Hairy Cell Leukemia Market Summary

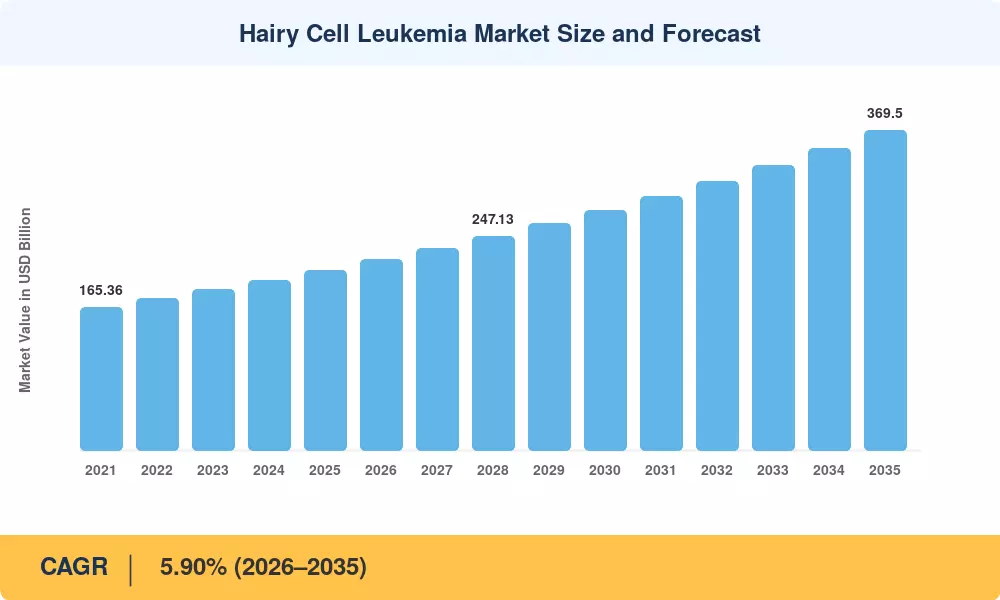

The Global Hairy Cell Leukemia Market size was valued at USD 208.00 Million in 2025, and the market is projected to grow from USD 220.40 Million in 2026 to USD 369.50 Million by 2035, registering a CAGR of 5.90% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the U.S. FDA's continued use of accelerated approval pathways for ultra-rare hematologic indications and the European Medicines Agency's revised orphan-drug incentive framework, which extended market exclusivity to twelve years for therapies serving populations below one in 50,000 [1]. These regulatory structures give pharmaceutical sponsors pricing flexibility that would be untenable in larger oncology segments, sustaining per-patient revenue well above USD 80,000 annually in North America and Western Europe.

A pronounced shift from purine-analog monotherapy toward precision-oncology combinations is redefining clinical practice in the hairy cell leukemia market. BRAF V600E–targeted agents, initially approved for melanoma, are now routinely combined with anti-CD20 monoclonal antibodies to achieve measurable residual disease negativity in first-line and relapsed settings alike [2]. Flow-cytometry-based MRD monitoring has matured from a research tool into a reimbursable companion diagnostic in several G7 countries, tightening the feedback loop between treatment selection and outcome measurement. The transition to a streamlined two-hour intravenous push administration of cladribine has lowered infusion-center burden and improved outpatient throughput, directly influencing treatment-setting economics.

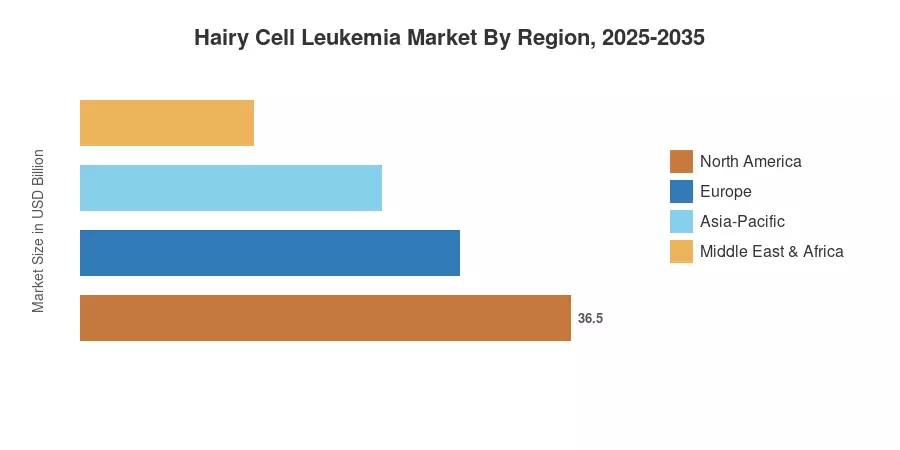

North America commands 42.1% of the hairy cell leukemia market, anchored by academic medical centers running investigator-initiated trials and by payer willingness to reimburse off-label combination regimens. Europe follows with 28.5% share, led by Germany's early-access compassionate-use programs. Asia-Pacific is the fastest-growing region at a 7.55% CAGR, propelled by South Korea's 2026 expansion of hematology benefits and China's National Reimbursement Drug List update that broadened coverage for ultra-rare therapies. The hairy cell leukemia market is poised to benefit from deepening diagnostic penetration in middle-income countries over the next decade.

Key Report Takeaways

• By Product Type

- Therapy-type products held 65.8% revenue share of the hairy cell leukemia market in 2025, driven by orphan-drug pricing and the dominance of purine-analog and BRAF-inhibitor regimens.

- Diagnostic modalities are advancing at an 8.40% CAGR through 2035 as flow-cytometry MRD panels and next-generation sequencing companion diagnostics gain reimbursement traction.

• By Route of Administration

- Intravenous delivery commanded 54.5% share of the hairy cell leukemia market in 2025, reflecting the entrenched role of IV cladribine and rituximab infusions.

- Oral formulations are projected to expand at an 8.60% CAGR over 2026–2035 as BRAF and BTK inhibitor uptake accelerates in relapsed settings.

• By Treatment Setting

- First-line therapy accounted for 56.1% of the hairy cell leukemia market share in 2025.

- Relapsed or refractory care is forecast to grow at an 8.80% CAGR through 2035, reflecting longer patient survival and second-line combination adoption.

• By End User

- Hospitals held 59.2% share in 2025, consolidating infusion and diagnostic services under one roof.

- Diagnostic laboratories are projected to grow at an 8.50% CAGR through 2035 as decentralized MRD testing expands.

• By Region

- North America captured 42.1% share of the hairy cell leukemia market in 2025.

- Asia-Pacific is projected to grow at a 7.55% CAGR between 2026 and 2035, outpacing all other regions.

Hairy Cell Leukemia Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates proprietary primary surveys of hematology-oncology prescribers, secondary data from national cancer registries (SEER, EUROCARE, GLOBOCAN), pharmaceutical revenue disclosures, and payer claims databases. Historical figures (2021–2024) reflect audited actuals; the base year 2025 blends confirmed Q1–Q3 sales with Q4 estimates. Forecast values (2026–2035) apply a calibrated CAGR adjusted for anticipated regulatory milestones, pipeline events, and regional reimbursement expansions across the hairy cell leukemia market.

.webp?v=1782976210)