Farm Equipment Rental Market Summary

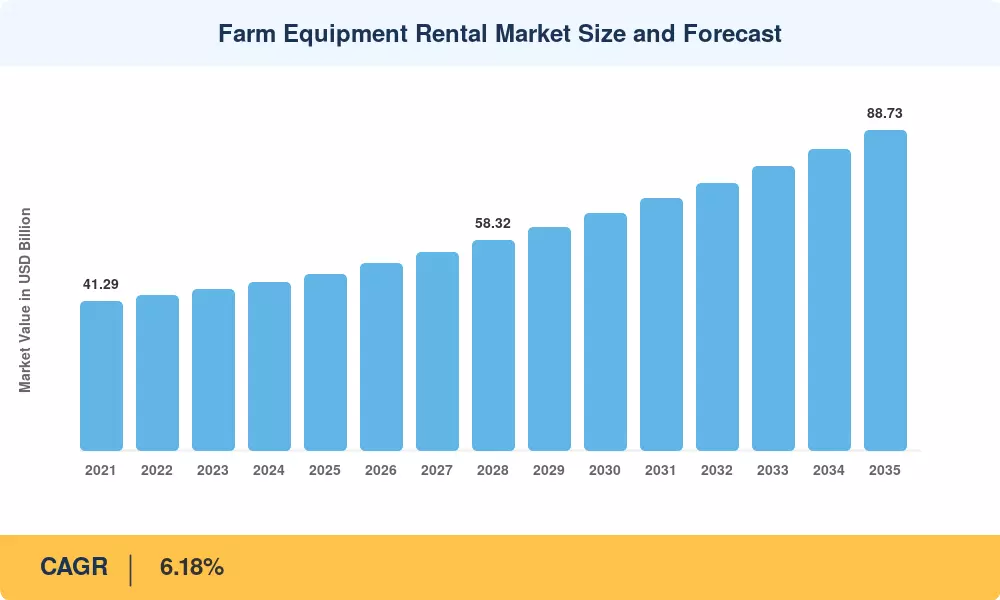

The farm equipment rental market was valued at USD 48.72 billion in 2025 and is projected to grow from USD 51.73 billion in 2026 to USD 88.73 billion by 2035, registering a CAGR of 6.18% during the forecast period (2026–2035). Rising capital costs for modern agricultural machinery, coupled with volatile commodity prices that squeeze farm-level margins, have driven a structural shift toward pay-per-use and lease-to-operate models. Government-backed mechanization programs — including the World Bank's USD 1.3 billion Agricultural Mechanization Initiative across Sub-Saharan Africa [1] and India's Sub-Mission on Agricultural Mechanization (SMAM) worth INR 4,500 crore [2] — are accelerating fleet deployments in underserved regions.

Technology is changing the way farmers access heavy machines. App-based rental systems, using dynamic pricing algorithms and GPS-enabled fleet tracking, are displacing legacy dealer-yard walk-in models. OEM captive finance divisions of Deere & Company, CNH Industrial and Kubota have established dedicated rental portfolios, not as aftermarket add-ons, but as ongoing revenue streams. Trials of autonomous tractors are squeezing the labor cost argument for outright ownership, forcing more operators to short-duration contracts.

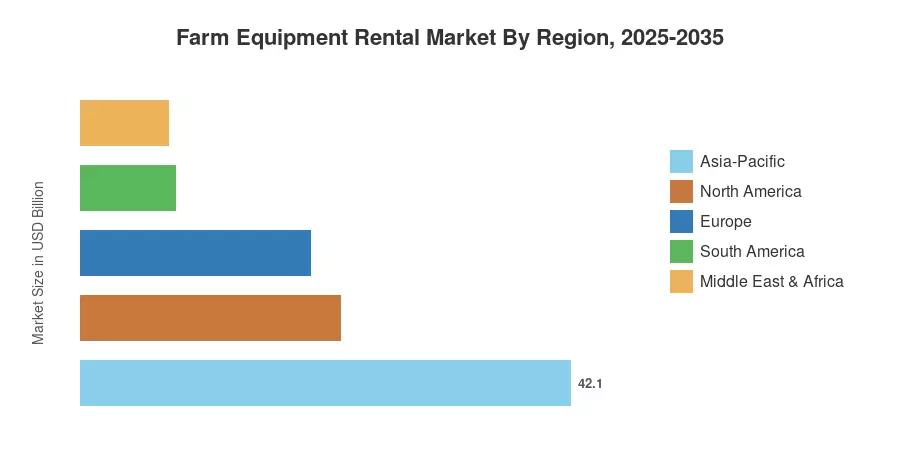

The Asia-Pacific region represents around 42% of the agricultural equipment rental market, driven by the concentration of smallholder farmers in India and cooperative mechanization networks in China. Africa is the fastest-expanding continent, anticipated to develop at a CAGR of about 8.5%, driven by donor-supported digitization and mobile-first booking platforms. The second-largest region is North America, which contributes about 22% of revenue, driven by large-acreage operators leasing high-horsepower combines and self-propelled sprayers. Fleet electrification and autonomous systems are changing unit economics, and the farm equipment rental market is on track to triple over the next decade.

Key Report Takeaways

• By Equipment Type

- Tractors captured 41.2% of the farm equipment rental market share in 2025, reflecting their universal applicability across tillage, hauling, and PTO-driven tasks.

- Harvesters are projected to record a CAGR of 7.96% through 2035, driven by combine rental demand during narrow harvest windows.

• By Business Model

- Offline dealers and co-op yards represented 83.2% of the farm equipment rental market in 2025.

- Online rental platforms are forecast to expand at a CAGR of 16.4% as app-based booking reaches new geographies.

• By Geography

- Asia-Pacific accounted for the largest share of the farm equipment rental market, supported by India's 120-million-plus smallholder base.

- Africa's farm equipment rental market is expanding fastest, with mobile booking penetration reaching an estimated 28% of new rental transactions by 2024.

Farm Equipment Rental Market Size and Forecast (2021–2035)

Market Research Future’s projections are based on surveys with primary dealers in 34 countries, OEM financial disclosures, mechanization databases from the Food and Agriculture Organization (FAO) and proprietary rental-transaction samples from six prominent digital platforms. Historical figures (2021-2024) are cross-checked with custom-import data and census data on agriculture.