Enhanced Oil Recovery Market Summary

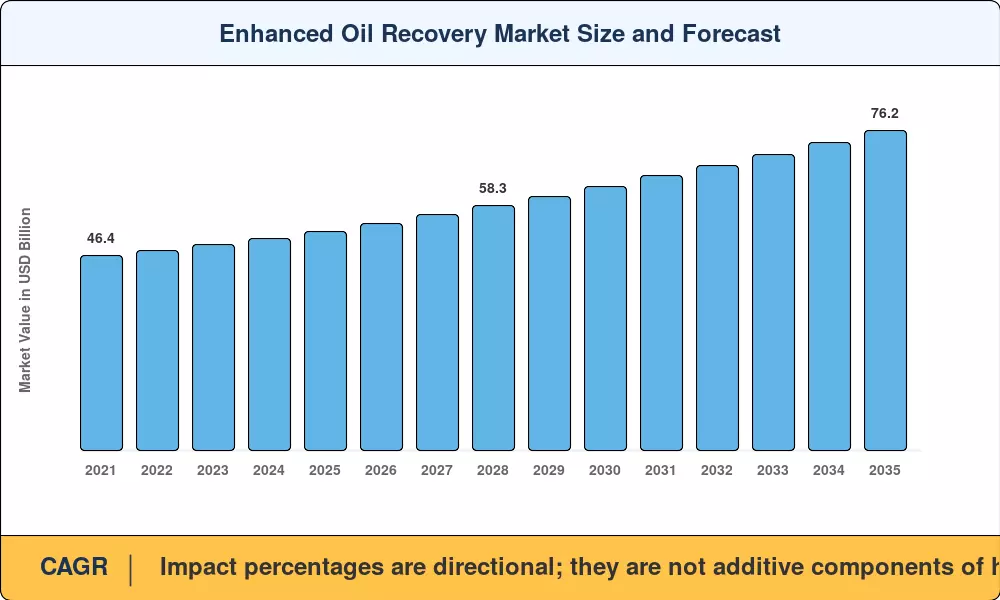

The Enhanced Oil Recovery Market was valued at USD 52.10 billion in 2025 and is projected to reach USD 54.00 billion in 2026 before climbing to USD 76.20 billion by 2035, advancing at a 3.9% CAGR during the 2026–2035 forecast period. Two structural tailwinds anchor this trajectory: the U.S. Section 45Q tax credit, which now awards up to USD 85 per metric ton of geologically sequestered CO₂, and OPEC+ production discipline that compels national oil companies to extract incremental barrels from aging reservoirs rather than develop frontier acreage [1][2]. Together, these forces redirect capital toward reservoir-optimization technologies at a pace that outstrips pure exploration budgets.

Field operators are moving away from first-generation steam-flood designs to integrated subsurface-modeling platforms that combine real-time fiber-optic sensing with machine learning decline-curve analysis. A longstanding policy commitment of the U.S. Department of Energy (DOE) between 2023 and 2025 has been to provide funding for carbon-capture, utilization and storage programs directly linked to oilfield injection, amounting to around $1.1 billion, which is now being realized by the private capital in the form of joint-venture arrangements [3][6].

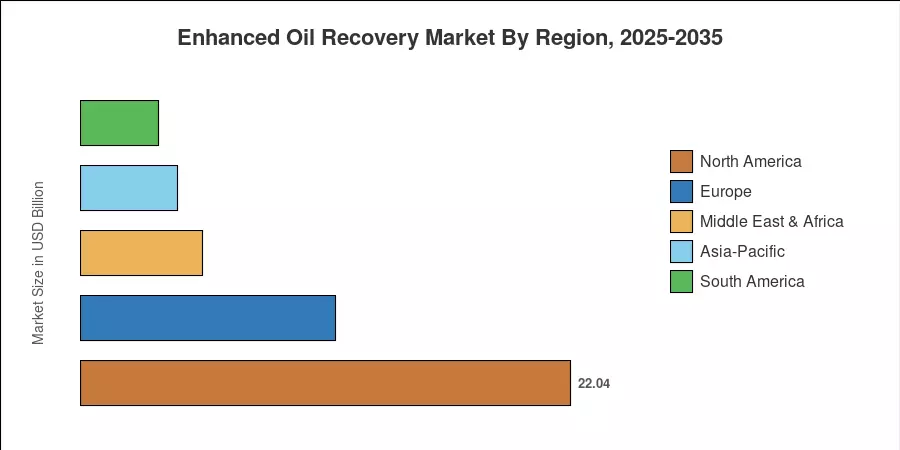

North America holds a share of about 42.3% in the Enhanced Oil Recovery Market. The Permian Basin and Western Canadian heavy-oil plays are at the forefront. However, Asia-Pacific is the fastest expanding area with a CAGR of 8.4%, fuelled by China’s Daqing and Shengli field revitalisation operations and India’s ONGC-led trial programmes. Europe holds the second largest share at around 22.0%, due to brownfield investments in the North Sea. Supply-side capacity for the Enhanced Oil Recovery Market is anticipated to ramp up into the early 2030s as CCUS pipeline networks expand throughout the U.S. Gulf Coast and Alberta.

Key Report Takeaways

• By Technology

- Thermal injection accounted for 47.5% of the Enhanced Oil Recovery Market in 2025, sustained by heavy-oil steam-flood operations across Canada and Venezuela.

- Gas injection is forecast to grow at a 6.9% CAGR through 2035, fueled by anthropogenic CO₂ supply from industrial capture facilities.

• By Reservoir

- Sandstone reservoirs held 49.2% of global Enhanced Oil Recovery Market deployments in 2025, benefiting from well-understood pore-geometry models that reduce screening risk.

- Mature fields represented 62.1% of total project starts in 2025, confirming the sector's tilt toward production optimization over greenfield exploration.

• By Geography

- North America maintained a 42.3% revenue share of the Enhanced Oil Recovery Market in 2025, supported by favorable regulatory treatment of injected CO₂.

- Asia-Pacific is projected to log an 8.4% CAGR through 2035, with China and India accounting for the bulk of new capacity additions.

Enhanced Oil Recovery Market Size and Forecast (2021–2035)

Market sizing combines bottom-up field-level production data from 14 main EOR basins with top-down macroeconomic variables, including crude-oil price trajectories, drilling-rig counts, and public capital-expenditure disclosures from operators representing over 65% of worldwide EOR output [1][4].

.webp?v=1784802855)