Frozen Bakery Market Summary

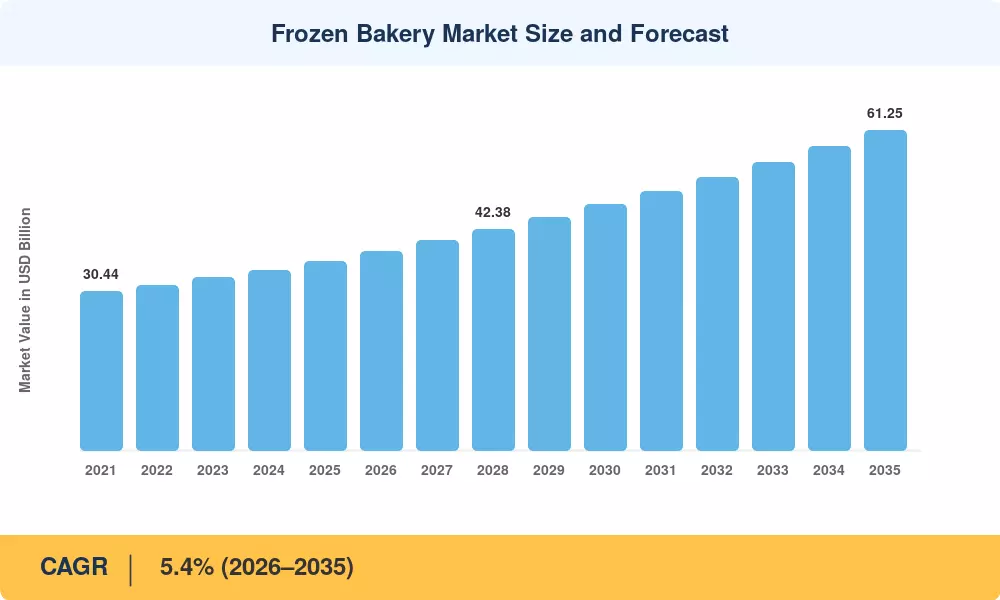

The Frozen Bakery Market reached a valuation of USD 36.20 Billion in 2025 and is projected to grow from USD 38.15 Billion in 2026 to USD 61.25 Billion by 2035, registering a CAGR of 5.4% during the forecast period (2026–2035). Accelerating urbanization, dual-income household proliferation, and sustained investment in cold-chain infrastructure are the primary catalysts propelling this expansion. Government food-safety modernization programs — including the EU's Farm-to-Fork strategy, which has earmarked over EUR 10 Billion for sustainable food-system upgrades — are reinforcing supply-chain resilience and creating a favorable regulatory backdrop for the Frozen Bakery Market [1].

A significant technological shift is underway as legacy batch-baking facilities give way to automated, energy-efficient production lines equipped with cryogenic freezing tunnels and AI-driven quality inspection. Capital expenditure in smart bakery automation exceeded USD 2.8 Billion globally in 2024, according to industry estimates, reflecting manufacturers' urgency to reduce waste and improve throughput [2]. Advances in modified-atmosphere packaging and rapid-freeze technology are extending product shelf life while preserving artisanal taste profiles, a combination that appeals equally to retail consumers and foodservice operators.

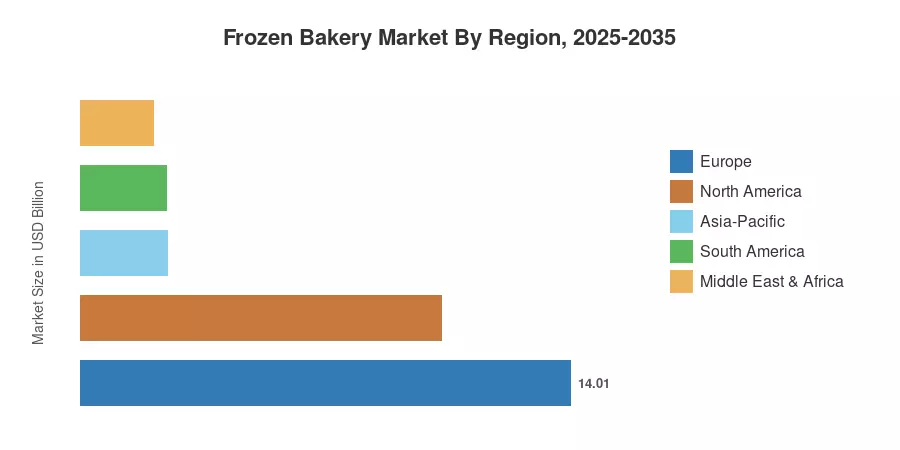

Europe commands the largest share of the Frozen Bakery Market at approximately 38.7% of global revenue in 2025, anchored by strong artisanal traditions in France, Germany, and the Nordic countries. Asia-Pacific is the fastest-growing region, projected to expand at a 6.9% CAGR through 2035, fueled by rapid modern-retail penetration and shifting dietary preferences toward Western-style baked goods. North America holds the second-largest position, driven by robust private-label frozen bakery programs across major grocery chains. The next decade will reward companies that balance scale-driven efficiency with localized product innovation.

Key Report Takeaways

• By Product Type

- Bread accounted for the dominant share of the Frozen Bakery Market in 2025, reflecting the category's role as a daily staple across both retail and foodservice channels.

- Pizza Crust is forecast to register the highest CAGR of 6.7% through 2035, propelled by at-home meal-kit trends and QSR expansion.

- Cakes and Pastries generated an estimated USD 7.96 Billion in 2025, supported by premiumization in celebration and indulgence occasions.

• By Form

- Ready-to-Bake products commanded approximately 42.4% of the Frozen Bakery Market in 2025, favored by in-store bakery operators seeking consistency with minimal labor.

- Ready-to-Proof formats are projected to grow at a 5.6% CAGR through 2035 as artisan-quality positioning gains traction.

• By Distribution Channel

- Off-Trade Retail held 63.3% of global Frozen Bakery Market revenue in 2025, led by hypermarket and supermarket frozen-aisle expansions.

- On-Trade HoReCa is advancing at a 6.1% CAGR through 2035, driven by post-pandemic foodservice recovery and labor-cost mitigation.

• By Region

- Europe led the Frozen Bakery Market with a 38.7% revenue share in 2025, underpinned by mature cold-chain networks and regulatory support.

- Asia-Pacific records the highest projected CAGR at 6.9% during 2026–2035, powered by urbanization and rising disposable incomes.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines top-down revenue analysis from company filings and trade-body data with bottom-up demand modeling across product types, forms, and distribution channels. Historical figures (2021–2024) are calibrated against customs data, retail scanner datasets, and foodservice procurement surveys. Forecast values (2026–2035) incorporate macroeconomic inputs, consumer-trend trajectories, and planned capacity expansions disclosed by leading manufacturers[4].

.webp?v=1785231586)