Gasoline Direct Injection Market Summary

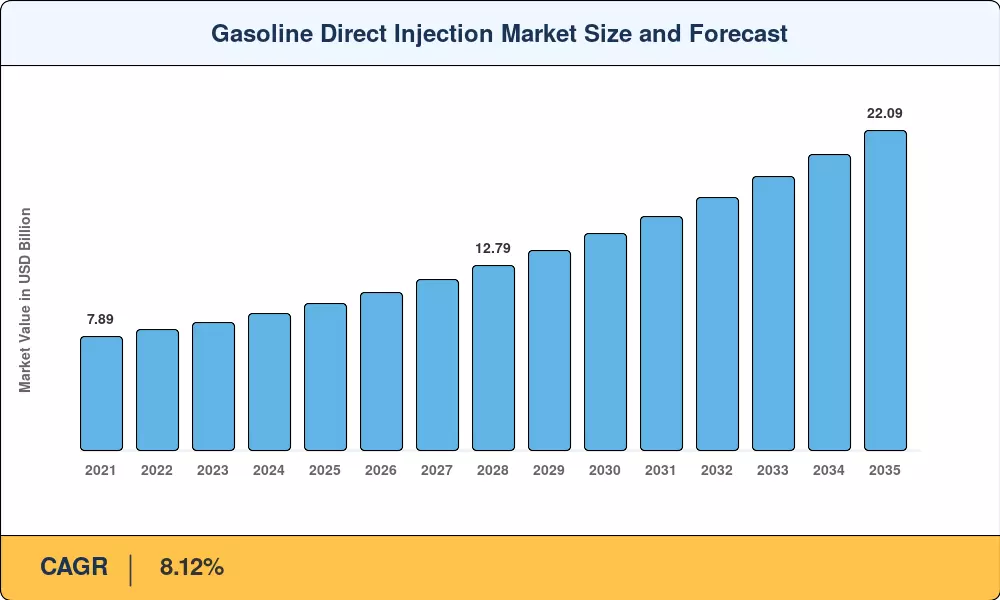

The Gasoline Direct Injection Market reached an estimated USD 10.12 Billion in 2025 and is projected to grow from USD 10.94 Billion in 2026 to USD 22.09 Billion by 2035, registering a CAGR of 8.12% across the forecast period (2026–2035). Tightening emission mandates — including Euro 7 particulate number limits in the EU and China's CN7 framework — are the single strongest catalyst, compelling automakers to retrofit or redesign powertrains around high-pressure fuel delivery architectures. Infrastructure investment commitments from OEMs exceeding USD 8 Billion between 2024 and 2028 reinforce the capital pipeline behind this technology transition [1].

A sweeping shift away from traditional port-fuel-injection systems is reshaping combustion engineering. Engine downsizing and turbocharging strategies depend on precise fuel metering at pressures exceeding 350 bar, and next-generation piezoelectric injector platforms now deliver sub-10-micron droplet size for superior atomization. The European Commission's regulatory roadmap through 2030, paired with India's BS6 Phase II rollout, has prompted leading Tier-1 suppliers to scale manufacturing capacity by 15–20% annually [2][3].

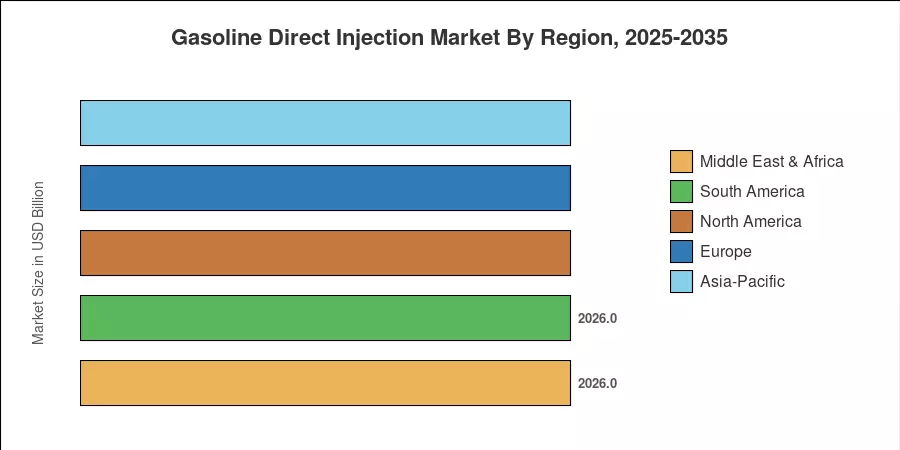

Asia-Pacific leads the Gasoline Direct Injection Market with approximately 41% of global revenue, driven by China's dominant vehicle production volumes. Europe follows with roughly 28% share, anchored by the stringent regulatory landscape. North America, accounting for around 22%, benefits from strong SUV and light-truck demand that favors direct-injection powertrains. These three regions collectively steer product roadmaps and pricing dynamics for the decade ahead.

Key Report Takeaways

• By Component

- Fuel injectors accounted for the largest share — approximately 38% — of the Gasoline Direct Injection Market in 2024, reflecting high unit content per engine.

- Sensors are poised to register a CAGR of 8.24% through 2035, driven by increasing demand for closed-loop combustion feedback in downsized engines.

• By Engine Type

- Inline-4 configurations dominate the Gasoline Direct Injection Market with roughly 67% share, aligning with the global preference for compact four-cylinder turbo architectures.

- Inline-3 engines are forecast to grow at the fastest pace (8.27% CAGR), driven by micro-car and mild-hybrid adoption in emerging economies.

• By Vehicle Type

- SUVs and MUVs commanded approximately 41% of the Gasoline Direct Injection Market value in 2024, as consumer preference for utility segments keeps displacement — and injector content — elevated.

• By Sales Channel

- OEM channels retained a dominant share exceeding 83% in 2024, while the aftermarket channel is growing at an 8.29% CAGR amid rising replacement demand.

• By Region

- Asia-Pacific held the leading position in the Gasoline Direct Injection Market with 41% share; the region's CAGR of 8.31% also makes it the fastest-growing geography through 2035.

Gasoline Direct Injection Market Size and Forecast (2021–2035)

Market sizing combines bottom-up component-level revenue estimates with top-down validation against OEM production data, regulatory impact modelling, and Tier-1 supplier disclosures. Historical figures (2021–2024) reflect actual shipment revenues, while the forecast (2026–2035) applies a compound annual growth model calibrated to emission-regulation timelines and powertrain electrification adoption curves.