Gene Panel Market Summary

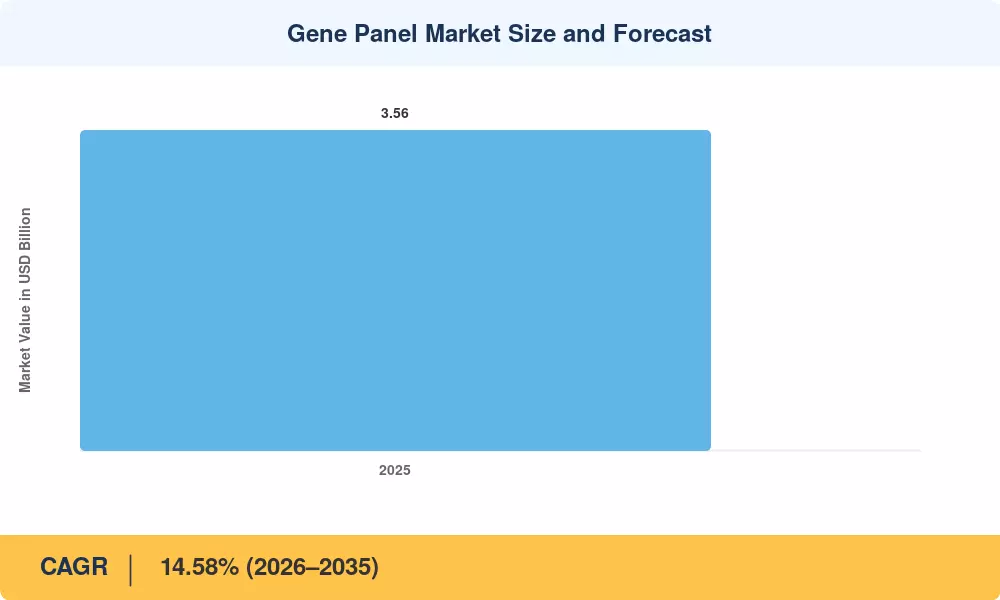

The Global Gene Panel Market size was valued at USD 3.56 Billion in 2025, and the market is projected to grow from USD 4.12 Billion in 2026 to USD 14.03 Billion by 2035, registering a CAGR of 14.58% during the forecast period 2026–2035. This trajectory reflects a structural shift in precision medicine, driven by the Centers for Medicare & Medicaid Services (CMS) National Coverage Determination 90.2, which broadened reimbursement for next-generation sequencing panels across oncology indications [1]. Private insurers have followed suit, reducing out-of-pocket burdens and unlocking repeat testing volumes for multi-gene cancer testing workflows.

A quiet revolution is reshaping diagnostic laboratories worldwide. Legacy single-gene Sanger sequencing is giving way to massively parallel targeted genomic sequencing platforms that interrogate dozens to hundreds of genes simultaneously. The NIH All of Us Research Program alone committed over USD 1.4 Billion toward population-scale genomics, expanding the addressable universe for hereditary disease gene panels and pharmacogenomic profiling [2]. Full-stack providers are bundling sequencing hardware, bioinformatics pipelines, and clinical reporting into single-vendor solutions — accelerating consolidation across the Gene Panel Market.

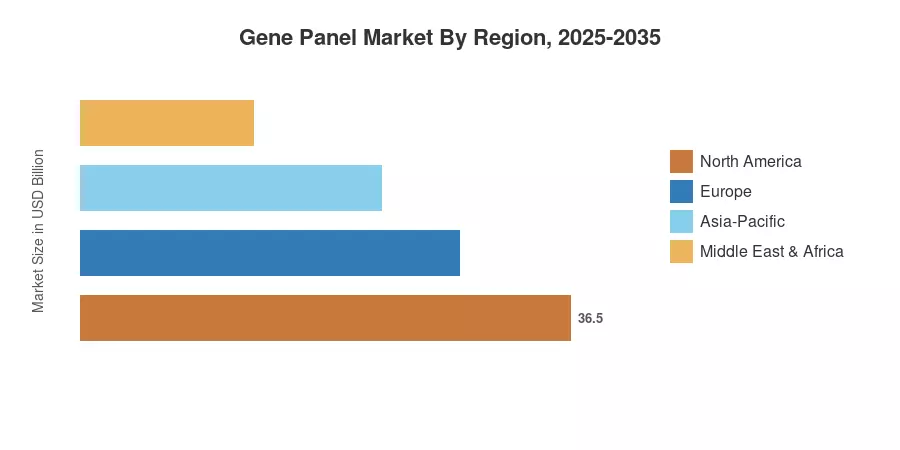

North America commanded a 38.95% revenue share of the Gene Panel Market in 2025, anchored by robust payer infrastructure and high oncology gene panel testing adoption. Asia-Pacific stands out as the fastest-growing region at a 15.25% CAGR through 2035, propelled by government-backed genomics programs in China, India, and Japan. Europe holds the second-largest share, benefiting from NHS Genomic Medicine Service expansion and the EU's 1+ Million Genomes Initiative. The decade ahead promises broader accessibility as next-generation sequencing panels penetrate community hospitals and emerging economies alike.

Key Report Takeaways

• By Product & Services

- Test Kits dominated the Gene Panel Market with a 60.05% revenue share in 2025, reflecting strong demand for ready-to-use targeted genomic sequencing kits across clinical laboratories.

- Testing Services are forecast to expand at a 15.23% CAGR through 2035, driven by outsourced oncology gene panel testing from smaller hospital systems.

• By Technique

- Amplicon-based workflows captured 65.46% of the Gene Panel Market share in 2025, favored for their cost efficiency in multi-gene cancer testing applications.

- Hybridization capture approaches are poised to grow at a 15.16% CAGR to 2035 as larger panels and hereditary disease gene panels demand higher uniformity of coverage.

• By Application

- Cancer Risk Assessment accounted for 52.45% of the Gene Panel Market in 2025, reflecting widespread NCCN guideline adoption for tumor profiling.

- Pharmacogenetics is projected to advance at a 15.11% CAGR through 2035, aided by growing preemptive prescribing programs.

• By End User

- Hospitals & Clinics held a 51.98% share of the Gene Panel Market in 2025, anchored by in-house molecular pathology departments.

- Diagnostic Laboratories are set to grow at a 14.99% CAGR to 2035 as reference labs scale high-throughput next-generation sequencing panels.

• By Region

- North America led the Gene Panel Market with 38.95% revenue in 2025, supported by favorable CMS reimbursement policies.

- Asia-Pacific is forecast to expand at a 15.25% CAGR to 2035, driven by national genomics initiatives and rising oncology gene panel testing demand.

Gene Panel Market Size and Forecast (2021–2035)

MRFR's market sizing integrates primary interviews with laboratory directors, procurement managers, and sequencing platform vendors, supplemented by secondary analysis of company filings, CMS claims data, and regional genomics databases. Historical figures (2021–2024) are validated against published revenues of leading manufacturers, while the forecast (2026–2035) employs a bottom-up model calibrated to installed sequencing base, test volumes, and average selling prices across next-generation sequencing panels.