Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

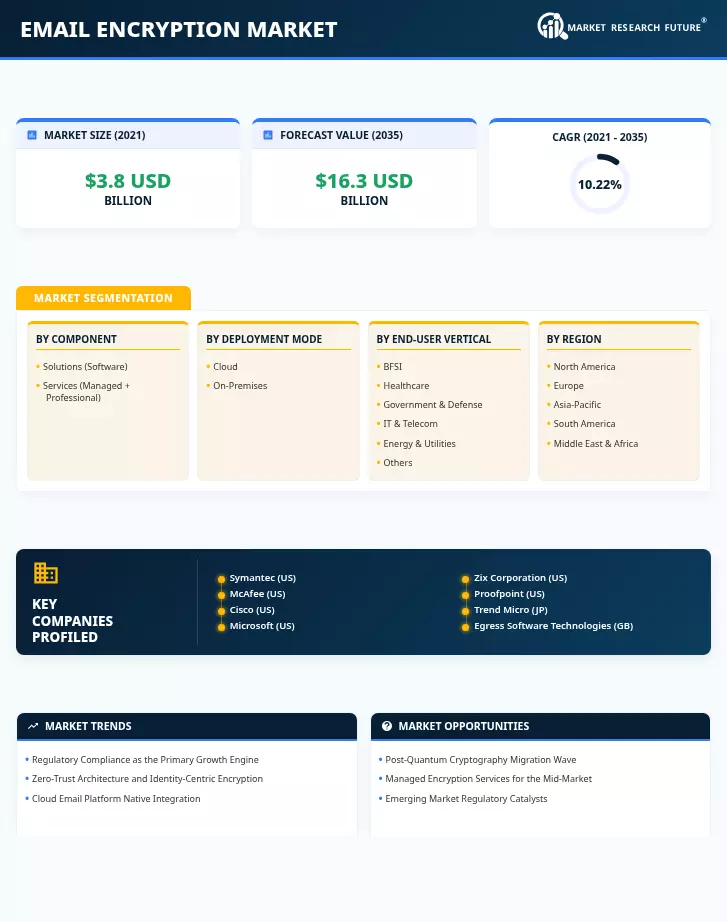

| By Component | Solutions (Software), Services (Managed + Professional) | Solutions (~64% share, 2025) | Services (11.8% CAGR) |

| By Deployment Mode | Cloud, On-Premises | Cloud (USD 3.6 B, 2025) | Cloud (higher absolute growth) |

| By End-User Vertical | BFSI, Email Encryption Market, Government & Defense, IT & Telecom, Energy & Utilities, Others | BFSI (~26% share, 2025) | Email Encryption Market (12.6% CAGR) |

| By Region | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America (~38% share, 2025) | Asia-Pacific (13.8% CAGR) |

Market Segmentation Overview

By Component

| Sub-Segment | Key Trend |

| Solutions (Software) | Gateway encryption platforms consolidating with native Microsoft 365 and Google Workspace integration; growing demand for policy-driven automatic encryption |

| Services (Managed + Professional) | Rise of encryption-as-a-service models targeting mid-market; increasing PKI outsourcing and compliance reporting consulting |

The component split reflects enterprise preference for licensed or subscription-based software products as the primary purchasing vehicle, with services growing as deployment complexity and compliance requirements drive demand for external expertise and managed key lifecycle operations.

By Deployment Mode

| Sub-Segment | Key Trend |

| Cloud | Dominance driven by SaaS email migration, API-based integration, and elastic key management infrastructure |

| On-Premises | Persistent demand from government, defense, and regulated financial institutions requiring sovereign key custody |

Cloud deployment continues to gain share as organizations move email infrastructure to hosted platforms, though on-premises solutions retain a critical role in high-security environments where encryption key material must remain within physically controlled boundaries.

By End-User Vertical

| Sub-Segment | Key Trend |

| BFSI | Regulatory-driven adoption across banking, insurance, and capital markets for customer data and transaction email protection |

| Email Encryption Market | Rapid growth driven by HIPAA enforcement, telehealth correspondence, and PHI-containing email volumes |

| Government & Defense | Zero-trust mandates, CMMC requirements, and classified information handling driving end-to-end encryption adoption |

| IT & Telecom | Customer data protection obligations and SLA-driven encryption for service provider communications |

| Energy & Utilities | NERC CIP compliance and OT/IT convergence extending encryption requirements to operational email systems |

| Others (Retail, Education, Manufacturing) | Growing awareness of data breach risks and emerging regulations in retail PCI compliance and educational data privacy |

Vertical adoption patterns mirror regulatory intensity — sectors with the most prescriptive data protection mandates demonstrate the highest encryption penetration rates, while less-regulated verticals are in earlier stages of adoption driven primarily by breach risk awareness and cyber insurance requirements.