Edge Computing Market Summary

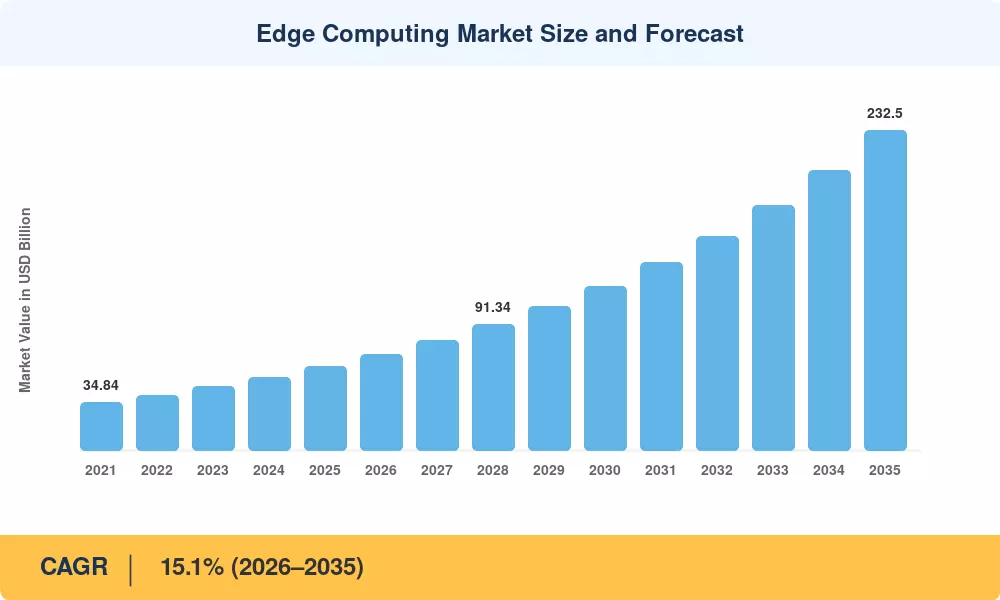

The Edge Computing Market reached an estimated USD 61.2 billion in 2025 and is projected to grow from USD 70.4 billion in 2026 to USD 232.5 billion by 2035, registering a CAGR of 15.1% during the forecast period (2026–2035). This expansion tracks closely with the global rollout of 5G-enabled edge computing deployments, which have cut latency budgets from 50 ms to under 10 ms for mission-critical workloads. The U.S. CHIPS and Science Act has earmarked over USD 52 billion for semiconductor and advanced compute infrastructure, a portion of which directly funds decentralized edge computing infrastructure build-outs across federal and defense networks [1].

Legacy centralized cloud architectures are buckling under data gravity. By 2025, enterprises generate roughly 75% of their data outside traditional data centers, according to Gartner. IoT edge processing and data filtering now handle initial inference at the device level, reducing backhaul bandwidth costs by 30–40% for manufacturers running smart-factory lines. Telecom operators have invested over USD 18 billion collectively in multi-access edge computing (MEC) platforms since 2022, signaling that fog computing and edge node management is shifting from pilot stage to production scale [3].

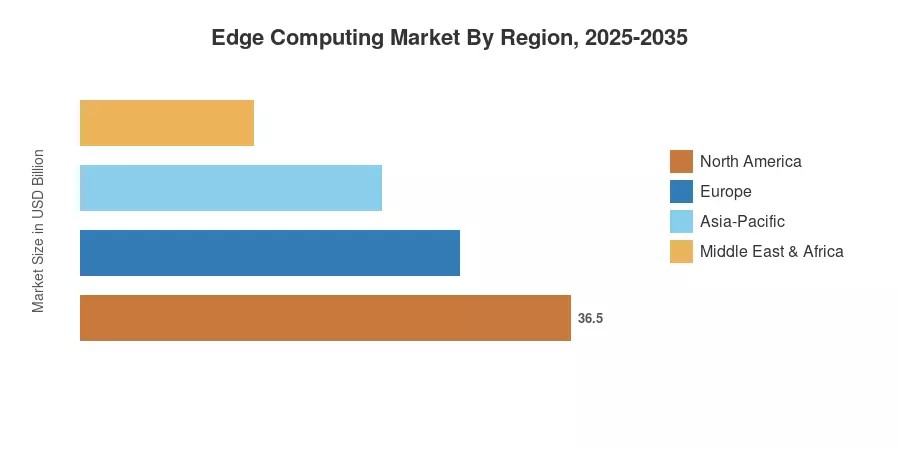

North America commands roughly 38% of the Edge Computing Market, driven by hyperscaler capex and defense-grade deployments. Asia-Pacific is the fastest-growing region at a CAGR of 17.8%, fueled by China's "East Data, West Computing" initiative and India's Digital India push. Europe holds the second-largest share at approximately 27%, anchored by GAIA-X data sovereignty mandates and Germany's Industrie 4.0 edge rollouts [4]. The next decade will see low-latency edge compute for real-time apps redefine how every connected industry operates.

Key Report Takeaways

• By Technology

- Hardware (servers, gateways, sensors) holds approximately 45% of the Edge Computing Market, as enterprises prioritize on-premises processing appliances over software-only stacks

- Edge AI software platforms are growing at a CAGR of 18.3%, reflecting demand for real-time machine-learning inference at the node level

- Edge-managed services surpassed USD 9.8 billion in 2025, driven by enterprises outsourcing fog computing and edge node management to managed-service providers

• By Sector

- Manufacturing leads sector adoption with a 22% revenue share in the Edge Computing Market, as IoT edge processing and data filtering underpins predictive-maintenance workflows

- Telecommunications is expanding at a CAGR of 16.5%, propelled by 5G-enabled edge computing deployments across network slicing and MEC platforms

- Healthcare edge deployments reached USD 5.4 billion in 2025, supporting real-time imaging diagnostics and remote patient monitoring

• By Region

- North America generated roughly USD 23.3 billion in 2025, supported by hyperscaler edge zones and U.S. DoD edge modernization budgets

- Asia-Pacific is the fastest-growing region in the Edge Computing Market at 17.8% CAGR through 2035

- Europe's share stands at approximately 27%, backed by GAIA-X and the EU Data Act's data-localization clauses

Market sizing combines bottom-up revenue analysis across hardware, software, and services with top-down cross-validation against enterprise IT spending surveys from IDC, Gartner, and operator capex filings. Historical figures (2021–2024) draw from audited company revenues and trade-association databases; forecast figures (2026–2035) apply segment-level growth modeling anchored to the 15.1% CAGR, adjusted for technology adoption S-curves and macroeconomic scenarios.