Technology

- MEMS-based sensors captured 39.1% of market revenue in 2025, reflecting mature fabrication ecosystems.

- Nanotechnology-enabled sensors are advancing at a 12.6% CAGR, unlocking ultra-sensitivity for trace-analyte detection.

• By End User

- Hospitals and clinics accounted for 38.9% of end-user spending in 2025.

- Home-care settings are forecast to climb at a 13.1% CAGR as remote patient monitoring reimbursement policies mature.

• By Region

- North America dominated with 35.4% of global revenue in 2025.

- Asia-Pacific is projected to witness the fastest growth at an 11.3% CAGR through 2035.

Disposable Medical Sensors Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue modeling across device categories, triangulated against hospital procurement databases, FDA 510(k) clearance volumes, and import-export trade flows from 42 countries. Historical figures are validated against published financial disclosures from leading OEMs, while forecast projections incorporate macro health-expenditure models from the WHO and OECD.