Fortified Dairy Products Market Summary

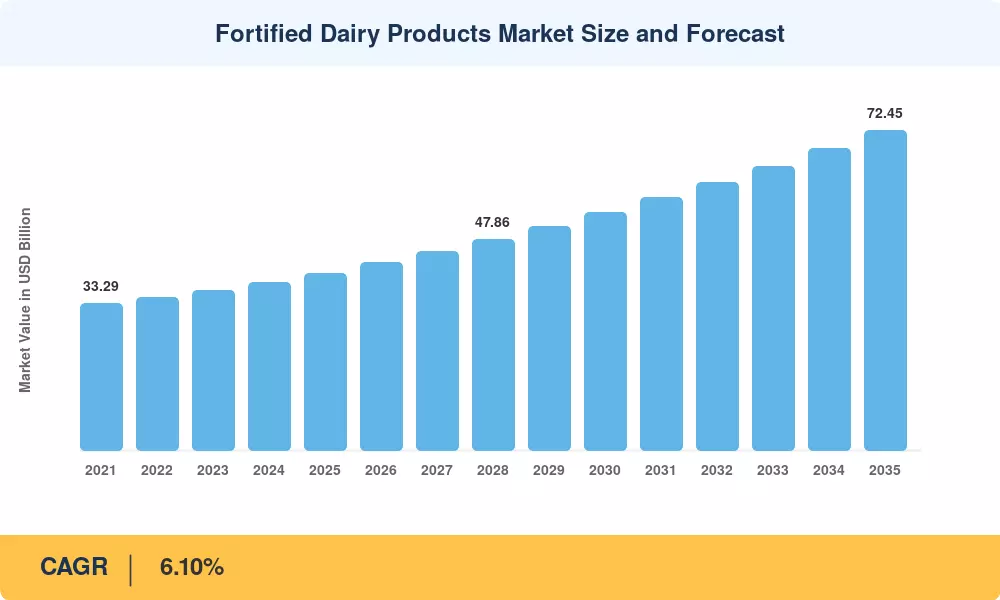

The fortified dairy products market reached USD 40.08 Billion in 2025 and is on track to grow from USD 42.52 Billion in 2026 to USD 72.45 Billion by 2035, registering a 6.10% CAGR across the forecast window. Two forces are propelling this trajectory: government-mandated fortification programs — India's FSSAI, for instance, requires all packaged milk to carry minimum vitamin A and D levels [1] — and a global consumer pivot toward functional foods that deliver immunity and bone-health benefits beyond basic nutrition [2]. Rising per-capita dairy consumption in South and Southeast Asia adds volume momentum that premium pricing alone could not generate.

Legacy dairy processing lines built for simple pasteurization are giving way to microencapsulation and precision-fermentation platforms capable of embedding heat-stable vitamins, minerals, and bioactive peptides without altering taste or shelf life. Investments in this space exceeded USD 1.2 Billion globally between 2022 and 2024, with firms such as Perfect Day and DSM-Firmenich scaling animal-free whey proteins that carry fortification payloads at lower production cost [3]. Regulatory agencies in the EU and the United States have fast-tracked novel-food approvals for these ingredients, cutting time-to-market from thirty-six months to roughly eighteen [4].

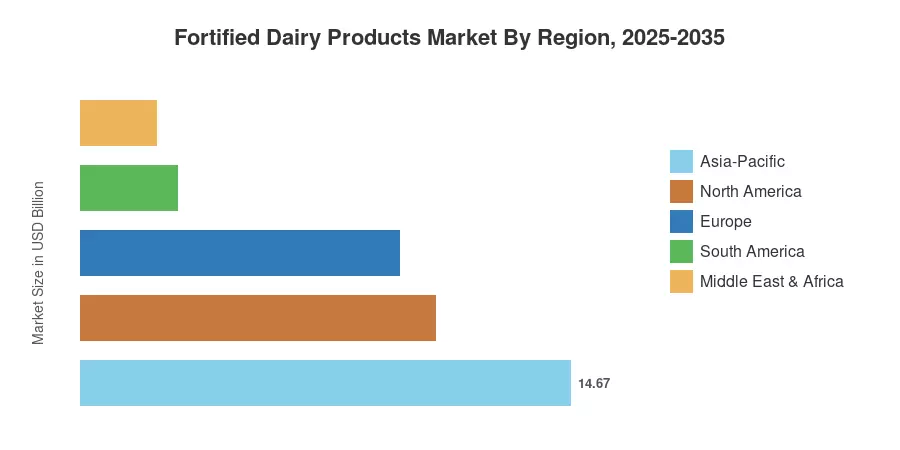

Asia-Pacific commands approximately 36.6% of the fortified dairy products market, driven by large-scale vitamin A and D supplementation campaigns across India and premium health-dairy demand in China. The Middle East & Africa region is the fastest-growing geography, posting a projected 5.70% CAGR as modern retail expansion removes cold-chain barriers. Europe holds the second-largest share at 23.8%, anchored by stringent EU nutrition-labeling regulations that incentivize fortification claims. Over the next decade, personalized nutrition platforms and direct-to-consumer subscription models are poised to reshape how fortified dairy reaches end users worldwide.

Key Report Takeaways

• By Product Type

- Milk accounted for 51.4% of the fortified dairy products market in 2024, reflecting its ubiquity as a daily staple across demographics.

- Yogurt is projected to expand at a 6.20% CAGR through 2035, fueled by probiotic positioning and single-serve convenience formats.

• By Nutrient Type

- Vitamins held 39.8% share of the fortified dairy products market in 2024, led by vitamin D and A additions in fluid milk.

- Probiotics are advancing at a 7.80% CAGR, the fastest among nutrient segments, as gut-health awareness scales globally.

• By Customer Demographics

- Children represented 45.0% of the fortified dairy products market demand in 2024, supported by school-feeding programs and pediatrician endorsements.

- Adults are expanding at a 6.35% CAGR, reflecting growing bone-density and immunity concerns among aging populations.

• By Distribution Channel

- Supermarkets and hypermarkets captured 53.5% share in 2024, benefiting from in-store nutritional labeling and promotional bundling.

- Online retail is set to grow at an 11.50% CAGR as subscription-box dairy services gain traction.

• By Region

- Asia-Pacific led with 36.6% revenue share of the fortified dairy products market in 2024.

- The Middle East & Africa is forecast to post a 5.70% CAGR through 2035, outpacing all other regions.

Market Size and Forecast (2021–2035)

Market Research Future employs a bottom-up revenue model aggregating manufacturer shipments, trade data from FAO and national dairy boards, and proprietary primary surveys of 220+ dairy processors across 35 countries. Historical figures (2021–2024) are validated against customs data and company filings; forecast values (2026–2035) apply the calibrated 6.10% CAGR with adjustments for regulatory phase-ins and infrastructure rollouts in specific geographies.