Drilling Tools Market Summary

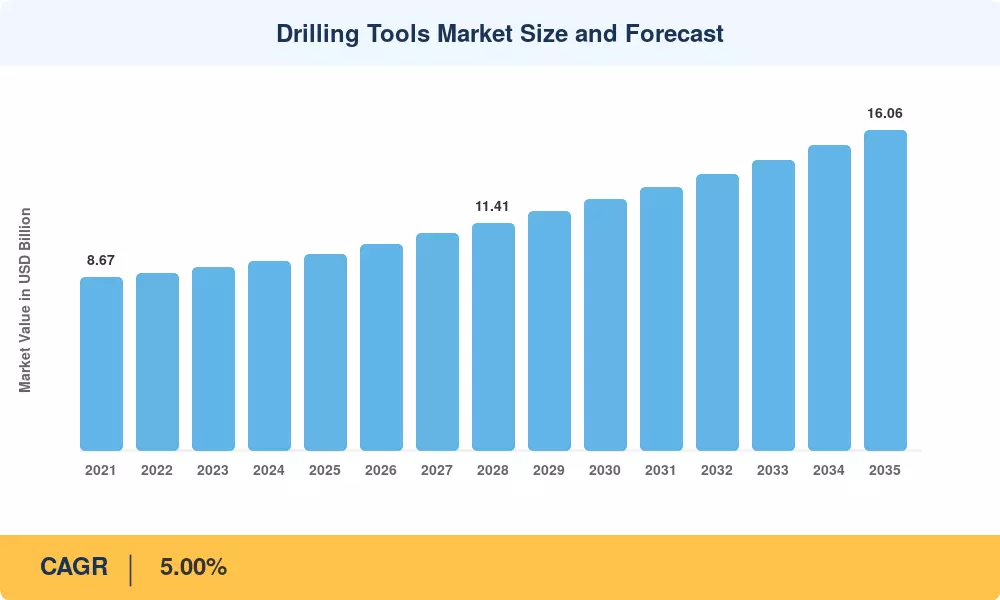

The Drilling Tools Market reached an estimated USD 9.86 billion in 2025 and is projected to grow from USD 10.35 billion in 2026 to USD 16.06 billion by 2035, registering a compound annual growth rate of 5.00% during the forecast period. Selective reinvestment in high-return wells and final investment decisions on deep- and ultra-deepwater assets across Brazil, the US Gulf of Mexico, and West Africa are anchoring the Drilling Tools Market expansion. Governments in more than 30 countries have introduced accelerated permitting frameworks for upstream exploration since 2023, collectively unlocking an estimated USD 78 Billion in new drilling commitments through 2030 [1].

A significant technology transformation is reshaping the Drilling Tools Market as operators replace conventional fixed-cutter and roller-cone assemblies with rotary steerable systems and high-specification mud motors that shorten rig time by 15–25% per lateral section [2]. National energy security mandates—including the US Inflation Reduction Act provisions for domestic critical-mineral drilling and the EU Critical Raw Materials Act—are channeling fresh capital toward advanced downhole equipment, with combined public-private investment surpassing USD 14 billion through 2028 [3].

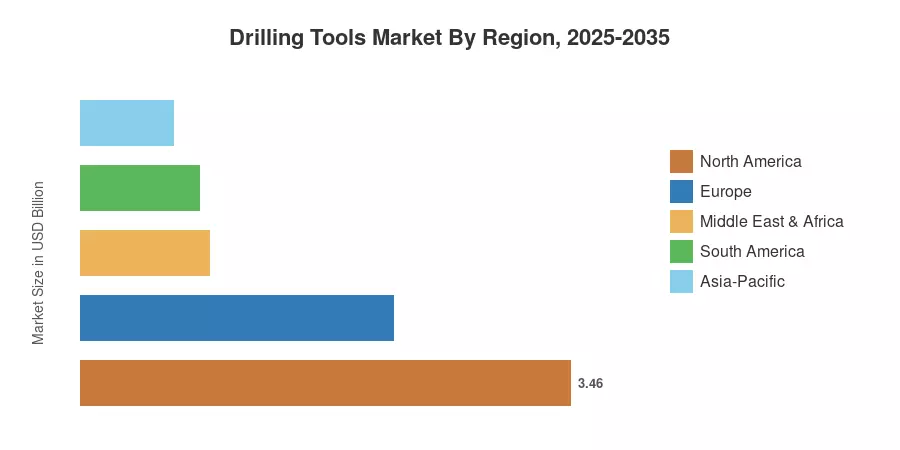

North America remained the dominant force in the Drilling Tools Market, commanding a 35.1% revenue share in 2025, powered by sustained Permian Basin and Montney formation activity. Asia-Pacific is the fastest-growing region with a projected 6.65% CAGR through 2035, driven by accelerating offshore programs in Southeast Asia and India's expanded sedimentary-basin licensing rounds. Europe held the second-largest share at 22.4%, supported by North Sea decommissioning-to-redevelopment cycles and growing geothermal well counts in Germany and Iceland [4]. The Drilling Tools Market trajectory over the coming decade will hinge on how quickly operators integrate automation, data analytics, and lower-carbon drilling programs into their capital budgets.

Key Report Takeaways

• By Tool Type

- Drill bits accounted for 34.3% of the Drilling Tools Market in 2025, reflecting the universal requirement for cutting structures across every well design.

- The "Other Tools" category is poised to expand at an 8.31% CAGR through 2035, fueled by growing adoption of specialty jars, hole openers, and casing-exit tools in complex completions.

• By Application

- Development and production drilling represented 47.8% of the Drilling Tools Market in 2025, as brownfield infill programs kept mature basins productive.

- Geothermal drilling is forecast to register a 9.92% CAGR through 2035, supported by enhanced geothermal system pilot projects in the US, Germany, and Japan.

• By Region

- North America generated 35.1% of the Drilling Tools Market revenue in 2025, anchored by horizontal-well intensity across tight-oil and shale-gas plays.

- Asia-Pacific is set to record the fastest regional growth at 6.65% CAGR, as India, Indonesia, and Australia ramp up exploration investment.

Market Size and Forecast (2021–2035)

Market Research Future derived historical figures from upstream capital expenditure databases, oilfield-service revenue disclosures, and customs-trade data. Forecast projections apply a calibrated CAGR model validated against rig-count trajectories, FID pipelines, and regional permitting trends [5].