Medical Sensors Market Summary

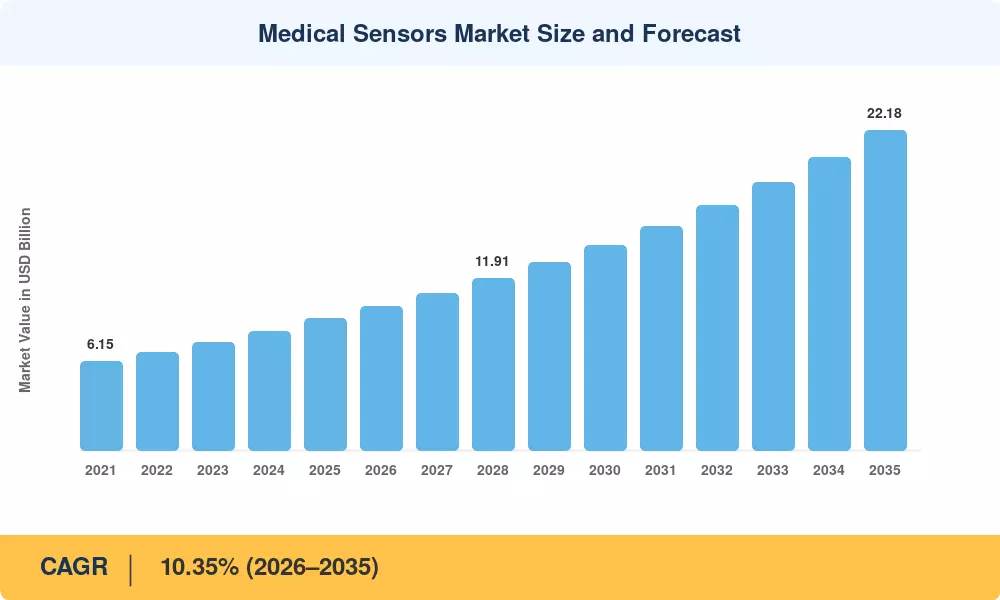

The Medical Sensors Market reached a valuation of USD 9.12 billion in 2025 and is projected to grow from USD 10.03 billion in 2026 to USD 22.18 billion by 2035, registering a CAGR of 10.35% across the forecast period (2026–2035). This expansion is anchored in accelerating demand for wearable biosensor devices that enable continuous patient vitals monitoring sensors outside hospital walls, combined with favorable reimbursement pathways established under the U.S. CMS Remote Physiologic Monitoring codes and the EU Medical Device Regulation (MDR 2017/745). The CHIPS and Science Act's USD 52.7 billion allocation for domestic semiconductor fabrication is directly benefiting clinical-grade sensing technology supply chains by reducing import dependency for MEMS wafers and fiber-optic transducers.

A fundamental technology transformation is reshaping the Medical Sensors Market as legacy single-use electrochemical strips give way to implantable physiological sensors capable of multi-analyte detection over weeks or months. AI-enabled edge analytics now process IoT health data sensor streams locally on wearable patches, cutting cloud latency and enabling real-time clinical alerts. Abbott's FreeStyle Libre 3, for instance, has demonstrated that continuous glucose monitors can replace 80% of finger-stick tests in ambulatory settings, a shift that pushed the global CGM segment past USD 8 billion in 2024.

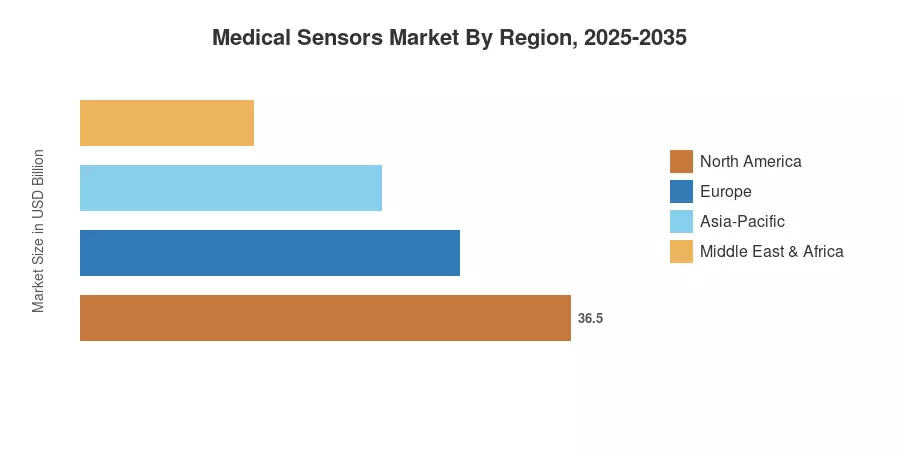

North America commanded roughly 36.5% of the Medical Sensors Market in 2025, driven by high per-capita device spending and a mature payer infrastructure. Asia-Pacific stands as the fastest-growing region with a CAGR of 14.85%, fueled by China's "14th Five-Year Plan" medical device localization push and India's Ayushman Bharat Digital Mission digitizing primary care. Europe holds the second-largest share at approximately 27.8%, with Germany and France leading the adoption of patient vitals monitoring sensors in telehealth platforms.

Key Report Takeaways

By Sensor Type

- Biosensors led the Medical Sensors Market with a 46.2% share in 2025, driven by continuous glucose monitoring and cardiac biomarker detection

- Optical and image sensors are forecast to expand at a 15.1% CAGR through 2035, supported by non-invasive diagnostics and hyperspectral imaging adoption

- Pressure sensors accounted for USD 1.38 billion in 2025, reflecting steady demand in ventilator and infusion pump applications

By Technology

- MEMS devices captured 55.3% of the Medical Sensors Market in 2025, reinforced by semiconductor miniaturization and wafer-level packaging innovations

- Nano and graphene sensors are projected to grow at a 15.6% CAGR, attracting R&D investment for implantable physiological sensors with enhanced biocompatibility

By Region

- North America represented 36.5% of the Medical Sensors Market share in 2025

- Asia-Pacific exhibits the fastest regional CAGR at 14.85% to 2035, led by China, India, and South Korea

- Europe contributed approximately USD 2.54 billion to the Medical Sensors Market in 2025

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue estimates from device OEM shipments, component-level ASP tracking, and top-down validation against national health expenditure databases. Historical data (2021–2024) derives from audited annual reports and trade association filings; forecast projections (2026–2035) apply regression-adjusted compound growth modeling calibrated to regulatory approval pipelines and reimbursement expansion schedules.