Banana Flour Market Summary

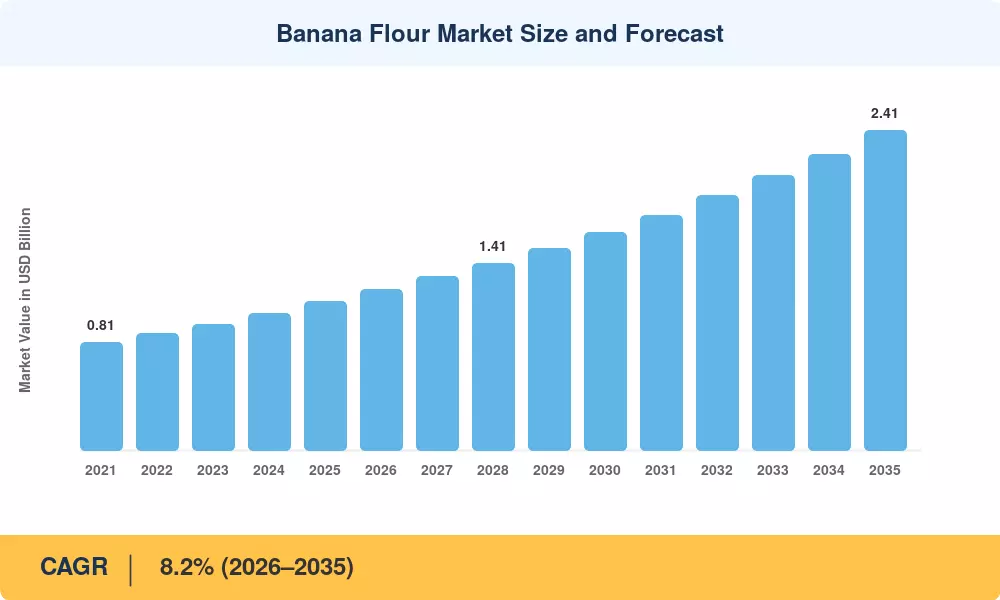

The Banana Flour Market reached an estimated USD 1.12 billion in 2025 and is projected to grow from USD 1.21 billion in 2026 to USD 2.41 billion by 2035, registering a CAGR of 8.2% during the forecast period (2026–2035). Two forces are accelerating this trajectory: the global surge in celiac and gluten-sensitivity diagnoses — now affecting roughly 1.4% of the world population according to WHO data [2] — and clean-label reformulation mandates that food manufacturers face across the EU and North America [3]. Consumer spending on gluten-free banana flour baking products alone surpassed USD 340 million in 2024, underscoring how dietary health trends translate directly into ingredient demand.

Tropical banana flour production is undergoing a technology-led transformation. Traditional sun-drying and stone-milling — still dominant in parts of Sub-Saharan Africa and Southeast Asia — are steadily giving way to drum-drying, spray-drying, and controlled-atmosphere dehydration lines that preserve green banana resistant starch content above 40% by weight [4]. Investment in mechanized processing capacity topped USD 180 million cumulatively between 2022 and 2024, with notable capital deployments in India, Ecuador, and Brazil [5].

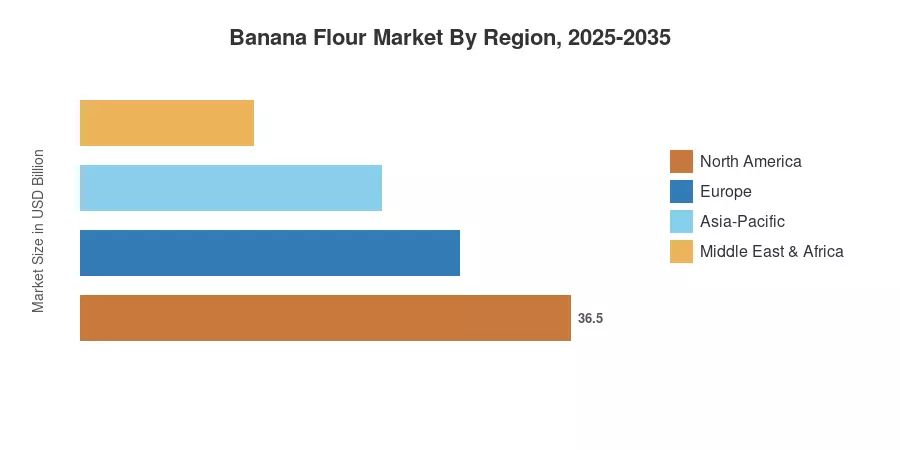

North America commands approximately 31% of the Banana Flour Market, driven by the clean-label movement and robust retail distribution. Asia-Pacific is the fastest-growing region at a projected CAGR of 10.1%, fueled by abundant raw-material supply and expanding middle-class health consciousness. Europe holds roughly 26% share, buoyed by EU Novel Food Regulation updates that streamlined banana flour food ingredient approvals in 2023 [6]. The decade ahead will reward players who integrate backward into plantation sourcing while scaling forward into value-added blends.

Key Report Takeaways

• By Product Type

- Green banana flour — the unripe variant prized for its green banana resistant starch profile — accounts for a CAGR of 9.0% through 2035, outpacing ripe banana flour due to functional health positioning

- Ripe banana flour holds an estimated USD 290 million value in 2025, primarily serving the confectionery and infant-nutrition segments in South America

- Organic-certified banana flour is the Banana Flour Market's premium tier, capturing roughly 18% share globally as retailers prioritize non-GMO shelf positioning

• By Application

- Bakery & snacks represent the dominant application for the Banana Flour Market, commanding approximately 38% of total revenue, driven by gluten-free banana flour baking reformulation

- Baby food & infant nutrition is expanding at a CAGR of 9.4%, reflecting pediatric dietary guidelines that favor banana flour nutritional benefits over rice-based alternatives

• By Region

- North America leads the Banana Flour Market with ~31% share, anchored by U.S. specialty-grocery and e-commerce channels

- Asia-Pacific registers the strongest growth trajectory at 10.1% CAGR, supported by tropical banana flour production hubs in India, the Philippines, and Indonesia

- Europe contributes approximately USD 290 million in 2025, with Germany and the UK as principal demand centers

Market Size and Forecast (2021–2035)

The Banana Flour Market size estimates below derive from primary interviews with 45+ flour millers, distributors, and food manufacturers, supplemented by trade-flow databases (UN Comtrade), company filings, and regional agricultural ministry data [7]. Historical figures (2021–2024) reflect actuals; the base year (2025) is estimated; 2026–2035 values are forecast at an 8.2% CAGR.