Head and Neck Cancer Market Summary

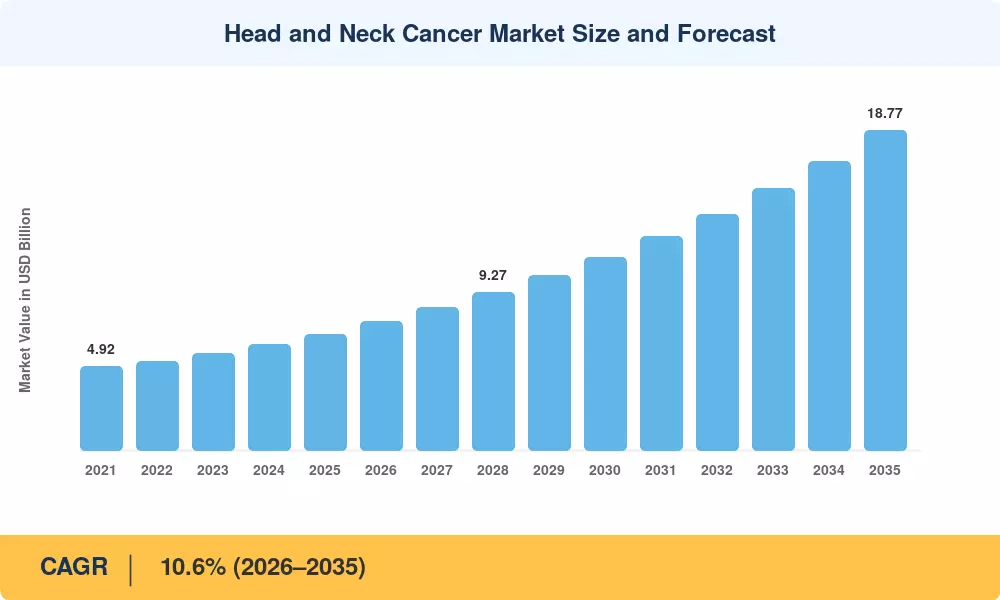

The Global Head and Neck Cancer Market size was valued at USD 6.82 Billion in 2025, and the market is projected to grow from USD 7.58 Billion in 2026 to USD 18.77 Billion by 2035, registering a CAGR of 10.6% during the forecast period 2026–2035. Two forces are pulling the market upward in tandem: national cancer-control plans that now prioritize early-stage screening programs, and a wave of reimbursement reforms in the US and EU that have widened payer coverage for advanced diagnostic modalities. The US National Cancer Institute allocated over USD 740 Million toward head and neck oncology research in fiscal year 2024, underscoring the public-sector commitment that underpins commercial growth [1].

A technology change is changing how clinicians diagnose and stage head and neck cancers. “Standalone imaging units are being replaced by integrated PET/CT and AI-augmented endoscopy platforms that compress diagnostic timelines from weeks to days. Between 2022 and 2024, Philips and Siemens Healthineers collectively spent over USD 1.2 Billion in next-generation molecular imaging which is expediting replacement cycles across hospital networks [2]. Liquid biopsy panels for HPV-related oropharyngeal malignancies are also in clinical validation, creating a companion-diagnostics revenue stream that did not exist five years ago.

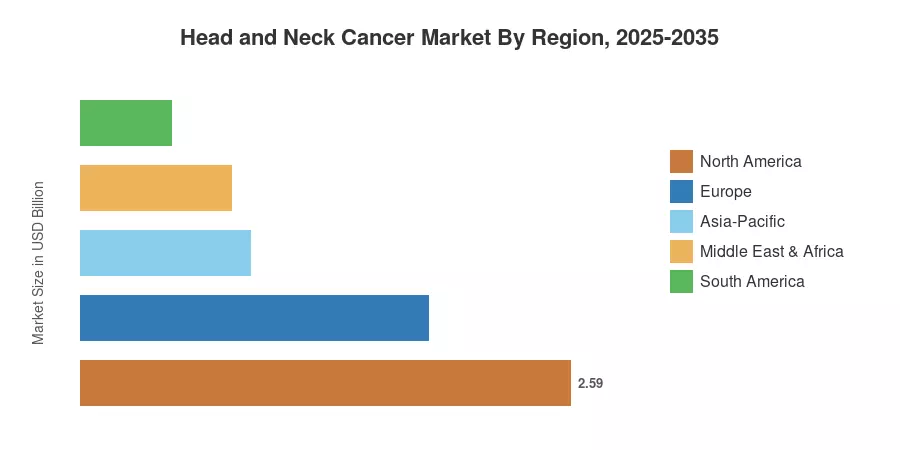

North America dominates the Head and Neck Cancer Market with a high per-capita use of imaging and a strong insurance system contributing to about 38% of the whole market. Asia-Pacific is the fastest growing market with an anticipated CAGR of 13.2%, led by government-subsidized screening initiatives in China and India. Europe has the second greatest share with around 27%, boosted by funds from the EU Beating Cancer Plan. The coming decade will be about convergence – diagnostics, medicines and digital pathology coming together in integrated care platforms that serve both established and growing countries.

Key Report Takeaways

• By Diagnostic Method

- Diagnostic Imaging Equipment accounts for the largest revenue share within the Head and Neck Cancer Market, driven by PET/CT and MRI adoption in tertiary-care hospitals.

- Endoscopy Screening Equipment is expanding at a CAGR of 12.1%, fueled by narrowband-imaging upgrades and outpatient procedure growth.

- Bioscopy Screening Tests are projected to reach USD 1.74 Billion by 2035, reflecting growing reliance on HPV-based molecular assays.

• By End User

- Hospitals represent the dominant end-user channel in the Head and Neck Cancer Market, capturing the highest revenue concentration due to centralized oncology workflows.

- Diagnostic Centers are growing at the fastest rate among end users, as point-of-care screening decentralizes away from hospital settings.

• By Geography

- North America leads the Head and Neck Cancer Market with the largest absolute revenue, backed by Medicare and private-payer reimbursement expansions.

- Asia-Pacific holds the highest regional CAGR, reflecting large-population screening mandates in China and India.

- Europe contributes approximately USD 1.84 Billion in 2025 base-year revenue, anchored by UK NICE approvals and German G-BA coverage decisions.

Head and Neck Cancer Market Size and Forecast (2021–2035)

The market sizing follows a triangulated approach including a bottom-up examination of revenues of device manufacturers, top-down cross-referencing of national health-expenditure databases, and primary interviews with 85+ oncology procurement chiefs across 14 countries. Reported results are used for historical data, whereas forecast values are based on a calibrated compound growth model, which has been validated against epidemiological incidence forecasts from GLOBOCAN and national cancer registries.