EV Test Equipment Market Summary

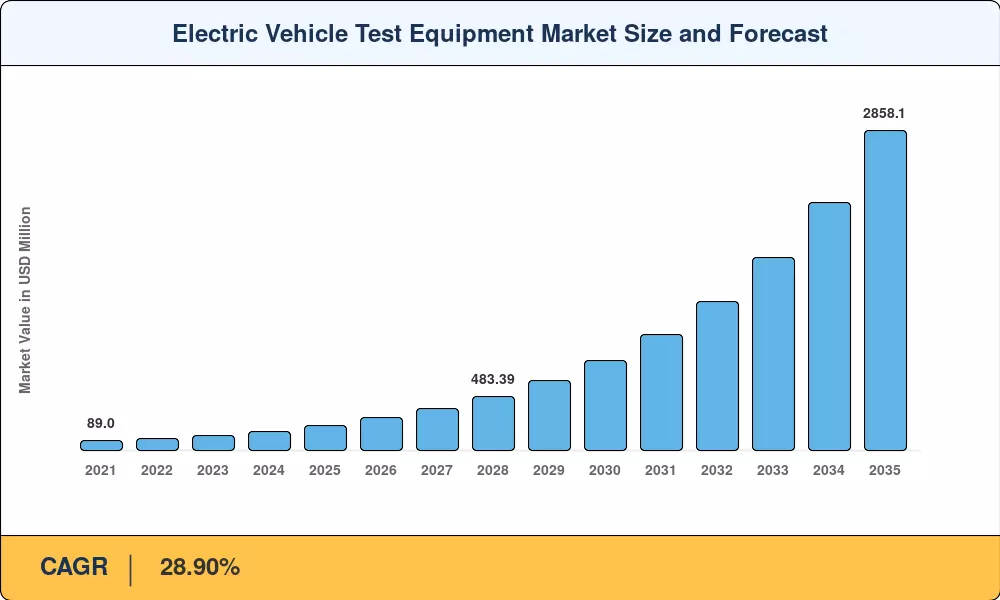

The electric vehicle test equipment market reached an estimated USD 225.80 Million in 2025 and is projected to surge to USD 2,858.10 Million by 2035, registering a 28.90% CAGR across the 2026–2035 forecast window. Two forces are converging to accelerate spending: first, automakers worldwide are scaling production toward an expected 40 million battery-electric units per year by 2030, and each assembly line requires dedicated validation hardware before vehicles reach consumers [1]. Second, tightening regulatory frameworks—particularly the EU Battery Regulation mandating digital battery passports by 2027 and UNECE R155/R156 cybersecurity type-approval deadlines—have compressed validation timetables and pushed OEMs to invest earlier in test infrastructure [2].

Technology transformation in the electric vehicle test equipment market is most visible in the migration from 400 V to 800 V drivetrain architectures. Legacy dynamometer and battery-cycling platforms designed for lower-voltage packs cannot safely handle the thermal management, insulation-resistance, and high-frequency switching demands of 800 V systems [3]. Retooling these stations has become a multi-billion-dollar upgrade cycle; BloombergNEF estimates that global spending on EV production-line capital equipment surpassed USD 16 billion in 2024 alone, with test and validation benches representing a growing share of that outlay [4].

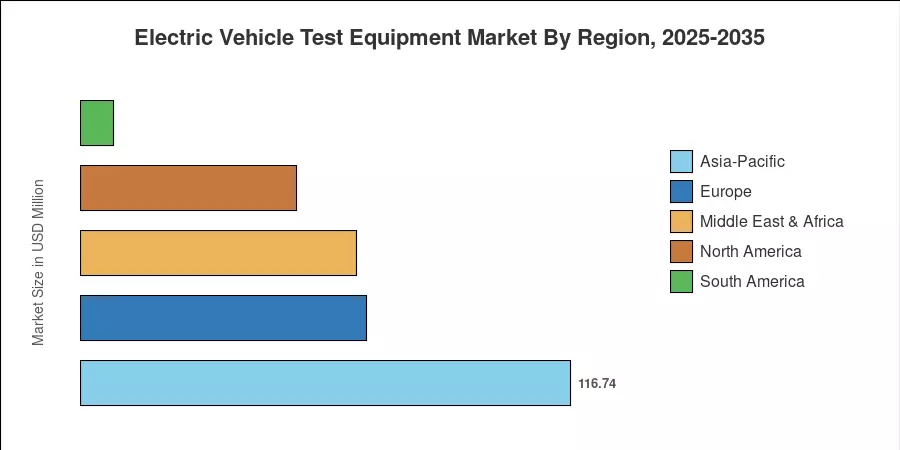

From a regional standpoint, Asia-Pacific dominated the electric vehicle test equipment market with roughly 51.7% of 2024 revenue, driven by China's battery mega-factory expansion and South Korea's cathode-material R&D push. Asia-Pacific is also the fastest-growing region at a projected 35.5% CAGR through 2035. North America held the second-largest share at approximately 22.8%, buoyed by Inflation Reduction Act incentives that tie tax credits to domestic content requirements for battery cells and packs [5]. Europe accounted for about 18.6% of the global electric vehicle test equipment market, with Germany's Fraunhofer institutes and France's investment in gigafactory corridors anchoring demand. As solid-state batteries and silicon-anode chemistries move from pilot lines to volume production, the need for next-generation test platforms will only intensify.

Key Report Takeaways

• By Vehicle Type & Propulsion

- Passenger cars generated approximately 64.1% of the 2024 electric vehicle test equipment market revenue, reflecting the sheer volume of BEV sedan and SUV launches across global platforms.

- Commercial-vehicle test demand is the fastest-growing vehicle-type segment, projected to expand at a 36.9% CAGR through 2035 as electric bus and truck programs ramp up in China, Europe, and North America.

- Battery electric vehicles accounted for roughly 69.4% of propulsion-type demand in 2024, while fuel-cell electric vehicles are forecast to register a 33.3% CAGR as hydrogen-truck pilots scale.

• By Equipment Type & Application

- EV Battery Test Systems commanded approximately 44.6% of the 2024 electric vehicle test equipment market revenue, covering cell-level cycling, module abuse testing, and pack-level thermal validation.

- EVSE and Charging Test Systems represent the fastest-growing equipment category at an estimated 33.0% CAGR, driven by megawatt charging standards for commercial fleets.

- OEM end-of-line testing held roughly 48.7% of application revenue in 2024, while independent and certification laboratories are forecast to grow at 35.8% CAGR through 2035.

• By Region

- Asia-Pacific led the electric vehicle test equipment market with a 51.7% revenue share in 2024 and is the fastest-growing region at a 35.5% CAGR.

- North America contributed approximately USD 51.48 Million in 2024 revenue, supported by DOE loan-program disbursements for battery plant buildouts.

- Europe is projected to grow at a 30.2% CAGR, with Germany, France, and the Nordic countries anchoring investment.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down revenue estimates from OEM capital-expenditure disclosures, tier-one supplier order-book data, and bottom-up unit-shipment tracking across battery cyclers, powertrain dynamometers, charging-interface testers, and HIL simulation platforms. Historical figures (2021–2024) rely on audited company filings and verified trade data; forecast values (2026–2035) apply an econometric demand model calibrated against EV production forecasts published by the IEA and BloombergNEF [1][4].

.webp?v=1784802885)