Fill Finish Manufacturing Market Summary

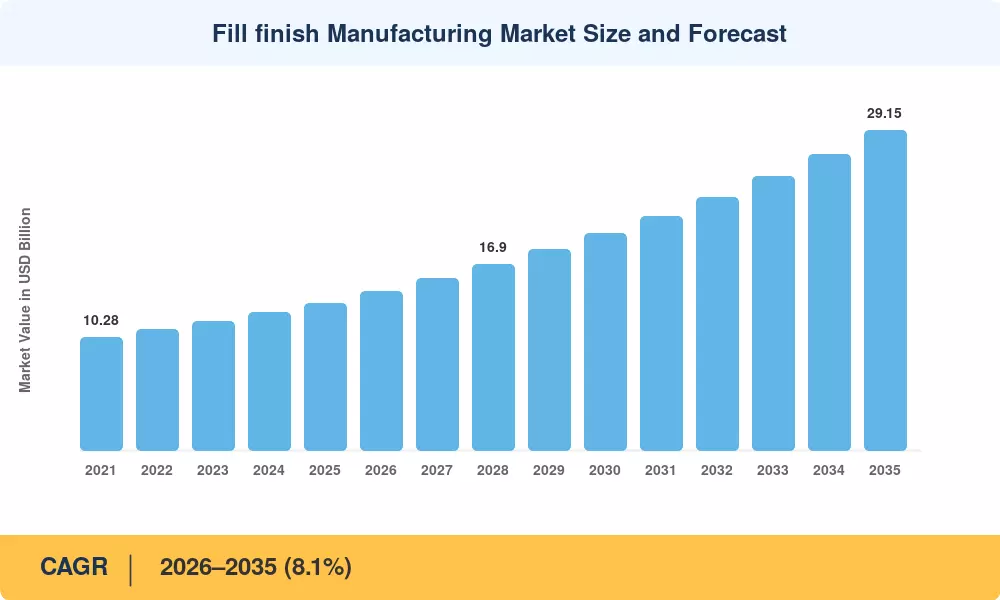

The Fill Finish Manufacturing Market size was valued at USD 13.38 Billion in 2025, and the market is projected to grow from USD 14.46 Billion in 2026 to USD 29.15 Billion by 2035, registering a CAGR of 8.1% during the forecast period 2026–2035. This growth trajectory is fueled by the accelerating shift in pharmaceutical development toward biologics, monoclonal antibodies, and cell and gene therapies — all of which require injectable delivery in sterile environments [1]. The U.S. Biosecure Act and EU GMP Annex 1 revisions have pushed manufacturers to invest heavily in upgraded filling infrastructure, with an estimated USD 8 billion in global capital expenditure committed between 2024 and 2027 alone [2].

The advent of highly automated, isolator-based filling platforms that can process fragile biologic molecules under rigorous contamination-control regimes is quickly replacing legacy oral-solid dose equipment. Robotic handling systems combined with AI-driven predictive maintenance now enable single filling lines to transition between vials, syringes and cartridges in hours rather than days. The trend to ready-to-use (RTU) container components has additionally decreased changeover times and the risk of particulate contamination, and medication inventors have started to reconsider their procurement strategy [3].

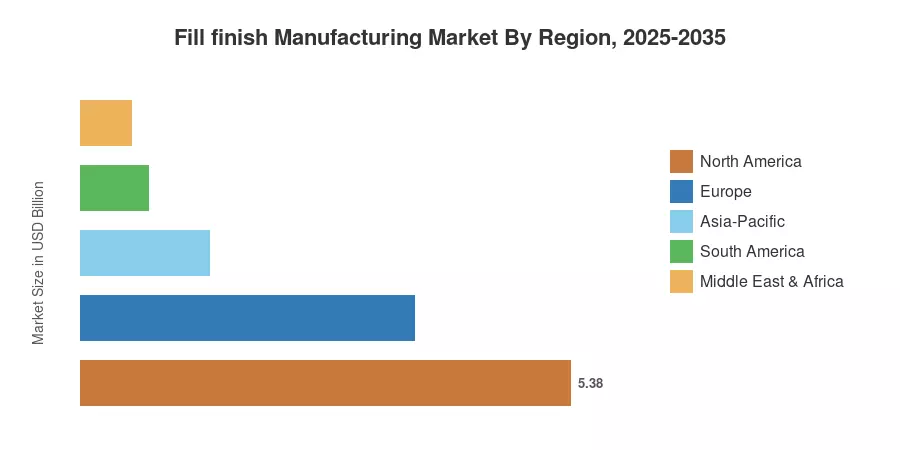

North America accounts for around 40.2% of the fill-finish manufacturing market, with a high concentration of biopharma headquarters and CDMO capacity along the U.S. Eastern Seaboard [4]. 27.4% for Europe, in second place, backed by precision engineering hubs in Germany and Switzerland. The Asia-Pacific is the fastest developing region with a CAGR of 10.6% till 2035, fuelled by the capacity additions in China, India and South Korea [5]. Over the coming decade, contract manufacturers are projected to acquire an increasing part of the worldwide fill-finish capacity as innovators are turning to asset-light models for early-stage pipeline assets.

Key Report Takeaways

• By Product Type

- Consumables — including prefilled syringes, vials, and cartridges — accounted for 58.2% of the Fill Finish Manufacturing Market in 2025, reflecting ongoing demand for high-volume injectable delivery formats.

- Instruments and systems are advancing at a 10.2% CAGR through 2035, as manufacturers adopt integrated and automated filling platforms.

• By End User

- Pharmaceutical and biotechnology companies held 57.3% revenue share of the Fill Finish Manufacturing Market in 2025, driven by in-house capacity for blockbuster biologics.

- Contract manufacturing organizations are expanding at a 9.9% CAGR through 2035, absorbing pipeline overflow from mid-size biotech innovators.

• By Container Material

- Glass containers captured 55.4% of the fill-finish manufacturing market share in 2025, though polymer alternatives are growing at a 10.2% CAGR as cyclic-olefin formats gain regulatory acceptance.

• By Geography

- North America held 40.2% of the fill-finish manufacturing market revenue in 2025.

- Asia-Pacific is the fastest-growing region with a 10.6% CAGR between 2026 and 2035, led by capacity expansion in China and India.

Market Size and Forecast (2021–2035)

MRFR’s value estimation framework employs a bottom-up revenue analysis of consumables, equipment, and service segments triangulated with the corresponding top-down macroeconomic indicators from WHO pharmaceutical expenditure databases, FDA approval trends, and capacity disclosures from CDMOs [6].