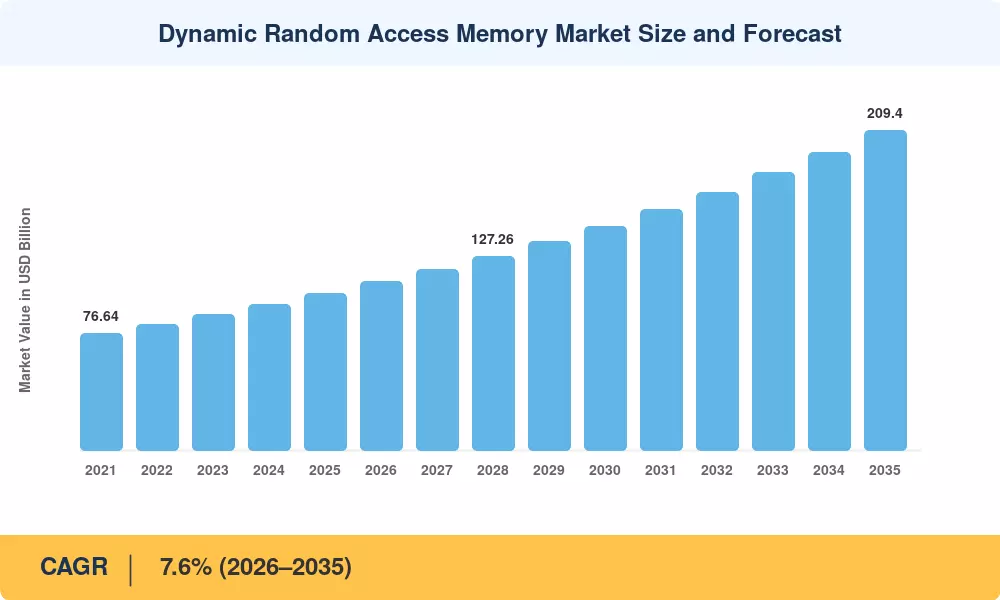

Dynamic Random Access Memory Market Summary

The dynamic random access memory market reached an estimated USD 102.8 billion in 2025, propelled by surging demand from data center operators, AI training clusters, and mobile device manufacturers. Starting from approximately USD 110.6 billion in 2026, the dynamic random access memory market is projected to expand at a CAGR of 7.6% through 2035, reaching USD 209.4 billion by the end of the forecast period. Two catalysts anchor this trajectory: hyperscaler capital expenditure on AI-optimized servers, which topped USD 160 billion globally in 2024 [2], and the accelerated rollout of 5G-enabled smartphones demanding higher-density LPDDR5 memory for mobile processors.

The manufacture of DRAM is undergoing a technical shift. DDR5 DRAM modules are replacing legacy DDR4 nodes for servers and PCs with double the bandwidth and better power efficiency per chip. Samsung, SK Hynix and Micron announced approximately USD 90 billion investments in wafer fab capacity expansion from 2023 to 2027. EUV lithography migration at the 1-alpha and 1-beta process nodes is expected to provide 15–20% cost-per-bit reductions every generation [3]. The HBM2 high bandwidth memory for AI circuits has become the fastest growing product class, with NVIDIA’s GPU roadmap bringing forward demand by at least two quarters.

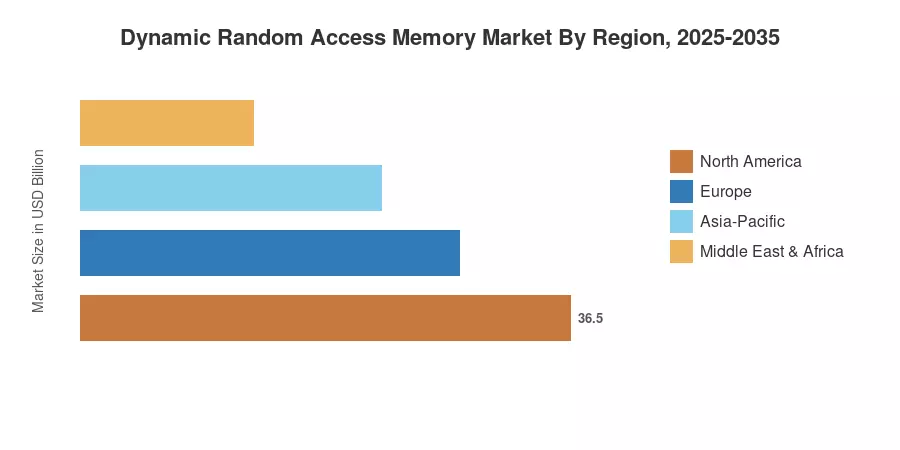

Asia-Pacific is the largest region in the dynamic random access memory market, accounting for almost 42% of the worldwide sales, led by fabrication clusters in South Korea, Japan and Taiwan. Cloud infrastructure spending is underpinning North America, the No. 2 market at over 28%. Europe accounts for about. 16% and the rest are Middle East & Africa and South America. Asia-Pacific remains firmly the fastest growing region through to 2035, as government semiconductor subsidies and localized assembly operations continue to draw investment

Key Report Takeaways

• By Technology

- DDR5 DRAM modules for servers and PCs command roughly 38% of the dynamic random access memory market by revenue in 2025, driven by Intel Sapphire Rapids and AMD Genoa platform adoption

- HBM2 high bandwidth memory for AI chips is growing at an estimated 18.5% CAGR through 2035, the fastest among all DRAM types in the dynamic random access memory market

• By Application

- Data centers and cloud computing represent the largest application vertical, contributing over 35% share of the dynamic random access memory market

- Automotive DRAM demand expands at 11.2% CAGR as ADAS and in-vehicle infotainment systems require ECC DRAM for mission-critical computing

• By Region

- Asia-Pacific leads the dynamic random access memory market at approximately 42% share, with South Korea alone contributing nearly 19% of global output

- Europe's dynamic random access memory market grows at 6.9% CAGR, supported by the EU Chips Act's €43 billion mobilization target

MRFR’s market size is based on direct interviews with 85+ semiconductor executives, quarterly shipment data from WSTS, firm financial disclosures, and unique demand models calibrated to fab utilization rates. Historical numbers are actuals (2021-2024); 2025 is a base year estimate; and 2026-2035 are projected forecasts.