Drug Repurposing Market Summary

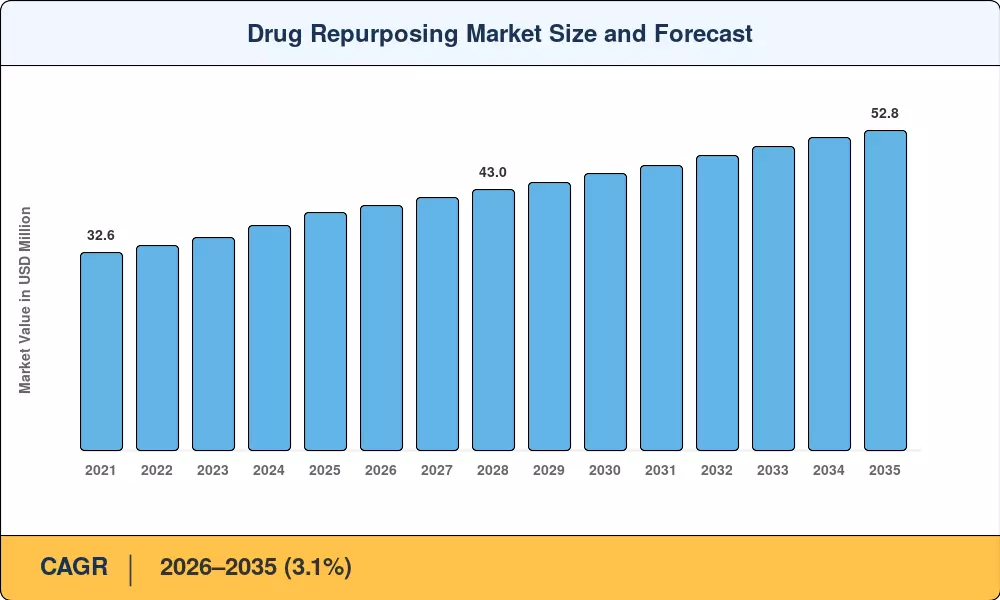

The Drug Repurposing Market reached an estimated USD 39.2 Billion in 2025, positioning it for steady expansion to USD 40.4 Billion in 2026 and a projected USD 52.8 Billion by 2035 at a 3.1% CAGR during the forecast period. This growth trajectory reflects a fundamental shift in pharmaceutical R&D strategy: with patent cliffs threatening an estimated USD 197 Billion in branded-drug revenue by 2031, innovators are accelerating efforts to find new therapeutic uses for existing drug new indication candidates rather than pursuing costly de novo discovery [2]. Regulatory pathways such as the FDA's 505(b)(2) route and the EMA's hybrid application procedure have formalized frameworks that reward therapeutic reprofiling strategies with shortened approval timelines.

A technology transformation is reshaping the Drug Repurposing Market at its core. Legacy trial-and-error screening approaches are giving way to computational drug repositioning platforms powered by machine learning and network pharmacology. The National Institutes of Health's NCATS program has committed over USD 750 Million in cumulative funding toward translational science initiatives that directly support off-label drug repositioning programs [3]. Pharma companies are integrating AI-driven target identification into their pipelines, compressing candidate selection from years to months and cutting preclinical costs by an estimated 40–60%.

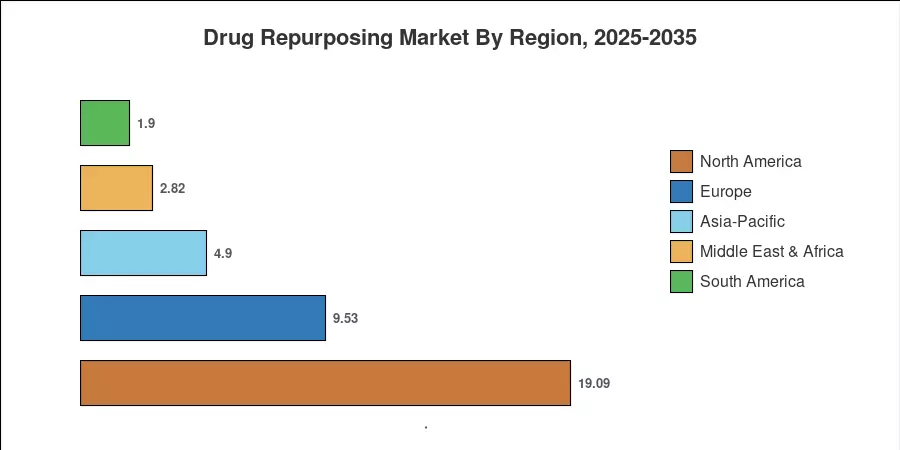

North America anchors global demand in the Drug Repurposing Market, commanding approximately 48.7% of 2024 revenue, driven by robust FDA-approved drug repurposing pathways and deep venture capital ecosystems. Asia-Pacific represents the fastest-growing region at a projected 12.5% CAGR through 2035, fueled by expanding clinical-trial infrastructure in China and India and favorable cost differentials. Europe holds the second-largest share at roughly 24.3%, with the EMA's adaptive licensing framework supporting accelerated approvals for repurposed molecules. The next decade will see computational drug repositioning and real-world evidence analytics redefine competitive advantage across every region.

Key Report Takeaways

• By Therapeutic Area

- Oncology led the Drug Repurposing Market with a 40.1% revenue share in 2024, reflecting sustained pipeline investment in immuno-oncology combinations and off-label drug repositioning for treatment-resistant tumors

- Rare and orphan diseases are projected to expand at a 15.9% CAGR through 2035, supported by orphan-drug incentive programs and venture funding surges

- CNS disorders represent the third-largest therapeutic area, with computational drug repositioning accelerating candidate identification for neurodegenerative conditions

• By Molecule Type

- Small-molecule drugs accounted for 69.4% of the Drug Repurposing Market in 2024, benefiting from well-characterized safety profiles and lower reformulation costs

- Peptides and biologics are advancing at a 14.1% CAGR, as therapeutic reprofiling strategy extends to complex molecules with declining manufacturing costs

• By Region

- North America commanded 48.7% of the 2024 Drug Repurposing Market revenue

- Asia-Pacific is forecast to grow at a 12.5% CAGR through 2035, driven by cost-competitive clinical operations and rising government investment in existing drug new indication research

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from company filings, regulatory approval databases, and pipeline analytics across all therapeutic reprofiling strategy segments. Top-down validation draws on national health expenditure data and patent-expiry calendars. The following table presents the Drug Repurposing Market trajectory across the full study period.