Electricity Retailing Market Summary

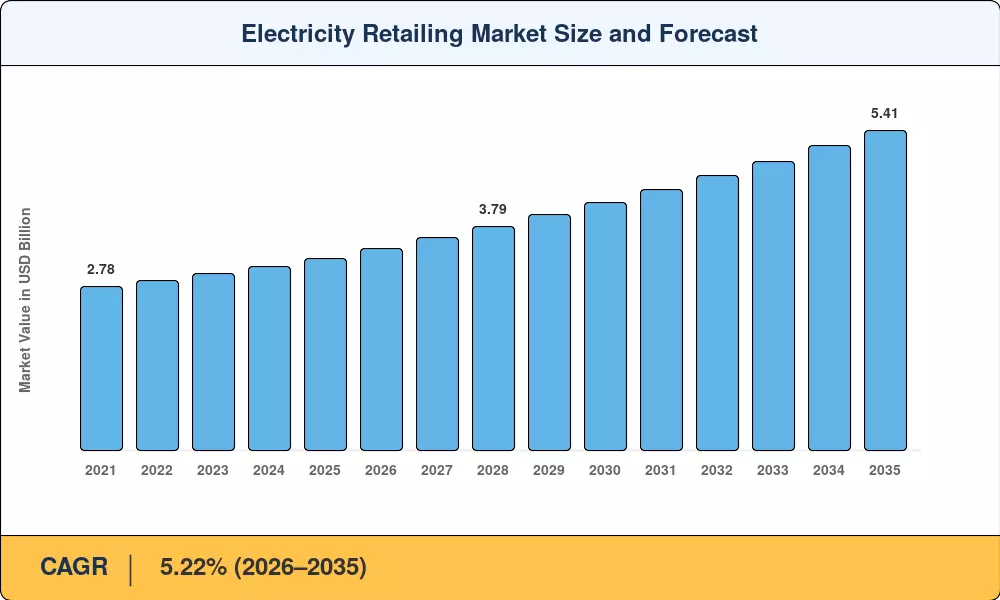

The global electricity retailing market was valued at USD 3.25 trillion in 2025 and is projected to grow from USD 3.42 trillion in 2026 to USD 5.41 trillion by 2035, registering a CAGR of 5.22% during the forecast period (2026–2035). Two structural forces are reshaping revenue trajectories for power retailers: government-mandated decarbonization timelines — the EU's Fit for 55 package alone mobilizes over EUR 300 billion in clean-energy investment through 2030 — and the rapid electrification of transportation, which the IEA projects will add roughly 1,500 TWh of incremental global demand by 2030 [1][2].

Dynamic, digitally enabled tariff structures are replacing legacy supply agreements established for baseload thermal generating. Retailers that have engaged in smart meter rollouts and cloud-based billing platforms currently control more than 400 million advanced metering endpoints worldwide, providing real-time pricing and demand-side flexibility services [3]. Regulatory agencies in OECD countries are tightening consumer-protection responsibilities, requiring merchants to balance tariff innovation and affordability obligations.

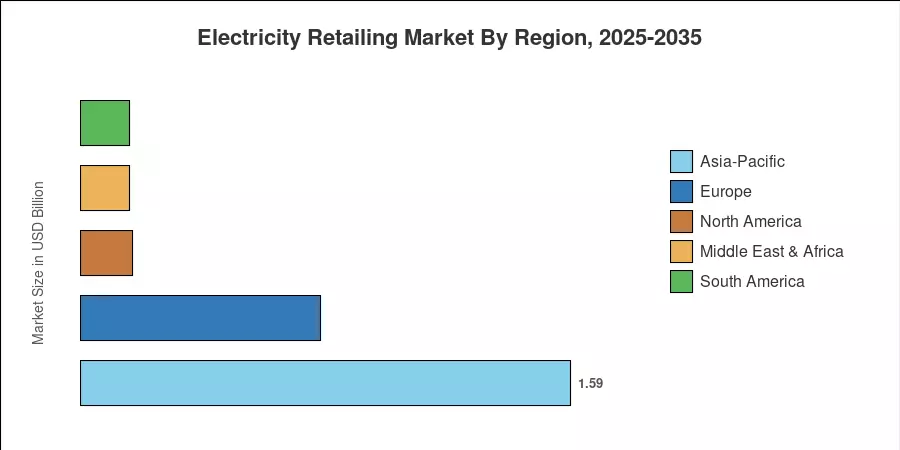

The Asia-Pacific region has the highest share of the electricity retailing industry, with a share of around 49% of the worldwide income, owing to continuing power-sector reform in China and the distribution revamp under UDAY in India. The region is also leading the rise at a predicted CAGR of 6.14%. Europe, which contributes about 24% of worldwide sales and is benefiting from aggressive renewable-integration targets, is next. North America, where data-center load and EV-charging infrastructure build-outs are reshaping peak-demand patterns, makes up the top three.

Key Report Takeaways

• By Tariff Type

- Fixed/flat-rate tariffs accounted for 47.5% of electricity retailing market revenue in 2025, reflecting consumer preference for bill predictability amid wholesale-price volatility.

- Green/renewable-backed tariffs are forecast to expand at a 7.92% CAGR through 2035, fueled by corporate ESG commitments and prosumer growth.

• By End-User

- The industrial segment represented the largest share of the electricity retailing market in 2025, driven by energy-intensive manufacturing clusters in Asia and Europe.

- Commercial end-users are projected to record a 6.35% CAGR as office electrification, on-site EV charging, and smart-building retrofits accelerate demand.

• By Geography

- Asia-Pacific led the electricity retailing market with a 49% revenue share in 2025, underpinned by China's provincial retail-pilot expansion and India's open-access reforms.

- North America is poised for robust expansion as hyperscale data centers and public-charging networks drive unprecedented load growth in key U.S. and Canadian utility territories.

Electricity Retailing Market Size and Forecast (2021–2035)

Market size estimates are based on utility revenue filings, national energy statistics databases (IEA, EIA, Eurostat), and proprietary demand models calibrated using metered consumption data from 45 countries [1][4][5].