Functional Flour Market Summary

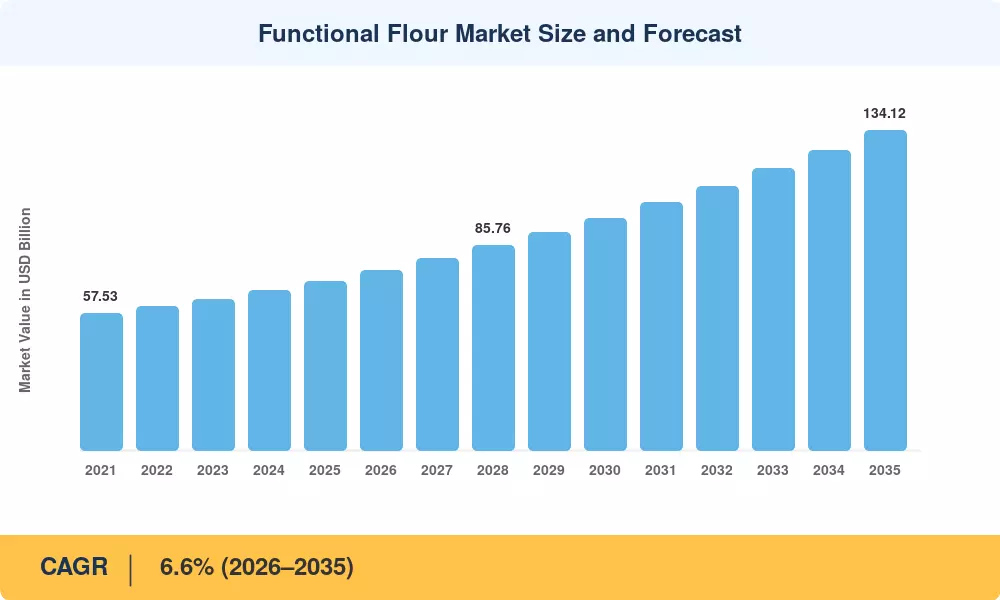

The Functional Flour Market stood at USD 70.80 billion in 2025 and is projected to reach USD 75.47 billion in 2026 before climbing to USD 134.12 billion by 2035, expanding at a compound annual growth rate of 6.6% over the 2026–2035 forecast window. Government-led fortification mandates — including India's Food Safety and Standards Authority directive requiring iron and folic acid enrichment in all commercially milled wheat flour — alongside rising consumer preference for clean-label ingredients have combined to propel the Functional Flour Market forward[2]. Corporate investment in plant-based protein platforms has intensified, with major ingredient houses committing over USD 2.5 billion in capital expenditure toward pulse-milling and modified-starch facilities between 2023 and 2025 [3].

Processing technology is changing the performance of functional flours. [4] Precision extrusion, heat-moisture treatment and enzymatic modification are replacing legacy roller-milling and simple sieving, enabling manufacturers to build particular gelatinization and viscosity profiles without expensive hydrocolloid additions. The European Commission’s 2024 update to Regulation (EC) No 1925/2006 increased the number of nutrients that might be added to foods and led to an increase in reformulation activities across Europe [5].

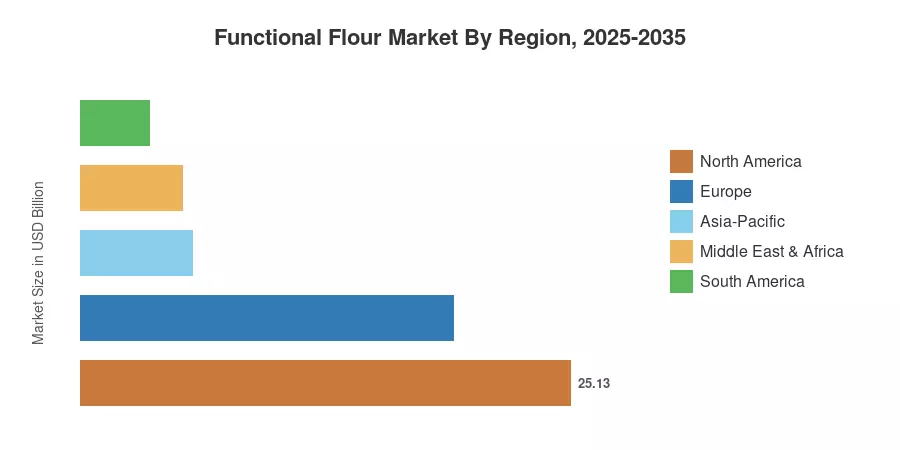

North America had around 35.5% of the Functional Flour Market worldwide in 2025. This is because of the U.S. FDA’s criteria for enrichment and the booming gluten-free retail market [6]. Asia-Pacific is the fastest expanding region, with a CAGR of 8.1% to 2035, driven by population-scale fortification programs and urbanization-induced snack consumption. Europe had the second greatest share at over 27%, driven by clean-label regulation and demand for organic certification.

Key Report Takeaways

• By Source

- Cereals accounted for 58.6% of total Functional Flour Market revenue in 2025, anchored by wheat, rice, and oat-based grades used across bakery and ready-to-eat categories.

- Legume-sourced flours are projected to grow at a 9.3% CAGR through 2035, reflecting strong demand from plant-protein formulators and meat-alternative producers.

• By Application

- Bakery and confectionery represented 43.3% of the Functional Flour Market in 2025, the single largest end-use segment globally.

- Meat alternatives are forecast to register a 7.2% CAGR to 2035 as food-service chains and retail brands scale plant-based product lines.

• By Geography

- North America led the Functional Flour Market with 35.5% revenue share in 2025.

- Asia-Pacific is set to expand at an 8.1% CAGR between 2026 and 2035, making it the world's fastest-growing regional market.

Functional Flour Market Size and Forecast (2021–2035)

Market Research Future (MRFR) sizing projections are derived from bottom-up revenue modeling of more than 120 worldwide flour processors and top-down validation against FAO production figures, national trade databases and proprietary primary surveys of formulators, millers and distributors[7].

.webp?v=1783518056)