Gel Documentation Systems Market Summary

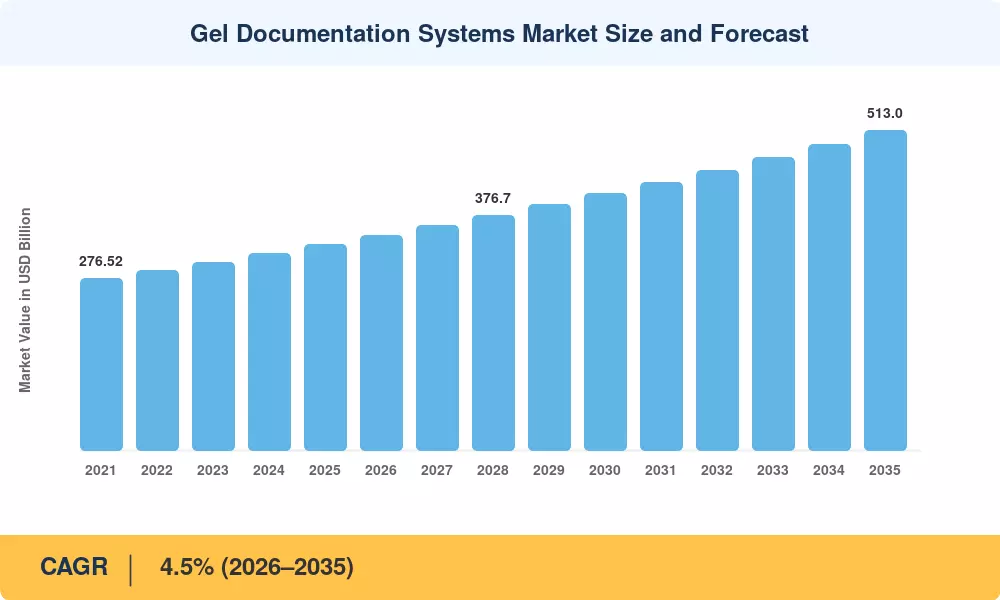

The Global Gel Documentation Systems Market size was valued at USD 330 Million in 2025, and the market is projected to grow from USD 345 Million in 2026 to USD 513 Million by 2035, registering a CAGR of 4.5% during the forecast period 2026–2035. Rising global cancer incidence — with GLOBOCAN recording over 20 million new cases in 2023 alone [2] — has intensified demand for molecular and genetic analysis tools, positioning gel imaging analysis as a critical capability in modern life-science workflows. Government investments in genomics infrastructure, including the U.S. National Institutes of Health's USD 1.6 billion allocation to the All of Us precision-medicine program [3], directly reinforce procurement cycles for electrophoresis imaging equipment across academic and clinical laboratories.

A technological transition is reshaping the Gel Documentation Systems Market as legacy UV-transilluminator setups give way to LED-based, digitally integrated platforms. Modern DNA gel documentation platforms now feature automated exposure optimization, cloud-based image archiving, and AI-assisted band quantification — capabilities that analog systems simply cannot match. Instrument refresh cycles have shortened to five-to-seven years as labs pursue compliance with 21 CFR Part 11 data-integrity mandates [4], accelerating replacement demand for next-generation agarose gel imaging software suites.

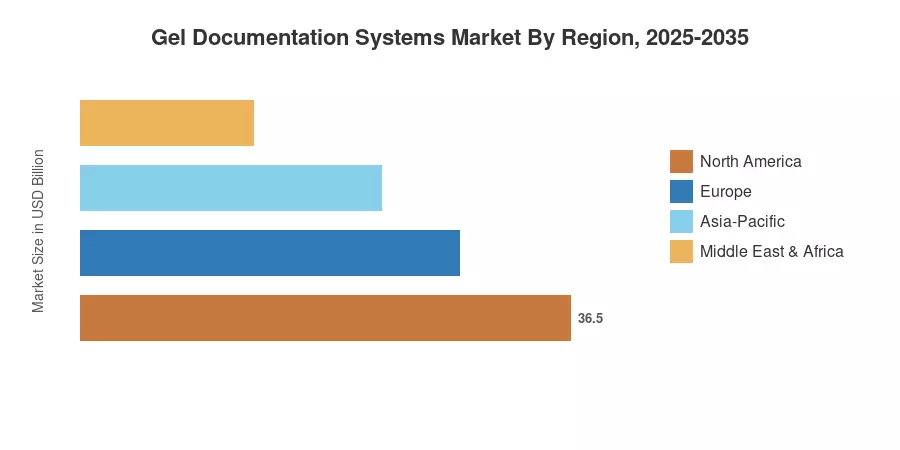

North America commands roughly 38% of the Gel Documentation Systems Market, supported by dense concentrations of NIH-funded research institutions and pharmaceutical R&D campuses. Asia-Pacific is the fastest-growing region at an anticipated CAGR of 5.8%, driven by China's 14th Five-Year Plan investments in biotechnology and India's expanding network of diagnostic laboratories [5]. Europe holds the second-largest share at approximately 27%, anchored by Germany's Fraunhofer institutes and the UK's Genomics England initiative. The decade ahead will be shaped by how quickly UV gel visualization gives way to multi-mode, software-driven documentation platforms.

Key Report Takeaways

• By Products

- Instruments held the largest segment share in 2025, accounting for roughly 52% of the Gel Documentation Systems Market, driven by ongoing laboratory build-outs and equipment replacement cycles.

- Software is the fastest-growing product category with a projected CAGR of 5.9%, reflecting the shift toward integrated gel imaging analysis workflows.

• By Application

- Nucleic acid quantification captured approximately 62% of total demand, reinforcing its role as the primary use case for DNA gel documentation across academic and clinical settings.

- Protein quantification applications are gaining traction at a CAGR of 4.8%, fueled by proteomics research expansion in the Gel Documentation Systems Market.

• By Region

- North America generated USD 125 million in 2025, maintaining its dominance in the Gel Documentation Systems Market through sustained federal research funding.

- Asia-Pacific is projected to register the highest regional CAGR of 5.8% through 2035, underpinned by the rapid expansion of electrophoresis imaging infrastructure in China and India.

Market Size and Forecast (2021–2035)

Market sizing relies on a bottom-up methodology combining laboratory instrument shipment data, vendor-reported revenues, and institutional procurement records from over 40 countries. Historical figures draw on customs databases and annual reports; forecast estimates apply regression-adjusted growth models calibrated against genomics R&D spending trends.