Electric Insulator Market Summary

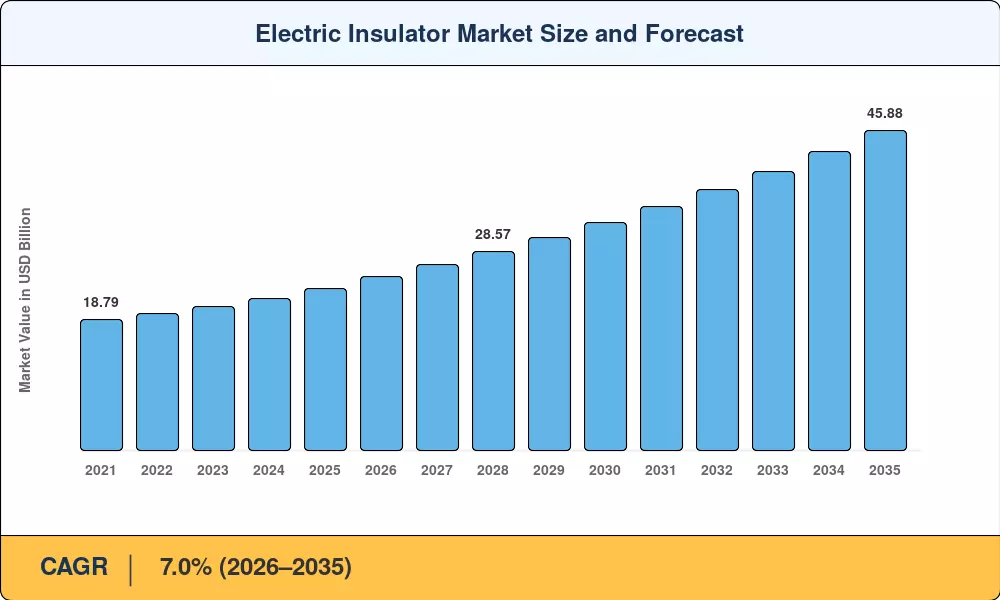

The Electric Insulator Market reached an estimated USD 23.28 Billion in 2025 and is projected to climb from USD 24.95 Billion in 2026 to USD 45.88 Billion by 2035, advancing at a compound annual growth rate of 7.0% across the forecast period. This expansion is anchored in two converging forces: a global wave of grid-hardening investments exceeding USD 680 Billion through the decade [1], and the accelerating build-out of ultra-high-voltage direct-current corridors connecting renewable generation hubs to urban load centers. Utilities across mature and developing economies alike are replacing aging insulator fleets installed during the mid-twentieth-century electrification cycle, while new HVDC interconnections demand insulator specifications that legacy ceramic designs struggle to meet.

The technology landscape within the Electric Insulator Market is undergoing a generational shift. Traditional porcelain and glass insulator strings — workhorses of transmission grids for over a century — are yielding ground to silicone-rubber composite designs that weigh 70–80% less and resist pollution flashover far more effectively [2]. China's State Grid Corporation alone committed over USD 28 Billion to UHV transmission between 2023 and 2025, driving the largest single source of insulator procurement globally [3]. India's Green Energy Corridor Phase II, backed by USD 8.6 Billion in government support, has similarly catalyzed demand for high-voltage composite units rated above 400 kV [4].

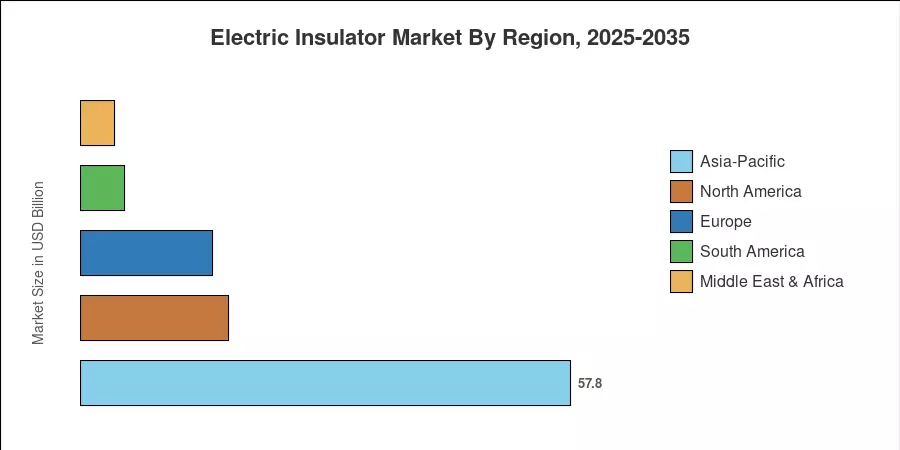

Asia-Pacific commands the dominant position in the Electric Insulator Market with approximately 57.8% of global revenue in 2025, propelled by China's ultra-high-voltage program and India's renewable-evacuation corridors. The region also registers the fastest projected CAGR at 7.8% through 2035. Europe holds the second-largest share at roughly 15.6%, driven by offshore wind interconnections and the European Commission's TEN-E infrastructure mandates [5]. North America's share stands near 17.4%, supported by the U.S. Department of Energy's Building a Better Grid Initiative, allocating USD 20 Billion to transmission modernization [6]. The Electric Insulator Market outlook through the next decade hinges on how quickly utilities transition procurement cycles toward composite polymer insulator line solutions and how regulatory bodies harmonize testing standards across trade blocs.

Key Report Takeaways

• By Dielectric Material

- Ceramic and porcelain insulators captured approximately 48.2% of the Electric Insulator Market share in 2025, underpinned by long service life and lower unit cost for standard distribution voltages.

- Composite and polymer variants are forecast to register the fastest segment CAGR of 8.3% between 2026 and 2035, driven by weight savings and pollution resistance for HVDC corridors.

• By Voltage Rating & Application

- Medium-voltage products accounted for the largest revenue share among voltage categories in the Electric Insulator Market in 2025, reflecting deep penetration in urban distribution networks.

- Transmission line applications led with approximately 44.5% of the Electric Insulator Market in 2025, with HVDC sub-applications expected to outpace the overall segment.

• By Region

- Asia-Pacific held roughly 57.8% of the Electric Insulator Market in 2025, with China and India together driving more than two-thirds of regional demand.

- North America's share stood at 17.4%, supported by federal grid-modernization legislation and wildfire-mitigation insulator upgrades across the western United States.

Market Size and Forecast (2021–2035)

Market Research Future's Electric Insulator Market sizing integrates top-down regulatory-spending analysis with bottom-up OEM shipment tracking across 28 country markets. Historical figures (2021–2024) are triangulated against utility capital-expenditure disclosures and customs trade data; forecast values (2026–2035) apply scenario-weighted CAGR modeling anchored to grid-investment pipelines published by IEA and national transmission authorities [1][7].