Formic Acid Market Summary

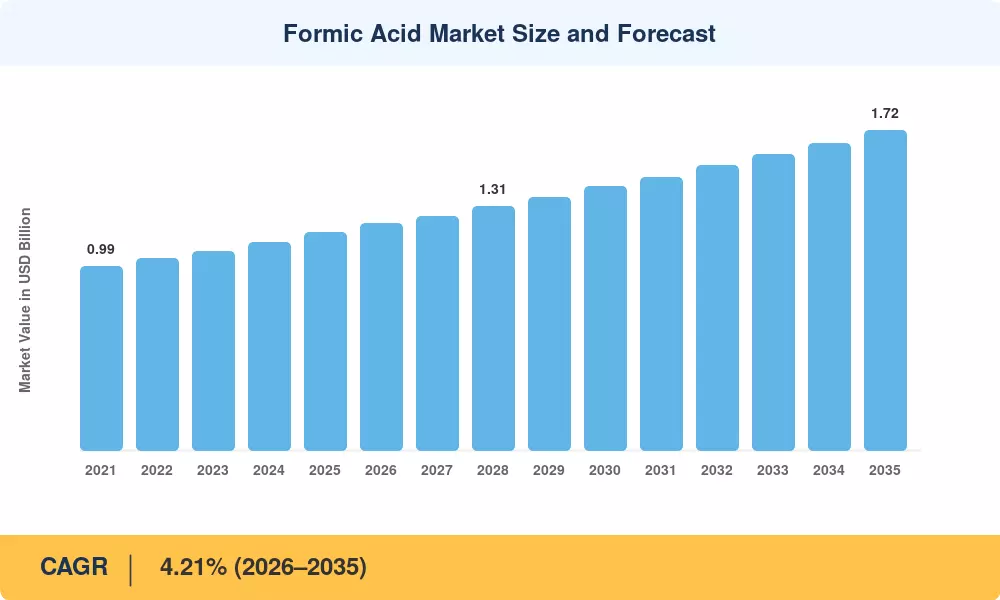

The global Formic Acid Market reached an estimated 1.17 million tons in 2025 and is projected to expand from 1.21 million tons in 2026 to 1.72 million tons by 2035, registering a CAGR of 4.21% during the forecast period. This growth trajectory is anchored in two structural catalysts: the accelerating global shift toward antibiotic-free livestock production—driven by the EU's 2022 ban on prophylactic antibiotic use in feed and similar regulatory pressure from the U.S. FDA's Veterinary Feed Directive—and the rising wave of investment in bio-based chemical intermediates as part of broader decarbonization mandates[2].

A transformation in production technology is reshaping the Formic Acid Market supply chain. Conventional methyl formate hydrolysis, which still accounts for the majority of global output, is increasingly complemented by electrochemical CO₂-to-formic acid conversion pathways. Pilot-scale projects in Germany and Japan have attracted over USD 320 million in combined public-private funding since 2023, signaling a medium-term shift in supply economics for specialty chemical compounds [3][4]. Bio-based production routes for feed preservatives and leather processing chemicals are expanding rapidly, with several European producers targeting carbon-neutral formic acid output by 2030.

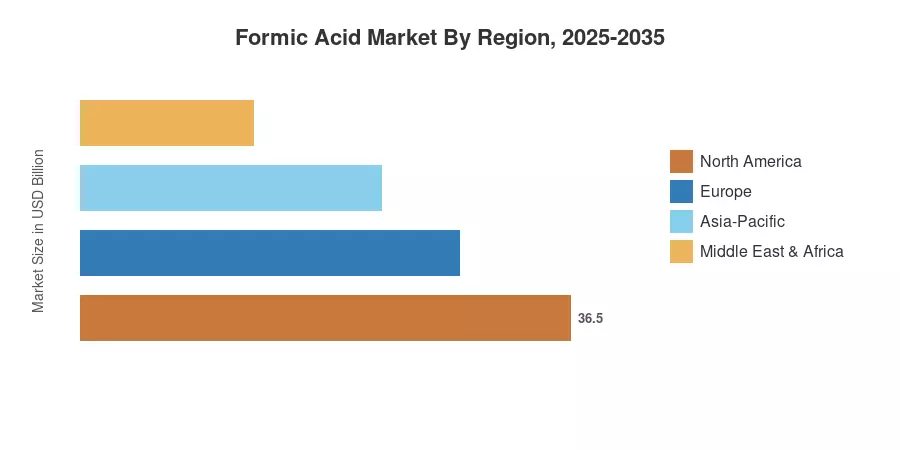

Asia-Pacific commands the dominant position in the Formic Acid Market, holding roughly 56.8% of global consumption in 2025, powered by China's expansive manufacturing base and India's growing demand for agricultural chemicals and rubber processing chemicals. The region is also the fastest-growing, advancing at a 4.89% CAGR through 2035. Europe remains the second-largest consuming region at approximately 21% share, where strict feed safety standards and leather processing chemicals regulations sustain steady demand. North America follows, driven by rising adoption of preservative chemicals and industrial organic acids in livestock and pharmaceutical applications [5][6].

Key Report Takeaways

• By Application

- Animal feed & silage additives led with a 4.48% CAGR through 2035, driven by the global regulatory push to replace antibiotics with acid-based preservatives in livestock nutrition

- Leather tanning accounted for the second-largest share of the Formic Acid Market in 2025, underpinned by expanding footwear production across South and Southeast Asia

- Textile dyeing chemicals applications are gaining traction, particularly in pH-adjustment processes for synthetic fiber manufacturing

• By Production Method

- Methyl formate hydrolysis held 62.4% of the Formic Acid Market share in 2025, reflecting its dominant position in large-scale industrial organic acids production

- Bio-based pathways are projected to grow at 5.02% CAGR, the fastest among all production routes, as producers invest in lower-carbon chemical intermediates

• By Region

- Asia-Pacific dominated the Formic Acid Market with 56.8% volume share in 2025

- Europe is advancing at a 3.72% CAGR, supported by stringent EU regulations on feed preservatives and leather processing chemicals

- North America's demand for preservative chemicals in animal nutrition is rising steadily

Formic Acid Market Size and Forecast (2021–2035)

MRFR's market sizing combines primary interviews with over 45 industry participants, trade data from UN Comtrade and national chemical industry associations, and proprietary demand modeling validated against company filings. Historical figures (2021–2024) reflect reported production and consumption data; the base year (2025) is estimated from H1 actuals extrapolated to full-year totals. Forecast values (2026–2035) apply MRFR's calibrated CAGR with adjustments for anticipated capacity additions and regulatory shifts.