Health Supplements Market Summary

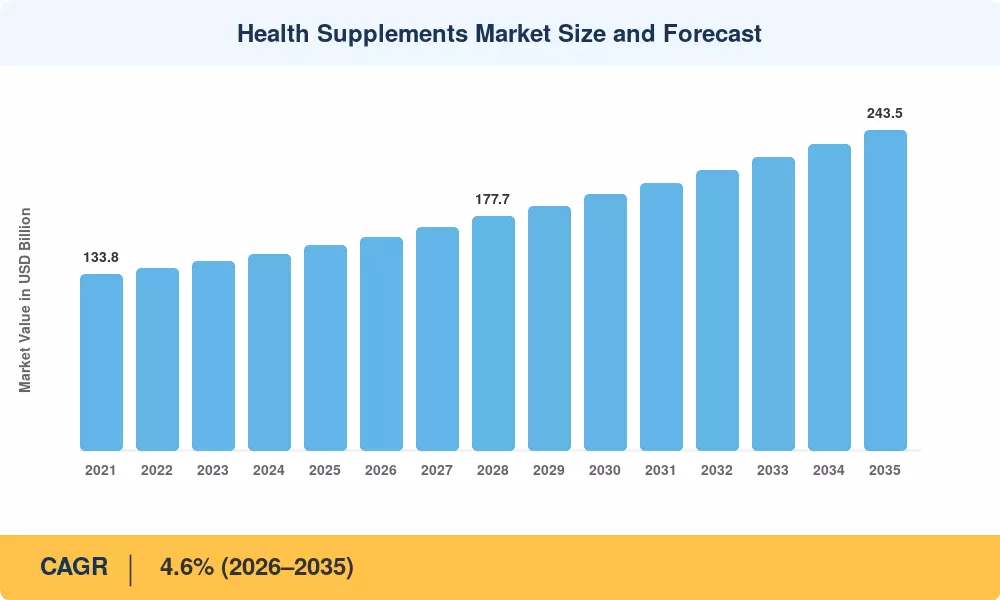

The Global Health Supplements Market size was valued at USD 155.8 Billion in 2025, and the market is projected to grow from USD 162.4 Billion in 2026 to USD 243.5 Billion by 2035, registering a CAGR of 4.6% during the forecast period 2026–2035. This expansion is anchored in two structural catalysts: the World Health Organization's 2023 Global Action Plan on non-communicable diseases, which pushed over 40 national governments to integrate preventive nutrition into public health mandates, and the cumulative USD 14.2 Billion in venture capital deployed into personalized nutrition startups between 2021 and 2024 [2].

The Health Supplements Market is witnessing a fundamental shift away from legacy pill-and-capsule formats toward advanced delivery systems. Gummy formulations, liquid shots, and functional beverages now account for a rapidly growing share of new product launches, driven by consumer demand for better taste and bioavailability. Pectin-based gummy matrices have unlocked the vegan demographic, while microencapsulation technologies are improving nutrient stability across shelf-life windows [3]. The U.S. FDA's expanded GRAS pathway for novel probiotic strains has reduced time-to-market for gut-health products by an estimated 18 months compared to 2019 benchmarks [4].

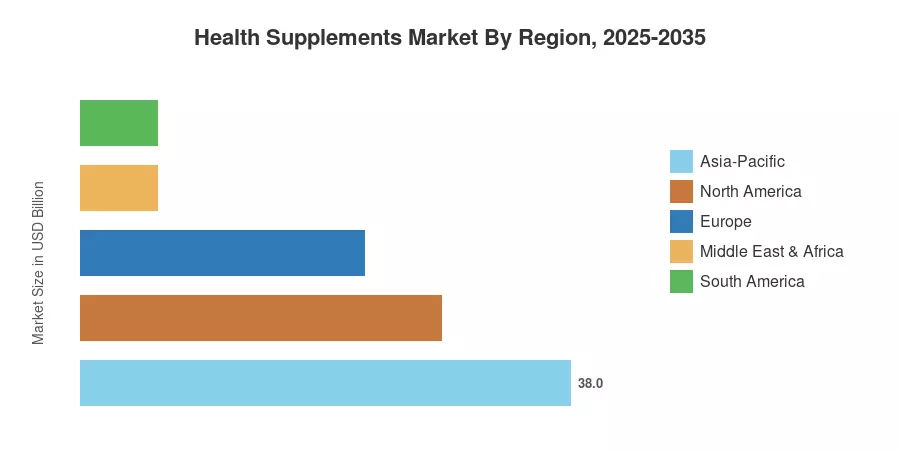

Asia-Pacific commands the largest share of the Health Supplements Market at approximately 38% of global revenue, supported by robust consumer spending in China, Japan, and India. Middle East & Africa represents the fastest-growing region, where rising disposable incomes and expanding pharmacy retail networks are accelerating supplement adoption. North America holds the second-largest share at roughly 28%, driven by a mature e-commerce infrastructure and high per-capita supplement spending [5].

Key Report Takeaways

• By Product Type

- Vitamins captured approximately 29% of the Health Supplements Market in 2025, led by Vitamin D and multivitamin formulations targeting immune and bone health.

- Prebiotics and probiotics represent the fastest-growing product category, expanding at a CAGR of 10.3% through 2035, fueled by clinical evidence linking gut microbiome diversity to immune and cognitive function.

• By Form

- Capsules and tablets continue to dominate by volume, though gummy formats are gaining ground at a CAGR of 13.0% as formulators expand flavor profiles and eliminate gelatin-based ingredients.

- Powder-based supplements are gaining traction in the Health Supplements Market, particularly among fitness-oriented consumer segments in North America and Europe.

• By Region

- Asia-Pacific leads the Health Supplements Market with the highest regional revenue, driven by China's Healthy China 2030 initiative and Japan's aging population.

- Middle East & Africa is poised to grow at the highest regional CAGR through 2035, supported by government healthcare diversification strategies in Saudi Arabia and the UAE.

Health Supplements Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining top-down revenue analysis from publicly listed supplement manufacturers, bottom-up channel audits across pharmacy, e-commerce, and specialty retail, and cross-validation against regulatory filing databases maintained by the FDA, EFSA, and FSSAI.