Edge Data Center Market Summary

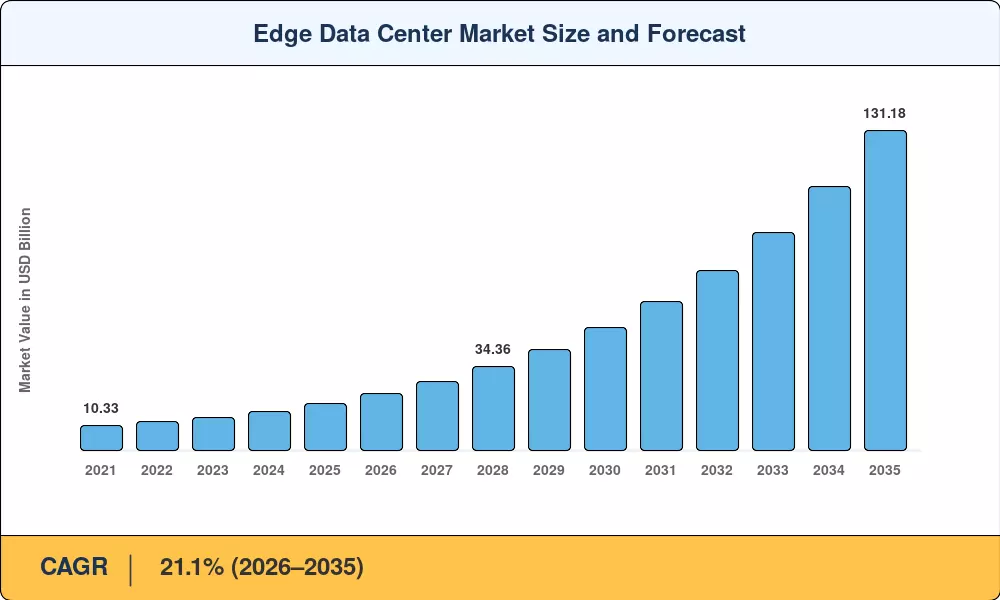

The Edge Data Center Market reached USD 19.35 billion in 2025, and this trajectory is set to accelerate — from an estimated USD 23.43 billion in 2026 to USD 131.18 billion by 2035, reflecting a compound annual growth rate of 21.1% across the forecast window [1]. Two forces are keeping construction pipelines full: data sovereignty mandates now active in more than 45 jurisdictions worldwide, and 5G radio densification programs that demand compute nodes within single-digit millisecond reach of end devices [4]. Operators that once debated the economics of distributing workloads away from centralized hyperscale campuses are now treating edge facilities as non-negotiable infrastructure.

A technology transition is underway. Legacy on-premise server closets and remote-office racks — often air-cooled, manually managed, and limited to basic file serving — are giving way to modular, liquid-cooled micro-facilities capable of running inference workloads for generative AI, autonomous vehicle mapping, and industrial digital twins [11]. The U.S. Department of Energy estimates data center power demand will rise 15–20% annually through 2030, with edge sites accounting for a growing slice of that load [3]. Capital is following: global data center construction spending surpassed USD 48 billion in 2024, and a meaningful share targeted sub-5 MW edge builds [14].

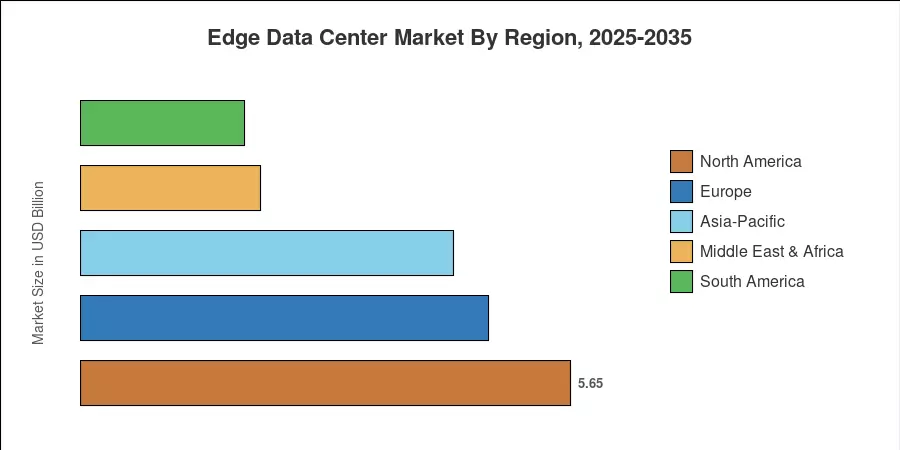

North America held the dominant position in the Edge Data Center Market with a 29.2% share in 2025, anchored by hyperscaler overflow requirements and enterprise hybrid-cloud mandates. Asia-Pacific is the fastest-growing region at a 22.2% CAGR, propelled by digital payment infrastructure build-outs and smart-city programs across India, China, and ASEAN nations. Europe commands the second-largest share at 24.3%, driven by GDPR-compliant local processing requirements and the EU's Digital Decade policy targets [8]. As AI inference shifts closer to the point of consumption, the Edge Data Center Market is positioned for a decade of compounding investment.

Key Report Takeaways

• By Component

- Solutions accounted for 57.8% of the Edge Data Center Market in 2025, reflecting demand for integrated power, cooling, and IT enclosure systems.

- Services will grow at a 22.0% CAGR through 2035, fueled by managed-edge and edge-as-a-service subscription models.

• By Data Center Size

- Large facilities controlled 49.8% share of the Edge Data Center Market in 2025, serving metro-area enterprise clusters.

- Mega-class edge sites will expand fastest at a 23.7% CAGR, driven by AI inference farm requirements at the periphery.

• By Tier

- Large facilities controlled 49.8% share of the Edge Data Center Market in 2025, serving metro-area enterprise clusters.

- Mega-class edge sites will expand fastest at a 23.7% CAGR, driven by AI inference farm requirements at the periphery.

- Tier 3 configurations held 48.9% share in 2025, balancing redundancy with capital efficiency.

• By End User

- BFSI captured 26.5% of the Edge Data Center Market share in 2025, reflecting real-time fraud detection and payment processing needs.

- IT & Telecom will record a 21.8% CAGR through 2035 as multi-access edge computing (MEC) deployments accelerate.

• By Region

- North America led the Edge Data Center Market with 29.2% share in 2025.

- Asia-Pacific is on track to record a 22.2% CAGR, making it the fastest-growing region.

Edge Data Center Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining bottom-up facility-level revenue tracking, top-down macroeconomic modeling tied to GDP-weighted IT spending, and secondary validation against operator disclosures and third-party infrastructure surveys [1][6]. Historical values (2021–2024) are actuals; 2025 is the estimated base year; and 2026–2035 values are forecast projections anchored to a 21.1% CAGR.