Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

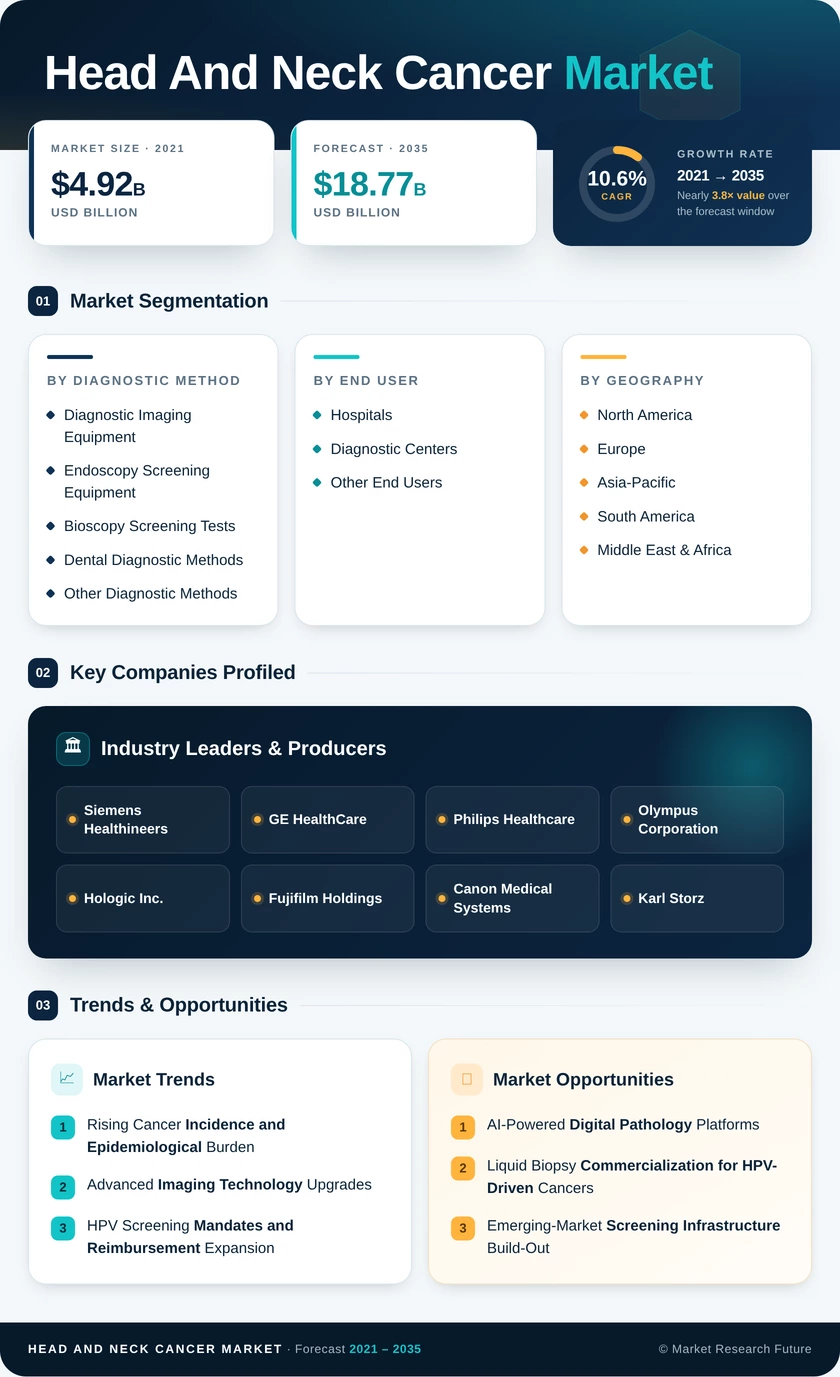

| By Diagnostic Method | Diagnostic Imaging Equipment, Endoscopy Screening Equipment, Bioscopy Screening Tests, Dental Diagnostic Methods, Other Diagnostic Methods | Diagnostic Imaging Equipment | Endoscopy Screening Equipment |

| By End User | Hospitals, Diagnostic Centers, Other End Users | Hospitals | Diagnostic Centers |

| By Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Diagnostic Method

| Sub-Segment | Key Trend |

| Diagnostic Imaging Equipment | AI-integrated PET/CT and MRI platform upgrades driving replacement cycles |

| Endoscopy Screening Equipment | Narrowband imaging and autofluorescence enabling office-based screening |

| Bioscopy Screening Tests | HPV molecular assays and liquid biopsy panels expanding clinical adoption |

| Dental Diagnostic Methods | Chair-side oral cancer visual screening gaining traction in primary care |

| Other Diagnostic Methods | Emerging ctDNA and multi-analyte molecular platforms in early commercialization |

Diagnostic Imaging Equipment holds the largest revenue share, reflecting the central role of cross-sectional imaging in head and neck cancer staging and surveillance. Endoscopy Screening Equipment is the fastest-growing sub-segment, driven by the clinical and economic advantages of minimally invasive outpatient procedures that reduce dependence on hospital-based imaging suites.

By End User

| Sub-Segment | Key Trend |

| Hospitals | Multidisciplinary tumor boards concentrate diagnostic and treatment decision-making |

| Diagnostic Centers | Payer incentives and patient preference accelerating outpatient screening migration |

| Other End Users | Research laboratories and ambulatory surgical centers contributing niche volumes |

Hospitals remain the dominant end-user channel due to the complexity of head and neck cancer workups, which require coordinated radiology, pathology, and surgical consultation. Diagnostic Centers are gaining share at the fastest rate as reimbursement structures increasingly favor lower-cost-of-care ambulatory settings for initial screening and follow-up surveillance.